Utility-Scale Power Asset Life Extension Market Research Report –Segmentation by Service Type (Inspection & Condition Assessment, Refurbishment & Overhaul, Retrofit & Modernization, Life Assessment & Engineering Studies, Long-Term Service Agreements, Others), By Asset Type (Turbines, Generators, Boilers & Heat Recovery Systems, Transformers & Substations, Balance of Plant Systems, Others), and Region - Size, Share, Growth Analysis | Forecast (2026– 2030)

Global Utility-Scale Power Asset Life Extension Market Size (2026-2030)

The Global Utility-Scale Power Asset Life Extension Market was valued at USD 18.4 billion in 2025 and is projected to grow at a CAGR of 6.9% from 2026 to 2030. The market is expected to reach USD 25.5 billion by 2030.

The Utility-Scale Power Asset Life Extension Market centers on services, engineering solutions, upgrades, retrofits, digital diagnostics, refurbishment programs, and component replacement strategies designed to extend the operational lifespan of large-scale power generation and utility infrastructure assets. These assets include gas turbines, steam turbines, generators, boilers, transformers, substations, hydro units, and associated balance-of-plant systems. Rather than replacing aging infrastructure outright, utilities and independent power producers are increasingly pursuing life extension programs to improve reliability, increase operating flexibility, comply with emissions and efficiency standards, and optimize capital expenditure. Market demand is strengthening as many installed utility-scale assets worldwide approach or exceed their original design life, while electricity systems still require dependable dispatchable and flexible capacity. Growing pressure to integrate renewable energy, maintain grid stability, and modernize legacy generation fleets is further supporting adoption. Asset owners are prioritizing selective modernization, performance restoration, digital monitoring, and outage optimization to preserve long-term value from existing infrastructure. As a result, the market is developing into a strategic investment area across mature and emerging power systems.

Key Market Insights

A large share of utility-scale thermal and hydro assets globally are operating beyond 25–30 years of service life, making refurbishment, turbine overhauls, and control system modernization increasingly important for plant owners seeking to defer replacement capital.

Gas turbine life extension programs are gaining traction because targeted upgrades can improve output by 2%–7% and in some cases add 10–30 MW of incremental capacity, creating a measurable return on modernization spending.

Utilities are increasingly allocating 8%–15% of annual plant maintenance budgets toward predictive diagnostics, asset health monitoring, and outage analytics, showing the market’s shift from reactive repair to planned life management.

Environmental compliance remains a core purchase trigger, as retrofits for emissions control, combustion optimization, and heat-rate improvement can reduce operating losses by 3%–8% while extending asset usability.

Hydropower life extension demand is expanding steadily because many utility-scale hydro units commissioned decades ago can operate for 40–80 years with staged rehabilitation of turbines, generators, civil structures, and automation systems.

Transformer and substation life extension is becoming a parallel growth pocket, especially as long procurement lead times for new grid equipment are encouraging utilities to use retrofit and refurbishment solutions instead of full replacement.

Asia-Pacific and North America account for a significant portion of ongoing modernization demand due to their large installed base of aging thermal, hydro, and transmission assets combined with rising grid reliability expectations.

Digital asset performance management platforms are improving maintenance planning accuracy by roughly 10%–20% in many utility use cases, helping operators reduce unplanned outages and extend useful operating life through better intervention timing.

Research Methodology

Scope & definitions

Covers services-only revenue generated from utility-scale asset life extension for power generation and grid assets, including inspection, refurbishment, retrofit, modernization, life assessment, engineering studies, and long-term service agreements.

Includes utility-scale thermal, hydro, nuclear, renewable-linked electrical assets, transformers, substations, and balance-of-plant systems; excludes greenfield EPC, full asset replacement, routine O&M, fuel supply, and non-utility distributed assets.

Geography: global; timeframe: historical review, 2025 base year, and 2026–2030 forecast.

Segmentation follows a MECE structure with a standardized data dictionary and explicit rules to prevent overlap and double counting.

Evidence collection

Secondary research uses verifiable sources such as company annual reports, investor presentations, OEM service portfolios, utility filings, grid/planning documents, EPRI materials, and relevant regulators/standards bodies/industry associations specific to the Utility-Scale Power Asset Life Extension Market (named in-report).

Primary research covers OEMs, EPC/service providers, utilities, IPPs, grid operators, asset managers, and technical consultants across regions.

Key claims in the report are supported by source-linked evidence and interview validation, with conflicting-source resolution and bias controls applied.

Triangulation & validation

Market sizing uses both bottom-up aggregation of service revenues/contracts and top-down allocation from utility asset-management and modernization spending pools.

Forecasts are reconciled to installed asset base, outage cycles, refurbishment intensity, project pipelines, and financial disclosures where applicable.

Cross-checks are applied at segment, regional, and company level to ensure consistency.

Presentation & auditability

All assumptions, inclusions/exclusions, formulas, and estimation logic are documented for auditability.

The report presents decision-grade tables, charts, and source-linked evidence trails for major estimates and conclusions.

Global Utility-Scale Power Asset Life Extension Market Drivers

Aging Utility Fleets Need Cost Optimization is driving the market growth

A major driver for the global utility-scale power asset life extension market is the rising age profile of installed generation and grid infrastructure combined with the high cost of building replacement assets. Across developed and developing electricity systems, many gas turbines, steam turbines, hydro turbines, generators, boilers, transformers, and substation systems are already operating near or beyond their initial design life. Even when these assets remain functional, efficiency degradation, mechanical wear, control obsolescence, and reliability risks increase with time. Replacing entire facilities demands very high capital commitments, long permitting cycles, lengthy procurement timelines, and in many countries exposure to policy uncertainty. In contrast, structured life extension programs allow operators to restore performance, improve safety margins, and preserve dispatchable capacity at a lower cost than greenfield development.

Grid Reliability Needs Flexible Existing Assets is driving the market growth

Another major driver is the growing requirement for grid reliability and operational flexibility in power systems undergoing rapid structural change. Electricity networks are absorbing larger shares of variable renewable generation, electrification-led demand growth, and more extreme weather-related disruptions. Under these conditions, utilities cannot rely solely on new-build capacity arriving on time or at predictable cost. Existing utility-scale assets still play a critical role in maintaining voltage support, inertia, reserve margins, black-start capability, and peak balancing. However, older assets must remain dependable if they are to serve that function effectively. Life extension investments enable operators to keep strategically important plants and grid systems available for longer periods while enhancing responsiveness and resilience. Upgrades to turbine controls, excitation systems, monitoring software, cooling systems, and auxiliary equipment can improve ramping behavior, reduce trip events, and support frequent cycling demanded by renewable-heavy grids.

Global Utility-Scale Power Asset Life Extension Market Challenges and Restraints

Regulatory Uncertainty Limits Long-Term Commitments is restricting the market growth

A key restraint in the global utility-scale power asset life extension market is regulatory and policy uncertainty surrounding the long-term role of legacy utility assets, especially thermal generation. Asset owners may recognize the technical and economic value of extending plant life, yet investment decisions are often delayed when carbon policy, emissions compliance obligations, market design rules, or retirement mandates remain unclear. In several countries, utilities must weigh whether a life extension project with a 10- to 20-year benefit horizon will remain commercially viable under future decarbonization frameworks. This is particularly challenging for coal and older gas assets, where plant modernization may improve efficiency but still face tightening environmental scrutiny.

Market Opportunities

The strongest opportunity in the global utility-scale power asset life extension market lies in integrated modernization programs that combine hardware refurbishment, digital intelligence, emissions optimization, and flexibility upgrades into a single value proposition. Historically, many operators approached life extension as a maintenance problem focused on isolated component replacement. The next phase of the market is broader and more strategic. Utilities now need existing assets to deliver more than simple endurance; they want higher availability, lower heat rates, faster ramping, improved compliance performance, and better compatibility with renewable-heavy grids. This creates a major opening for companies that can package outage planning, predictive diagnostics, advanced controls, remote monitoring, turbine upgrades, transformer retrofits, and balance-of-plant engineering into modular long-term service offerings.

How this market works end-to-end

The market works through a fairly practical chain, even if suppliers often make it sound more complex than it is.

First, a utility, grid operator, or independent power producer identifies an aging asset with rising outage risk, falling efficiency, control obsolescence, or compliance pressure. That asset may be a turbine, generator, boiler, heat recovery system, transformer, substation component, or a broader balance-of-plant system.

Second, the owner defines whether the need is diagnostic, corrective, or strategic. Some projects begin with inspection and condition assessment. Others start with a forced outage, a life assessment study, or a long-term service planning cycle.

Third, engineering teams assess remaining useful life. This is where life assessment and engineering studies matter. The buyer wants to know whether the asset can run safely and economically beyond its original design window.

Fourth, the owner decides the service path. That may be refurbishment and overhaul for worn assets, retrofit and modernization for controls or performance upgrades, or a long-term service agreement when the goal is predictable lifecycle management.

Fifth, the vendor scope is matched to the asset class. Turbines and generators often attract the highest scrutiny because they sit at the center of plant output. Boilers and heat recovery systems matter in thermal assets. Transformers and substations matter when grid reliability is under stress. Balance-of-plant systems come into play when auxiliary failure drives hidden downtime.

Sixth, the business case is tested across the operating context. A gas-fired plant, a hydro facility, a nuclear unit, and a grid-connected infrastructure asset do not follow the same logic. Neither do plants in different capacity bands. A sub-250 MW unit may justify a narrower intervention than a 1,000+ MW site.

Seventh, spending is allocated by region and fleet maturity. North America and Europe often focus on modernization and compliance-heavy upgrades. Asia-Pacific often combines fleet age, system growth, and reliability needs in a different mix.

Eighth, project execution is tied to outages, permitting, technical approvals, and service windows. That is why timing matters almost as much as technical scope.

Ninth, outcomes are judged on more than added years of life. Buyers look at outage reduction, operating flexibility, performance recovery, and whether capital was deferred in a sensible way.

What matters most when evaluating claims in this market

A lot of market claims sound strong until you test what is actually being measured. The weak point is usually not the engineering. It is the market boundary.

Claim type

What good proof looks like

What often goes wrong

Market size

Clear services-only scope, segment mapping, no overlap across asset and service types

Mixing service revenue with equipment sales or plant capex

Growth outlook

Forecast tied to installed base, outage cycles, retrofit need, and replacement delays

Straight-line growth based on generic power demand

Segment dominance

Defined chapter logic and mutually exclusive segment buckets

Double counting the same project in several segments

Regional demand

Country or fleet-level logic tied to asset age and grid need

Broad assumptions based on GDP or total power capacity alone

Vendor positioning

Service capability matched to real asset classes and project types

Treating all OEMs and service firms as interchangeable

Opportunity claims

Specific use cases where modernization beats replacement

Vague statements about “aging infrastructure” without decision context

The decision lens

A buyer should use a simple framework before purchasing this report.

Check the market boundary

Make sure the report is truly about life-extension services. If it blends services with new equipment sales, EPC, or full plant replacement, the numbers will be harder to use.

Test the transaction layer

Ask what exactly is being counted. Is the report measuring service revenue, project value, or a broader asset-management spend pool? Good reports stay consistent.

Compare segment logic

Review whether service type, asset type, power source, plant capacity, and region are structured without overlap. A useful report should avoid counting the same project twice under different labels.

Review the proof standard

Look for source-linked evidence behind major claims. The best reports do not just state trends. They show how those trends were validated.

Check forecasting discipline

A serious forecast should connect to fleet age, asset renewal timing, outage intervals, modernization cycles, and regional grid needs. It should not rely on generic growth language.

Ask where the report helps action

The report should support decisions on market entry, service-line prioritization, region focus, account targeting, and competitive positioning. If it cannot change a decision, it is probably too broad.

The contrarian view

The biggest mistake in this market is assuming that every aging asset creates equal demand. It does not. Some assets are old but not attractive for life extension. Others are not that old but become urgent candidates because grid conditions changed.

Another common error is mixing maintenance with life extension. Routine service is not the same as a decision to extend useful life. If a report does not separate these clearly, the market will look larger than it really is.

A third problem is hidden double counting. One project may involve a turbine overhaul, controls retrofit, engineering study, and long-term agreement. Weak market models count each element in overlapping ways and inflate demand.

There is also too much reliance on broad proxies like installed capacity or generation mix. Those are useful inputs, not sizing answers. What matters is asset condition, replacement economics, outage history, compliance pressure, and strategic importance to the grid.

The final trap is the “one-size” claim. Life extension logic is not identical across coal, gas, hydro, nuclear, renewable-linked systems, and grid infrastructure. Buyers should be wary of any report that treats them as one undifferentiated pool.

Practical implications by stakeholder

Utilities and power generators

Need to compare life extension versus replacement using asset-specific economics, not fleet-wide averages.

Benefit from segment-level visibility by service type and asset type when planning capital allocation.

OEMs and specialist service providers

Should use the report to identify where retrofit and modernization are rising faster than classic overhaul work.

Can refine account targeting by power source, plant capacity, and regional fleet maturity.

Investors and private equity

Need a clean services-only market view to assess recurring revenue potential.

Should look for where long-term service agreements create more durable value than one-off projects.

Grid operators and infrastructure managers

Gain from understanding transformer, substation, and related infrastructure life-extension demand.

Can use regional analysis to track resilience-driven modernization pressure.

Strategy and market intelligence teams

Need a report that avoids overlapping segment logic.

Should test whether the methodology can support board-level planning, not just slide-level storytelling.

UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2025 - 2030

Base Year

2025

Forecast Period

2026 - 2030

CAGR

6.9%

Segments Covered

By Service Type , Asset Type , Power Source, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

GE Vernova, Siemens Energy, Mitsubishi Power, Ansaldo Energia, Voith Group, Andritz, Sulzer, EthosEnergy, Wärtsilä, Baker Hughes, ABB, and Hitachi Energy

Market Segmentation

Utility-Scale Power Asset Life Extension Market – By Service Type

Introduction/Key Findings

Inspection & Condition Assessment

Refurbishment & Overhaul

Retrofit & Modernization

Life Assessment & Engineering Studies

Long-Term Service Agreements

Others

Y-O-Y Growth Trend & Opportunity Analysis

In 2025, based on market segmentation by service type, the Refurbishment & Overhaul segment holds the highest share of the Utility-Scale Power Asset Life Extension Market. This is primarily due to the immediate need among utilities and independent power producers to restore aging equipment performance, improve operational reliability, and avoid the significantly higher capital burden of full asset replacement.

Retrofit & Modernization is the fastest-growing segment during the forecast period. This growth is driven by the increasing need for digital controls, emissions compliance upgrades, operational flexibility, automation improvements, and grid responsiveness across aging power assets. As power systems integrate more renewable energy and utilities seek better performance from existing infrastructure, retrofit and modernization services are gaining stronger momentum than conventional overhaul work.

Utility-Scale Power Asset Life Extension Market – By Asset Type

Introduction/Key Findings

Turbines

Generators

Boilers & Heat Recovery Systems

Transformers & Substations

Balance of Plant Systems

Others

Y-O-Y Growth Trend & Opportunity Analysis

In 2025, based on market segmentation by asset type, the Turbines segment accounts for the largest share of the Utility-Scale Power Asset Life Extension Market. This dominance is mainly attributed to the central role turbines play in utility-scale power generation across thermal, hydropower, and selected renewable-linked systems. Since turbines are among the most critical and high-value assets within power plants, operators prioritize their life extension to sustain output, improve efficiency, reduce forced outages, and maintain plant reliability.

Transformers & Substations is the fastest-growing segment during the forecast period. This growth is driven by rising grid modernization requirements, increasing pressure on transmission and distribution infrastructure, long procurement lead times for new electrical equipment, and the need to improve asset reliability amid expanding renewable integration. Utilities are increasingly investing in the life extension of transformers and substations to delay replacement costs and strengthen network resilience.

Utility-Scale Power Asset Life Extension Market – By Power Source

Introduction/Key Findings

Coal-Fired Power Plants

Gas-Fired Power Plants

Nuclear Power Plants

Hydropower Plants

Utility-Scale Renewable Power Assets

Others

Y-O-Y Growth Trend & Opportunity Analysis

Regional Segmentation

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

Asia-Pacific is the dominant region in the global utility-scale power asset life extension market. The region leads due to its vast installed base of utility-scale thermal, hydro, and grid infrastructure assets, many of which are entering mid-life or late-life operating phases while still remaining strategically important for energy security. Countries such as China, India, Japan, South Korea, and several Southeast Asian nations continue to rely on existing large-scale generation fleets to support industrial demand growth, urbanization, and grid stability. At the same time, utilities across the region are under pressure to improve efficiency, reduce forced outages, and align legacy assets with evolving environmental standards rather than retire them immediately.

Latest Market News

March 3, 2026 — GE Vernova Expands Electrification Manufacturing in Italy GE Vernova announced an approximately USD 30 million investment to expand its electrification manufacturing facility in Sesto San Giovanni, Italy, to support rising global demand for grid infrastructure. The move is relevant to the Utility-Scale Power Asset Life Extension Market because stronger electrification and grid equipment capacity supports substation upgrades, retrofit programs, and long-life utility infrastructure strategies.

November 6, 2025 — South Africa Approves 20-Year Extension for Koeberg Unit 2 South Africa’s National Nuclear Regulator authorized the 930 MWe Koeberg Unit 2 for a further 20 years of operation. The decision highlights how regulatory approval for extended plant operation can directly sustain demand for asset assessment, refurbishment, safety upgrades, and long-term life extension services in utility-scale power systems.

April 30, 2025 — Nordic Investment Bank Backs Olkiluoto Nuclear Upgrades The Nordic Investment Bank signed a EUR 75 million loan agreement with Teollisuuden Voima Oyj to finance safety upgrades at units 1 and 2 of Finland’s Olkiluoto nuclear power plant. The financing points to continued investment in modernization and safety-linked upgrade programs that extend the operating viability of large baseload generation assets.

April 1, 2025 — Turbine Supply Crunch Strengthens Case for Extending Existing Assets POWER reported that a gas turbine supply crunch was unfolding as utilities sought new capacity, forcing procurement delays and planning adjustments. For the Utility-Scale Power Asset Life Extension Market, this is important because constrained access to new turbine supply can push utilities toward refurbishment, overhaul, and modernization of existing generating assets instead of full replacement.

March 17, 2025 — Belgium Finalizes Reactor Restart and Lifetime Extension Framework Belgium finalized arrangements tied to the 10-year lifetime extension of Doel 4 and Tihange 3, two reactors providing 2 GWe of capacity. The development reinforces the role of policy-backed lifetime extensions in supporting engineering upgrades, maintenance planning, and major refurbishment programs across aging utility-scale nuclear assets.

December 6, 2024 — Axpo Commits New Investment to Keep Beznau Running Beyond 60 Years Swiss utility Axpo announced plans to invest a further CHF 350 million to enable the Beznau nuclear power plant to operate until 2033. This is a clear example of capital being directed toward long-duration life extension for mature baseload assets, with direct implications for modernization, inspection, and safety enhancement service demand.

May 31, 2024 — Fortum Awards Loviisa Turbine Modernization Contract Fortum awarded Doosan Škoda Power a contract to modernize the low-pressure turbines at the Loviisa nuclear power plant in Finland as part of lifetime extension-related investments. The project is expected to increase the plant’s total capacity by about 38 MWe, showing how life extension spending can also deliver measurable output gains rather than only preserving operations.

Key Players

GE Vernova

Siemens Energy

Mitsubishi Power

Ansaldo Energia

Voith Group

Andritz

Sulzer

EthosEnergy

Wärtsilä

Baker Hughes

Questions buyers ask before purchasing this report

What exactly counts as life extension in this market?

In this report, life extension means paid services that increase or preserve the useful operating life of utility-scale power assets beyond routine maintenance. That includes inspection and condition assessment, refurbishment and overhaul, retrofit and modernization, life assessment and engineering studies, and long-term service agreements tied to life-management outcomes. It does not include greenfield construction, full asset replacement, routine O&M, or fuel supply. That distinction matters because many market estimates get inflated by bundling unrelated spending into the same number.

Does this report cover equipment sales or only services?

The useful way to frame this market is services-only. Buyers usually need to know where service revenue sits, not a blended figure that mixes equipment sales, replacement capex, and lifecycle service contracts. A services-only boundary makes vendor comparison cleaner and helps commercial teams assess where spending is actually contestable. It also reduces double counting. If a report mixes transaction layers, it becomes harder to use for pricing strategy, partner selection, or regional market prioritization.

How is this market different from general power plant services?

General power plant services can include everyday maintenance, inspections, spare-parts support, and broad plant support activity. The Utility-Scale Power Asset Life Extension Market is narrower and more strategic. It focuses on projects and contracts intended to extend usable life, restore performance, improve controls, reduce risk, or avoid near-term replacement. That distinction is not cosmetic. It changes which buyers matter, which budgets are tapped, and which vendors are really competing for the same work.

Which segments matter most for a buyer evaluating this report?

The most useful segment cuts are service type, asset type, power source, plant capacity, and region. Those dimensions reflect how real buying decisions are made. Service type shows where the money goes. Asset type shows what is being worked on. Power source reflects operating context. Plant capacity affects project scale and economics. Region captures differences in fleet age, regulation, and grid conditions. A report that uses these lenses well is more practical than one built around broad labels that do not match procurement behavior.

How can I tell if the forecast is realistic?

A realistic forecast should connect to the installed base, asset age, refurbishment cycles, outage schedules, modernization intensity, and replacement delays. It should also reflect that not every old asset becomes a life-extension project. The best forecasts are grounded in operational logic, not broad assumptions about energy demand or infrastructure spending. Buyers should look for consistency between segment-level trends and the real conditions that trigger spending. If the growth story sounds smooth everywhere, that is usually a warning sign.

Will this report help with market entry or account prioritization?

Yes, if it is structured properly. A good report should show where demand is strongest by service type, asset type, region, and operating context. That helps vendors decide whether to lead with overhaul, modernization, engineering studies, or long-term agreements. It also helps identify which customer types are likely to buy first and which geographies have the right fleet profile. For market entry, the report is most useful when it links demand patterns to actual buying conditions rather than generic industry language.

Why do reports in this market often disagree with each other?

They usually disagree because they define the market differently. One report may count only service revenue. Another may include replacement equipment, plant upgrades, or broader asset-management spending. Some also double count projects that span several service lines. Regional assumptions can vary as well. That is why methodology matters as much as the final number. Buyers should not ask only which report has the biggest estimate. They should ask which report has the cleanest scope, strongest validation, and most usable structure.

Is regional analysis really important for this market?

Yes, because this market is shaped by regional fleet realities more than by generic global averages. Asset age, regulation, replacement economics, outage practices, service ecosystems, and grid reliability needs vary a lot across regions. A plant owner in North America may be solving a different problem than one in Asia-Pacific or Europe, even if the asset class looks similar on paper. Regional analysis helps buyers avoid false comparisons and identify where service models, pricing, and project timing are most attractive.

To Learn more about this report,

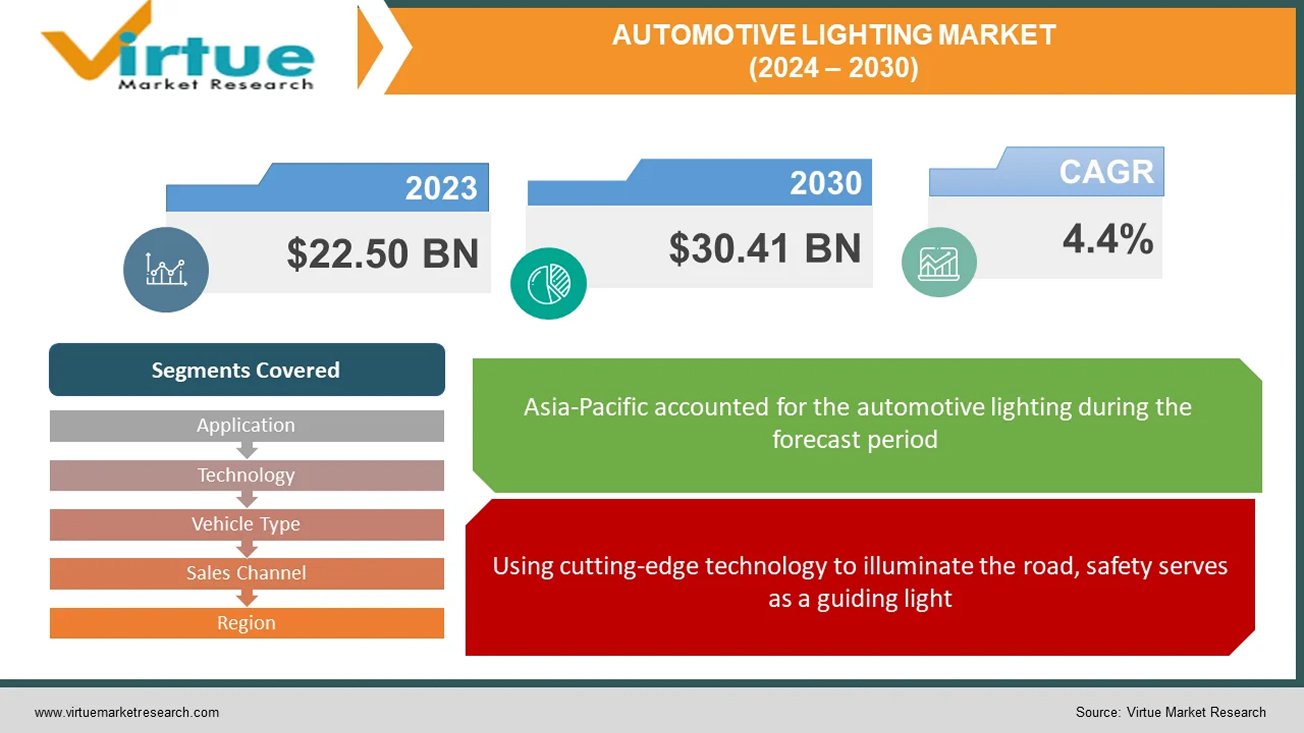

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

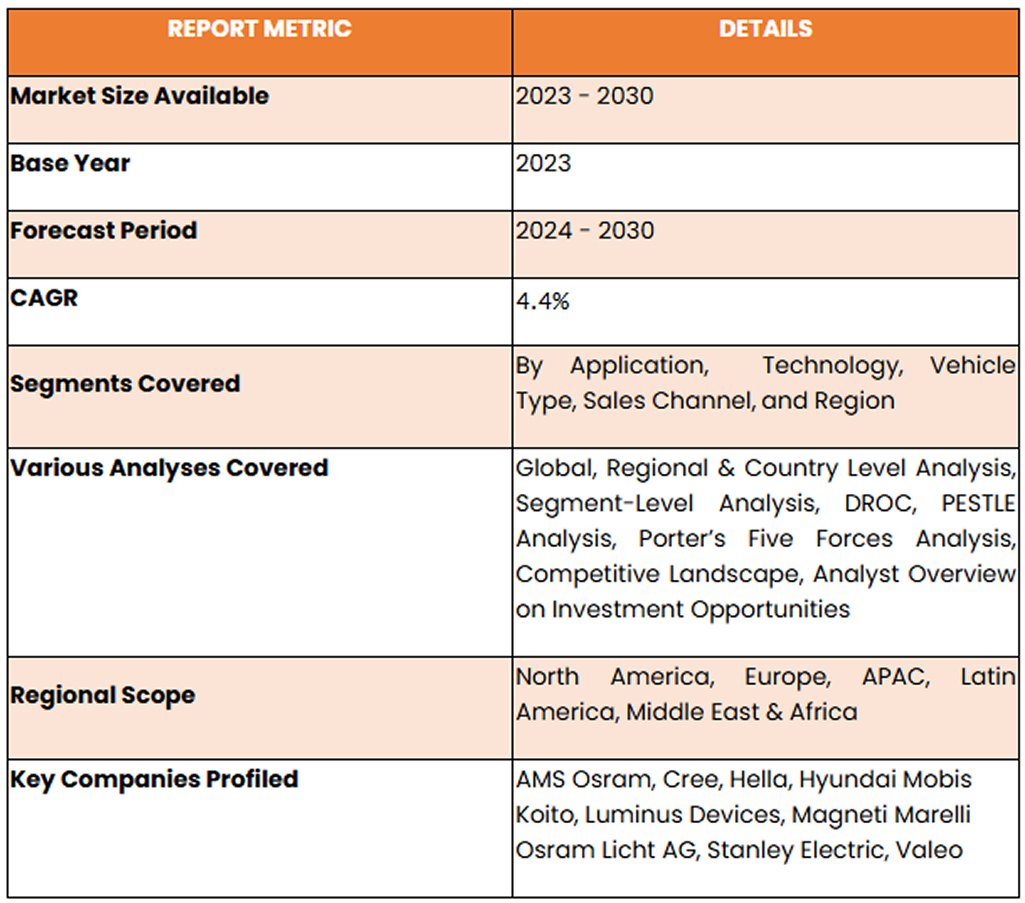

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

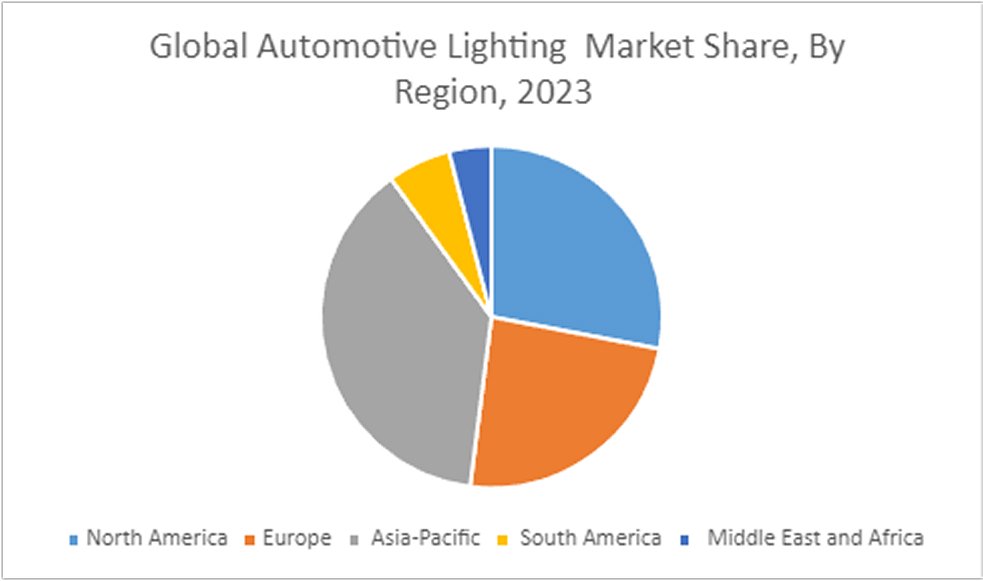

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – SCOPE & METHODOLOGY

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Source

1.5. Secondary Source

Chapter 2. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – EXECUTIVE SUMMARY

2.1. Market Size & Forecast – (2026 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – COMPETITION SCENARIO

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Packaging SERVICE TYPE Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET - ENTRY SCENARIO

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Players

4.5.6. Threat of Substitutes

Chapter 5. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET - LANDSCAPE

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – By Service Type

6.1 Introduction/Key Findings

6.2 Inspection & Condition Assessment

6.3 Refurbishment & Overhaul

6.4 Retrofit & Modernization

6.5 Life Assessment & Engineering Studies

6.6 Long-Term Service Agreements

6.7 Others

6.8 Y-O-Y Growth trend Analysis By Service Type

6.9 Absolute $ Opportunity Analysis By Service Type , 2026-2030

Chapter 7. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – By Asset Type

7.1 Introduction/Key Findings

7.2 Turbines

7.3 Generators

7.4 Boilers & Heat Recovery Systems

7.5 Transformers & Substations

7.6 Balance of Plant Systems

7.7 Others

7.8 Y-O-Y Growth trend Analysis By Asset Type

7.9 Absolute $ Opportunity Analysis By Asset Type, 2026-2030

Chapter 8. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – By Power Source

8.1 Introduction/Key Findings

8.2 Coal-Fired Power Plants

8.3 Gas-Fired Power Plants

8.4 Nuclear Power Plants

8.5 Hydropower Plants

8.6 Utility-Scale Renewable Power Assets

8.7 Others

8.8 Y-O-Y Growth trend Analysis Power Source

8.9 Absolute $ Opportunity Analysis Power Source , 2026-2030

Chapter 9. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET, BY GEOGRAPHY – MARKET SIZE, FORECAST, TRENDS & INSIGHTS

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Service Type

9.1.3. By Power Source

9.1.4. By Asset Type mode

9.1.5. Countries & Segments - Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Service Type

9.2.3. By Power Source

9.2.4. By Asset Type mode

9.2.5. Countries & Segments - Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Service Type

9.3.3. By Power Source

9.3.4. By Asset Type mode

9.3.5. Countries & Segments - Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Power Source

9.4.3. By Asset Type mode

9.4.4. By Service Type

9.4.5. Countries & Segments - Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Power Source

9.5.3. By Service Type

9.5.4. By Asset Type mode

9.5.5. Countries & Segments - Market Attractiveness Analysis

Chapter 10. UTILITY-SCALE POWER ASSET LIFE EXTENSION MARKET – Company Profiles – (Overview, UTILITY-SCALE POWER ASSET LIFE EXTENSION Service Type Portfolio, Financials, Strategies & Developments)

10.1 GE Vernova

10.2 Siemens Energy

10.3 Mitsubishi Power

10.4 Ansaldo Energia

10.5 Voith Group

10.6 Andritz

10.7 Sulzer

10.8 EthosEnergy

10.9 Wärtsilä

10.10 Baker Hughes

Fill out the form below and our team will get back to you shortly

FAQ's

The market was valued at USD 18.4 billion in 2025 and is projected to reach USD 25.5 billion by 2030, growing at a CAGR of 6.9% during 2026–2030.

The market was valued at USD 18.4 billion in 2025 and is projected to reach USD 25.5 billion by 2030, growing at a CAGR of 6.9% during 2026–2030.

The market was valued at USD 18.4 billion in 2025 and is projected to reach USD 25.5 billion by 2030, growing at a CAGR of 6.9% during 2026–2030.

The main drivers are the aging global utility asset base and the growing need for grid reliability, flexibility, and cost-efficient modernization of existing power infrastructure.

The main drivers are the aging global utility asset base and the growing need for grid reliability, flexibility, and cost-efficient modernization of existing power infrastructure.

The main drivers are the aging global utility asset base and the growing need for grid reliability, flexibility, and cost-efficient modernization of existing power infrastructure.

The market is segmented by product into Turbine and Generator Life Extension, and Boiler and Balance-of-Plant Life Extension; by application into Thermal Power Plants, Hydropower Plants, Renewable Power Assets, Nuclear Power Plants, and Grid-Connected Utility Infrastructure.

The market is segmented by product into Turbine and Generator Life Extension, and Boiler and Balance-of-Plant Life Extension; by application into Thermal Power Plants, Hydropower Plants, Renewable Power Assets, Nuclear Power Plants, and Grid-Connected Utility Infrastructure.

The market is segmented by product into Turbine and Generator Life Extension, and Boiler and Balance-of-Plant Life Extension; by application into Thermal Power Plants, Hydropower Plants, Renewable Power Assets, Nuclear Power Plants, and Grid-Connected Utility Infrastructure.

Asia-Pacific is the dominant region due to its large installed base of aging power assets, rising electricity demand, and strong need for affordable modernization.

Asia-Pacific is the dominant region due to its large installed base of aging power assets, rising electricity demand, and strong need for affordable modernization.

Asia-Pacific is the dominant region due to its large installed base of aging power assets, rising electricity demand, and strong need for affordable modernization.

Leading players include GE Vernova, Siemens Energy, Mitsubishi Power, Ansaldo Energia, Voith Group, Andritz, Sulzer, EthosEnergy, Wärtsilä, Baker Hughes, ABB, and Hitachi Energy.

Leading players include GE Vernova, Siemens Energy, Mitsubishi Power, Ansaldo Energia, Voith Group, Andritz, Sulzer, EthosEnergy, Wärtsilä, Baker Hughes, ABB, and Hitachi Energy.

Leading players include GE Vernova, Siemens Energy, Mitsubishi Power, Ansaldo Energia, Voith Group, Andritz, Sulzer, EthosEnergy, Wärtsilä, Baker Hughes, ABB, and Hitachi Energy.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19366 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the HVDC Transmission Systems Market was valued at approximately USD 13.84 Billion. It is projected to grow at a CAGR of around 7.7% during the forecast period of 2026–2030, reaching an estimated USD 20.05 Billi...

Report Code: VMR-19364 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Reactive Power Compensation Market was valued at approximately USD 8.14 Billion. It is projected to grow at a CAGR of around 8.3% during the forecast period of 2026–2030, reaching an estimated USD 12.13 Bill...

Report Code: VMR-19363 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Microgrid Controllers & Integration Services Market was valued at approximately USD 5.84 Billion. It is projected to grow at a CAGR of around 9.8% during the forecast period of 2026–2030, reaching an estimat...

Report Code: VMR-19318 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the Grid Protection & Control Systems Market was valued at approximately USD 109.7 Billion. It is projected to grow at a CAGR of around 8% during the forecast period of 2026–2030, reaching an estimated USD 161.1...

Report Code: VMR-19314 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the AI Model Monitoring and Guardrails Market was valued at approximately USD 2,140 million. It is projected to grow at a CAGR of around 8.40% during the forecast period of 2026–2030, reaching an estimated USD 3...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”