Home Diagnostics & Self-Testing Market Research Report – Segmented by Product Type (Blood Glucose Monitoring Tests, Pregnancy & Fertility Tests, Infectious Disease Test Kits, Cardiovascular Monitoring Tests, Cholesterol Test Kits, Drug & Alcohol Testing Kits, Genetic & DNA Testing Kits, Others); by Sample Type (Blood, Urine, Saliva, Stool, Breath, Others); by Distribution Channel (Retail Pharmacies, Online Pharmacies & E-commerce Platforms, Supermarkets & Hypermarkets, Direct-to-Consumer (DTC) Channels, Others); by Technology (Lateral Flow Assays, Immunoassays, Molecular Diagnostics, Biosensors & Wearable-based Testing, Others); and Region - Size, Share, Growth Analysis | Forecast (2026– 2030)

Global Home Diagnostics & Self-Testing Market Size (2026-2030)

In 2025, the Home Diagnostics & Self-Testing Market was valued at approximately USD 9.85 Billion. It is projected to grow at a CAGR of around 7.9% during the forecast period of 2026–2030, reaching an estimated USD 14.41 Billion by 2030.

The home diagnostics and self-testing market is the global ecosystem of consumer-facing test kits and devices, which are used outside clinical settings to detect, monitor, or screen health conditions. These products allow individuals to create health insights with the help of simple procedures at home, which may require little training. The market comprises a broad scope of rapid and monitoring solutions in the context of chronic disease management, reproductive health, detecting infectious diseases, and preventive screening. It narrows down to the sale of physical test kits and devices and does not extend to laboratory-based diagnostics, professional medical care, and physician-led testing processes.

Over the past few years, the market has shifted not only from the occasional, need-based testing but also to a more continuous and preventative approach of self-monitoring. This change has been informed by a growing health awareness, integration of digital health, and normalization of remote care models. Simultaneously, regulatory oversight with regard to accuracy and claims has escalated, imposing greater barriers to the entry of new products. The supply chain interruptions and the imbalance in the supply of major components have also affected the availability of products and their prices, complicating the process of expanding operations to other regions.

To decision-makers, these shifts are redefining value creation and capture. The new rules of success require coordinating product design and user convenience, choosing scalable technologies, and dealing with fragmented distribution channels. Businesses also need to consider regional regulatory directions and demand fluctuation more closely. The wrong estimation of such factors may result in overinvestment or late entry into the market, so informed, segment-level analysis is required to be effective in strategy.

Key Market Insights

India increased health expenditure to 2% of budget, an increase of 10% on average.

The volume of dealings in the Asia Pacific increased 12%, with China increasing 53%.

The increase in medical expenses was 7% ear, which further promoted the adoption of home-based monitoring options.

A survey of 100 executives in 15 countries points to recovery-speed disparities in medtech.

Monitoring equipment is used by 37%, and monitoring health or fitness is used by 47% of users claim to use healthcare apps or wearables monthly, which indicates the development of a habit.

A quarter (28) would pay higher to receive individualized treatment; a quarter (22) to monitor it.

49% of the healthcare respondents are implementing DevSecOps for digital risk.

High-income super consumers (51 percent) prefer the option of at-home care now.

Over 90% would revisit virtuously, increasing the use of self-testing.

24% would change physicians in case they lose virtual visits, particularly younger.

The 35% at-home test substitution in China is an indicator of high consumer willingness today.

The US consumers are interested: 26% vitamin, 24% flu, 23% cholesterol testing.

One out of every 2 surveyed consumers has purchased wearables; more than 75% of consumers are open to them.

Research Methodology

Scope & Definitions

Boundary: product/system sales of home diagnostics & self-testing kits/devices; excludes lab-based diagnostics and services revenue.

Segmentation: product type, sample type, distribution channel, technology, and region; MECE with “Others” buckets.

Geography/timeframe: global coverage with regional splits; historical, base year, and forecast period defined in-report.

Data dictionary standardizes test types, channels, and technologies; strict rules prevent double counting across segments.

Evidence Collection (Primary + Secondary)

Primary: interviews across manufacturers, distributors, retailers, clinicians, and regulatory experts; multi-level validation.

Secondary: World Health Organization, U.S. Food and Drug Administration, Centers for Disease Control and Prevention, company filings, investor reports, clinical publications, and relevant regulators/standards bodies/industry associations specific to {Global Home Diagnostics & Self-Testing Market} (named in-report).

All key claims are supported by verifiable sources with source-linked evidence in the report.

Triangulation & Validation

Dual sizing: bottom-up aggregation of company revenues and unit shipments; top-down benchmarking against healthcare spending and diagnostics penetration.

Reconciliation with audited financials and disclosures; conflicting-source resolution via weighted credibility scoring and expert validation.

Presentation & Auditability

Transparent assumptions, formulas, and segment bridges documented; reproducible models.

Version-controlled datasets with traceable citations; audit trail ensures decision-grade reliability.

Global Home Diagnostics & Self-Testing Market Drivers

Increasing need for decentralized medical care and real-time health information.

The trend of healthcare delivery moves toward decentralized consumer-controlled settings as opposed to centralized clinical settings, which drives the need for home diagnostics and self-testing solutions. Even patients grow to anticipate actionable health information on demand without the need to schedule a clinical appointment or wait until laboratory results are obtained. This change in behavior is in line with the greater healthcare automation trends, in which digital platforms incorporate test results into personal health ecosystems.

The technological progress in digital-enabled testing technologies is enhancing the accessibility of users.

Home diagnostics are changing the process of testing and making it more accurate, intuitive, and reachable through technological innovation. Contemporary devices are more and more equipped with biosensors, mobile connectivity, and app-based interfaces that guide users through testing procedures and interpret results in real time.

The growth of direct-to-consumer distribution systems is redefining market accessibility.

The fast development of direct-to-consumer and e-commerce channels is redefining the way in which diagnostic products reach end users, accelerating the penetration into the market. Consumers are now interested in convenient buying possibilities where they have privacy, speed, and a greater variety of products than in the traditional retail environments. Online solutions take advantage of data analytics and personalized recommendations to pair users with the right testing solutions, driving greater engagement and repeat use.

Global Home Diagnostics & Self-Testing Market Restraints

The regulatory fragmentation and changing approval standards remain a slowing factor to product launches and raise compliance costs. The issues of accuracy and inconsistent execution of the tests by the users erode trust, particularly when complex tests are required, and accurate handling of the tests is essential. Volatility in the supply chain is breaking the supply chain components, and the price pressure is increasing across the online channels. The privacy risks associated with connected machines make the adoption more challenging.

Global Home Diagnostics & Self-Testing Market Opportunities

The growing consumer desire to receive convenient, at-home healthcare opens significant prospects to the development of integrated self-testing ecosystems based on the combination of diagnostics with the digital tracking of the body and remote consultations. Expansion in preventive health awareness assists in the demand for reoccurring monitoring solutions, particularly for chronic illnesses. The emerging markets have untapped potential due to improved accessibility and increased affordability.

How this market works end-to-end

Product design phase

Manufacturers define product types such as glucose, infectious disease, or genetic kits, aligning with target use cases.

Technology selection

Choices between lateral flow, molecular diagnostics, or biosensors determine cost, speed, and accuracy.

Sample alignment

Design adapts to blood, urine, saliva, stool, or breath inputs based on user convenience and test sensitivity.

Regulatory pathway

Products undergo approval processes that vary by region and technology complexity.

Manufacturing scale-up

Production capacity must align with demand spikes, especially for infectious disease testing.

Channel distribution

Products move through retail pharmacies, e-commerce, supermarkets, or direct-to-consumer models.

Consumer usage

End users perform tests at home, with usability and clarity driving repeat usage.

Data integration

Some devices connect to apps or platforms, enabling tracking and remote health insights.

Post-market monitoring

Manufacturers track performance, recalls, and compliance updates across regions.

Why this market matters now

The core pressure is not demand—it is alignment. Demand is strong, but uneven. Some categories see spikes, others plateau. At the same time, regulatory bodies are tightening oversight on accuracy and claims. This creates a mismatch between innovation speed and approval timelines.

Supply chains add another layer of uncertainty. Components for biosensors or molecular kits face sourcing delays. Distribution channels are also shifting. Online platforms are gaining share, but they introduce pricing pressure and counterfeit risks.

Geopolitical and economic volatility affects import dependencies, currency exposure, and regional pricing strategies. Buyers must decide where to invest, what to scale, and how to hedge risk—without clear signals from traditional market indicators.

What matters most when evaluating claims in this market

Claim type

What good proof looks like

What often goes wrong

Market size

Segmented, non-overlapping data by product and region

Double counting across product categories

Growth potential

Channel-specific and technology-specific trends

Overgeneralized global averages

Accuracy claims

Clinical validation and regulatory approvals

Marketing-led claims without verification

Demand signals

Repeat purchase rates and usage frequency

One-time spike extrapolation

Distribution strength

Channel share with inventory flow data

Ignoring stockouts or supply gaps

The decision lens

Define boundary clearly

Confirm what is included as product sales versus services to avoid scope errors.

Segment demand correctly

Compare product types, sample types, and channels without overlap.

Validate regulatory paths

Assess approval timelines and compliance risks across regions.

Stress-test supply chain

Check supplier concentration, lead times, and component dependencies.

Compare channel economics

Evaluate margins and control across retail, online, and direct models.

Assess technology fit

Match technology choice with scalability, cost, and user adoption.

Time market entry

Identify signals of saturation, regulatory shifts, or demand spikes.

The contrarian view

Many assume this market grows uniformly with rising health awareness. It does not. Growth is uneven and often reactive. Infectious disease testing can surge, then drop sharply. Chronic condition monitoring grows steadily but faces pricing pressure.

Another common mistake is treating all self-tests as interchangeable. Technology, sample type, and channel create distinct sub-markets with different economics. Ignoring this leads to flawed forecasts.

Double counting is also widespread. Products that serve multiple use cases or channels are often counted more than once, inflating market estimates.

Practical implications by stakeholder

Manufacturers

Prioritize scalable technologies over niche innovation

Align product design with regulatory ease

Distributors

Diversify channels to reduce dependency risk

Monitor inventory volatility closely

Retailers and e-commerce platforms

Focus on trusted brands to reduce return rates

Manage counterfeit and compliance risks

Investors

Avoid broad market assumptions

Focus on segment-level performance signals

Healthcare providers

Integrate home testing data cautiously

Validate accuracy before recommending products

Regulators

Balance access with safety

Monitor cross-border product flows

HOME DIAGNOSTICS & SELF-TESTING MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2025 - 2030

Base Year

2025

Forecast Period

2026 - 2030

CAGR

7.9%

Segments Covered

By Product Type, Sample Type , Technology , , Distribution Channel and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Johnson & Johnson, Becton, Dickinson and Company, Dexcom Inc., Ascensia Diabetes Care, QuidelOrtho Corporation, Bio-Rad Laboratories, Thermo Fisher Scientific, OraSure Technologies, SD Biosensor Inc., Hologic Inc., Danaher Corporation, and Acon Laboratories.

Global Home Diagnostics & Self-Testing Market Segmentation

Global Home Diagnostics & Self-Testing Market – By Product Type

Blood glucose monitoring tests dominate the product type segment with a share of about 28% due to the constant demand of diabetic populations and the frequent need to be tested. About 18 percent of the world uses the infectious disease test kits, whereas the pregnancy and fertility tests constitute almost 14 percent of the entire world.

The fastest developing type of product is infectious disease test kits, with an almost 18 percent growth rate, which is supported by the increase in demand for rapid diagnostics and home-based screening. About 9 percent are the genetic and DNA testing kits, and approximately 10 percent are the cardiovascular monitoring tests.

Global Home Diagnostics & Self-Testing Market – By Sample Type

The segment with the largest share in the distribution channel is retail pharmacies, which have a share of almost 38%, which is well supported by consumer trust and great accessibility. Online pharmacies and e-commerce platforms have about a 27% share, while the supermarkets and hypermarkets have approximately a 14% share of the overall market revenue.

The fastest-growing channel with an approximate share of 27% is online pharmacies and e-commerce platforms due to convenience and pricing benefits. Direct-to-consumer channels occupy almost a 13% share, with retail pharmacies still holding a significant share at about 38% across the globe.

Global Home Diagnostics & Self-Testing Market – By Technology

Global Home Diagnostics & Self-Testing Market– Regional Analysis

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

The regional segment exhibits a relatively large share of about 38%, with the support of a highly developed healthcare infrastructure and high consumer adoption of the self-testing solutions. Europe shares almost one-fifth of the total market demand, with Asia Pacific sharing almost one-fourth of the total market demand.

The fastest-growing region is the Asia Pacific, with approximately 27% share due to increasing healthcare awareness and the growing access to diagnostics. With a share of 38, North America leads with a share of about 38, trailed by Europe and South America with shares of about 20 and 8, respectively.

Latest Market News

Mar 18, 2026: A major diagnostics company has announced the expansion of its at-home infectious disease testing portfolio to increase production capacity by 35% relative to levels at the start of 2025 and intends to distribute it across 22 countries by Q4 2026. The company also reported that there was a 28% increase in the direct-to-consumer sales between Jul 2025 and Feb 2026, indicating strong traction of the online channel.

Jan 09, 2026: A big wearable health technology company introduced a next-generation biosensor-based home monitoring device with 20 percent higher accuracy compared to its 2024 model and with a battery life of 14 days as opposed to 10 days. It was first rolled out in 5 main markets and is estimated that over 1.2 million units will be rolled out by Dec 2026.

Nov 27, 2025: A global player in the diagnostics sector entered into a strategic partnership with an online shopping platform to increase the availability of home testing kits, increasing online SKU listings by 45 percent compared to Mar 2025 and reducing 72-hour delivery time to 36 hours across 8 regions. The partnership is to increase contributions to the digital sales to more than 30 percent by mid-2026.

Sep 14, 2025: A major healthcare firm has managed to acquire a home diagnostics startup in a deal that is valued at around USD 180 million, acquiring over 25 proprietary test kits in the process. It is projected that the acquisition will put it in 12 new regional markets by early 2026.

Jun 03, 2025: A molecular diagnostics company announced the release of a rapid home-use test platform that delivers results in less than 15 minutes, nearly four times faster than its 2023 models. The firm announced that it had already distributed 500,000 units in North America and Europe in the first 60 days.

Feb 11, 2025: A global chain of retail pharmacy stores expanded a line of home testing products in its own label and increased its shelf space by 25 percent across 9,000 stores and added 10 variants of its own-label product range between Aug 2024 and Jan 2025. The project helped to increase the sales of in-store diagnostic kits by 17 percent in the same time frame.

Oct 22, 2024: A digital health company has just raised USD 95 million to scale its direct-to-consumer genetic testing offerings with the goal of growing its clientele by 3.5 million customers by the end of 2025. As of Sep 2024, the firm also recorded a year-over-year growth in subscription-based testing services by 32%.

Jul 05, 2024: A global manufacturer of diagnostics announced the regulatory clearance of a new home-use cardiovascular test kit across 6 countries where it has achieved sensitivity values over 92% and specificity over 90% in clinical validation studies conducted between Jan 2023 and Apr 2024. The company has set the target of increasing production by 30% by the beginning of 2025.

Key Players

Abbott Laboratories

Roche Diagnostics

Siemens Healthineers

Johnson & Johnson

Becton, Dickinson and Company

Dexcom Inc.

Ascensia Diabetes Care

QuidelOrtho Corporation

Bio-Rad Laboratories

Thermo Fisher Scientific

Questions buyers ask before purchasing this report

How is the market size calculated without double counting?

The report uses a strict segmentation framework where each product is assigned to a single category based on primary use. Overlapping use cases are resolved using a hierarchy rule. Channel revenues are not added separately to product revenues, preventing duplication. Regional splits are applied after product-level aggregation, ensuring consistency.

Does the report differentiate between test types and technologies?

Yes. Product types such as glucose or infectious disease tests are analyzed separately from technologies like lateral flow or molecular diagnostics. This allows buyers to see how technology choices impact growth, cost, and regulatory timelines without mixing them with demand-side categories.

How are regional differences handled?

The report breaks down the market by major regions, accounting for regulatory variation, distribution structures, and demand patterns. It avoids applying uniform growth assumptions across regions and instead reflects localized dynamics.

What kind of primary research supports the findings?

Insights are validated through interviews across the value chain, including manufacturers, distributors, and healthcare professionals. Conflicting inputs are resolved using credibility weighting and cross-verification with secondary data.

Can this report help with go-to-market strategy?

Yes. It provides clarity on which channels are gaining traction, how pricing varies across them, and where consumer adoption is strongest. This helps in selecting the right entry strategy and avoiding costly misalignment.

How does the report address supply chain risks?

It evaluates sourcing dependencies, production bottlenecks, and distribution constraints. This allows buyers to anticipate risks that could impact availability and pricing.

Is demand stable across all product categories?

No. Demand varies significantly by product type. Some categories show steady growth, while others are highly volatile. The report highlights these differences to prevent overgeneralization.

What decisions does this report directly support?

It supports portfolio planning, regional expansion, channel selection, and risk management. It helps buyers make informed choices under uncertainty and avoid misreading market signals.

To Learn more about this report,

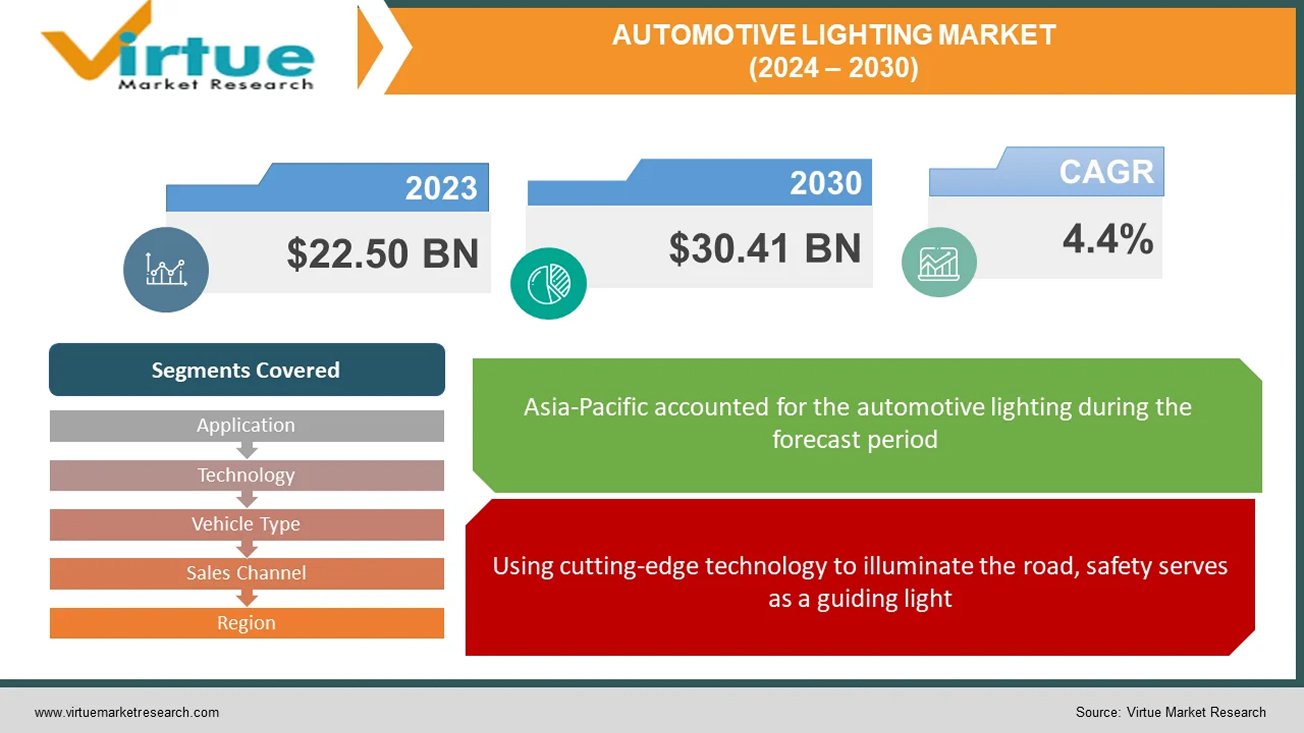

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

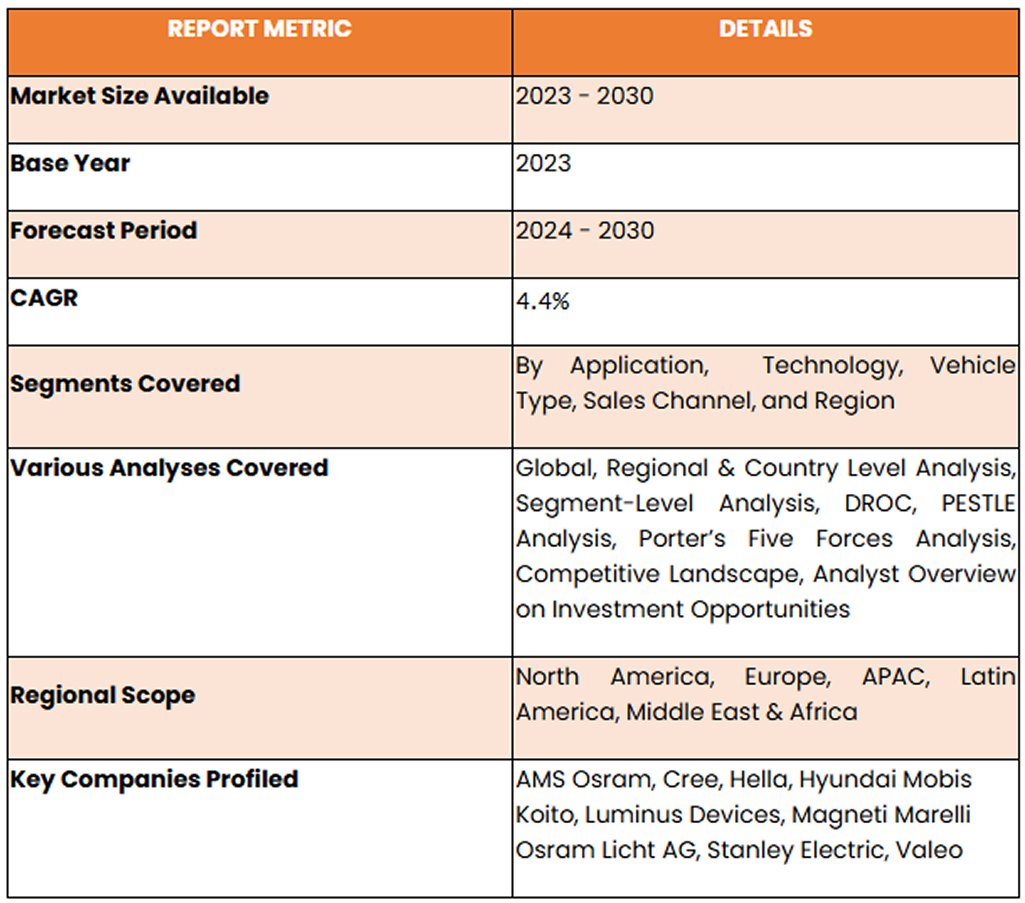

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

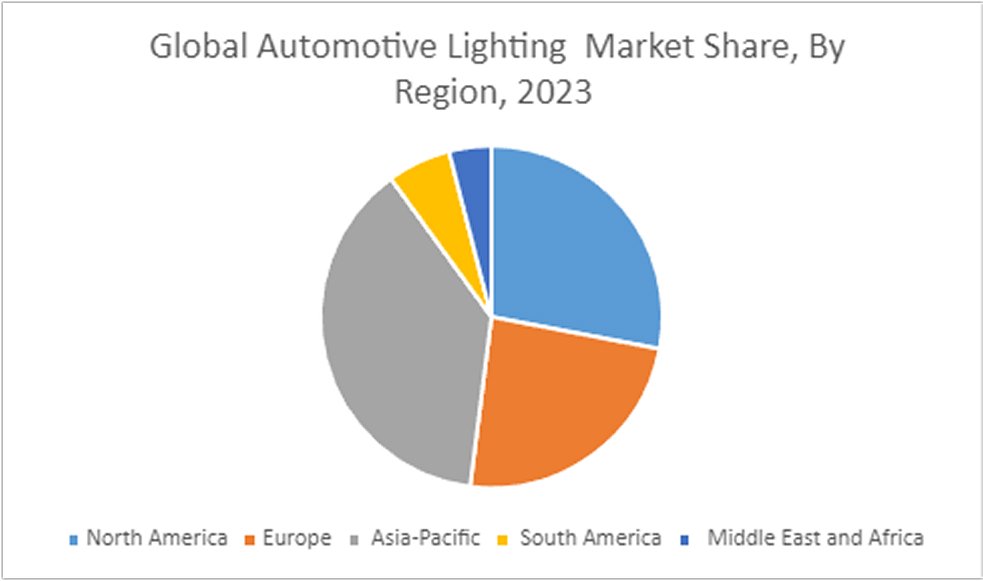

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. HOME DIAGNOSTICS & SELF-TESTING MARKET – SCOPE & METHODOLOGY

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Source

1.5. Secondary Source Chapter 2. HOME DIAGNOSTICS & SELF-TESTING MARKET – EXECUTIVE SUMMARY

2.1. Market Size & Forecast – (2026 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis Chapter 3. HOME DIAGNOSTICS & SELF-TESTING MARKET – COMPETITION SCENARIO

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Packaging PRODUCT TYPE Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis Chapter 4. HOME DIAGNOSTICS & SELF-TESTING MARKET - ENTRY SCENARIO

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Players

4.5.6. Threat of Substitutes Chapter 5. HOME DIAGNOSTICS & SELF-TESTING MARKET - LANDSCAPE

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities Chapter 6. HOME DIAGNOSTICS & SELF-TESTING MARKET – By Product Type

6.1 Introduction/Key Findings

6.2 Blood Glucose Monitoring Tests

6.3 Pregnancy & Fertility Tests

6.4 Infectious Disease Test Kits

6.5 Cardiovascular Monitoring Tests

6.6 Cholesterol Test Kits

6.7 Drug & Alcohol Testing Kits

6.8 Genetic & DNA Testing Kits

6.9 Others

6.10 Y-O-Y Growth trend Analysis By Product Type

6.11 Absolute $ Opportunity Analysis By Product Type , 2026-2030

Chapter 7. HOME DIAGNOSTICS & SELF-TESTING MARKET – By Sample Type

7.1 Introduction/Key Findings

7.2 Blood

7.3 Urine

7.4 Saliva

7.5 Stool

7.6 Breath

7.7 Others

7.8 Y-O-Y Growth trend Analysis By Sample Type

7.9 Absolute $ Opportunity Analysis By Sample Type, 2026-2030

Chapter 10. HOME DIAGNOSTICS & SELF-TESTING MARKET , By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product Type

10.1.3. By Technology

10.1.4. By Distribution Channel

10.1.5. Sample Type

10.1.6. Countries & Segments - Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product Type

10.2.3. By Technology

10.2.4. By Distribution Channel

10.2.5. Sample Type

10.2.6. Countries & Segments - Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.2. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product Type

10.3.3. By Sample Type

10.3.4. By Distribution Channel

10.3.5. Technology

10.3.6. Countries & Segments - Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Sample Type

10.4.3. By Product Type

10.4.4. By Technology

10.4.5. Distribution Channel

10.4.6. Countries & Segments - Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.4. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.10. Egypt

10.5.1.10. Rest of MEA

10.5.2. By Sample Type

10.5.3. By Product Type

10.5.4. By Distribution Channel

10.5.5. Technology

10.5.6. Countries & Segments - Market Attractiveness Analysis Chapter 11. HOME DIAGNOSTICS & SELF-TESTING MARKET – Company Profiles – (Overview, Portfolio, Financials, Strategies & Developments)

11.1 Abbott Laboratories

11.2 Roche Diagnostics

11.3 Siemens Healthineers

11.4 Johnson & Johnson

11.5 Becton, Dickinson and Company

11.6 Dexcom Inc.

11.7 Ascensia Diabetes Care

11.8 QuidelOrtho Corporation

11.9 Bio-Rad Laboratories

11.10 Thermo Fisher Scientific

Fill out the form below and our team will get back to you shortly

FAQ's

In 2025, the Home Diagnostics & Self-Testing Market was valued at approximately USD 9.85 Billion. It is projected to grow at a CAGR of around 7.9% during the forecast period of 2026–2030, reaching an estimated USD 14.41 Billion by 2030.

In 2025, the Home Diagnostics & Self-Testing Market was valued at approximately USD 9.85 Billion. It is projected to grow at a CAGR of around 7.9% during the forecast period of 2026–2030, reaching an estimated USD 14.41 Billion by 2030.

The major drivers of the Global Home Diagnostics & Self-Testing Market include the increasing shift toward decentralized and consumer-centric healthcare, where individuals demand real-time health insights without clinical dependency. The growing integration of digital health technologies such as biosensors, mobile applications, and connected diagnostic devices is improving accuracy, usability, and accessibility of home testing solutions. Additionally, the rapid expansion of direct-to-consumer and e-commerce distribution channels is significantly enhancing product availability, privacy, and purchasing convenience, thereby accelerating market adoption across both developed and emerging regions.

The major drivers of the Global Home Diagnostics & Self-Testing Market include the increasing shift toward decentralized and consumer-centric healthcare, where individuals demand real-time health insights without clinical dependency. The growing integration of digital health technologies such as biosensors, mobile applications, and connected diagnostic devices is improving accuracy, usability, and accessibility of home testing solutions. Additionally, the rapid expansion of direct-to-consumer and e-commerce distribution channels is significantly enhancing product availability, privacy, and purchasing convenience, thereby accelerating market adoption across both developed and emerging regions.

Blood Glucose Monitoring Tests, Pregnancy & Fertility Tests, Infectious Disease Test Kits, Cardiovascular Monitoring Tests, Cholesterol Test Kits, Drug & Alcohol Testing Kits, Genetic & DNA Testing Kits, and Others are the segments under the Global Home Diagnostics & Self-Testing Market by Product Type. Blood, Urine, Saliva, Stool, Breath, and Others are the segments by Sample Type. Retail Pharmacies, Online Pharmacies & E-commerce Platforms, Supermarkets & Hypermarkets, Direct-to-Consumer (DTC) Channels, and Others are the segments by Distribution Channel. Lateral Flow Assays, Immunoassays, Molecular Diagnostics, Biosensors & Wearable-based Testing, and Others are the segments by Technology.

Blood Glucose Monitoring Tests, Pregnancy & Fertility Tests, Infectious Disease Test Kits, Cardiovascular Monitoring Tests, Cholesterol Test Kits, Drug & Alcohol Testing Kits, Genetic & DNA Testing Kits, and Others are the segments under the Global Home Diagnostics & Self-Testing Market by Product Type. Blood, Urine, Saliva, Stool, Breath, and Others are the segments by Sample Type. Retail Pharmacies, Online Pharmacies & E-commerce Platforms, Supermarkets & Hypermarkets, Direct-to-Consumer (DTC) Channels, and Others are the segments by Distribution Channel. Lateral Flow Assays, Immunoassays, Molecular Diagnostics, Biosensors & Wearable-based Testing, and Others are the segments by Technology.

North America is the most dominant region for the Global Home Diagnostics & Self-Testing Market, holding approximately 38% share. This leadership is supported by advanced healthcare infrastructure, strong consumer adoption of self-testing solutions, and widespread availability of regulated diagnostic products. Asia Pacific is the fastest-growing region, driven by rising healthcare awareness, expanding digital health penetration, and increasing demand for affordable at-home testing solutions. Europe maintains a stable share due to mature healthcare systems and preventive care adoption, while Latin America and the Middle East & Africa are witnessing gradual growth supported by improving healthcare access and awareness.

North America is the most dominant region for the Global Home Diagnostics & Self-Testing Market, holding approximately 38% share. This leadership is supported by advanced healthcare infrastructure, strong consumer adoption of self-testing solutions, and widespread availability of regulated diagnostic products. Asia Pacific is the fastest-growing region, driven by rising healthcare awareness, expanding digital health penetration, and increasing demand for affordable at-home testing solutions. Europe maintains a stable share due to mature healthcare systems and preventive care adoption, while Latin America and the Middle East & Africa are witnessing gradual growth supported by improving healthcare access and awareness.

The key players in the Global Home Diagnostics & Self-Testing Market include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Johnson & Johnson, Becton, Dickinson and Company, Dexcom Inc., Ascensia Diabetes Care, QuidelOrtho Corporation, Bio-Rad Laboratories, Thermo Fisher Scientific, OraSure Technologies, SD Biosensor Inc., Hologic Inc., Danaher Corporation, and Acon Laboratories.

The key players in the Global Home Diagnostics & Self-Testing Market include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Johnson & Johnson, Becton, Dickinson and Company, Dexcom Inc., Ascensia Diabetes Care, QuidelOrtho Corporation, Bio-Rad Laboratories, Thermo Fisher Scientific, OraSure Technologies, SD Biosensor Inc., Hologic Inc., Danaher Corporation, and Acon Laboratories.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19361 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Newborn Screening Market was valued at approximately USD 6.14 Billion. It is projected to grow at a CAGR of around 7.6% during the forecast period of 2026–2030, reaching an estimated USD 8.86 Billion by 2030...

Report Code: VMR-19360 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Home Diagnostics & Self-Testing Market was valued at approximately USD 9.85 Billion. It is projected to grow at a CAGR of around 7.9% during the forecast period of 2026–2030, reaching an estimated USD 14.41...

Report Code: VMR-19358 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Clinical Microbiology Testing Market was valued at approximately USD 9.85 Billion. It is projected to grow at a CAGR of around 7.9% during the forecast period of 2026–2030, reaching an estimated USD 14.41 Bi...

Report Code: VMR-19356 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Global Fertility Services & IVF Technology Market was valued at approximately USD 53 Billion and is projected to reach around USD 82.30 Billion by 2030, expanding at a CAGR of about 9.2% during 2026–2030.

Report Code: VMR-19355 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Global Women’s Health Diagnostics & Devices Market was valued at approximately USD 58.40 Billion. It is projected to grow at a CAGR of around 6.8% during the forecast period of 2026–2030, reaching an estimat...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”