United Kingdom Virtual Wards and Hospital-at-Home Technology Market Research Report – Segmented by Technology Component (Remote Patient Monitoring (RPM) Platforms, Virtual Care & Telehealth Platforms, Care Coordination & Workflow Management Software, Clinical Decision Support & AI Analytics Solutions, Medical Devices & Connected Monitoring Equipment, Others); by Care Model (Acute Virtual Wards, Step-Down/Post-Discharge Virtual Wards, Admission Avoidance Hospital-at-Home Programs, Rehabilitation-at-Home Programs, Palliative & End-of-Life Virtual Care Programs, Others); by Clinical Use Case (Respiratory Conditions, Cardiovascular Conditions, Frailty & Elderly Care, Post-Surgical Recovery, Oncology Care, Infectious Diseases, Chronic Disease Management, Others); by Healthcare Provider Type (NHS Acute Hospital Trusts, Community Healthcare Providers, Integrated Care Systems (ICSs), Mental Health & Specialist Trusts, Independent Healthcare Providers, Others); by Deployment Model (Cloud-Based Solutions, Hybrid Deployment Solutions, On-Premises Solutions, Others); and Region - Size, Share, Growth Analysis | Forecast (2026– 2030)

United Kingdom Virtual Wards and Hospital-at-Home Technology Market Size (2026-2030)

The United Kingdom Virtual Wards and Hospital-at-Home Technology Market was valued at approximately USD 412.6 Million. It is projected to grow at a CAGR of around 15.5% during the forecast period of 2026–2030, reaching an estimated USD 848.08 Million by 2030.

The United Kingdom Virtual Wards and Hospital-at-Home Technology Market includes digital technology that allows healthcare services to be delivered to patients at home at a hospital level or under clinically managed care rather than in hospital settings. What is on offer is a range of software platforms, remote monitoring solutions, virtual care technologies, data analytics, and digital infrastructure that facilitate the management of patient pathways virtually. It does not include any income generated from the traditional hospital stays, home care services that are not technology-related, or general healthcare delivery that is not part of virtual ward systems.

The market has become more than just a capacity-management response; it has become a more well-defined part of the healthcare delivery system. With the development of real-time monitoring, data analysis, and streamlined care management, healthcare providers are increasingly embedding remote care into their day-to-day workflows. There is a greater focus on optimizing patient flow, early intervention, minimizing unnecessary hospital use, and having clinical control. Consequently, technology deployments are moving away from single digital products toward platforms that enable scalability, interoperability, and efficiency.

The market is a hub for healthcare transformation and resource optimization for decision-makers. Long-term integration, cyber resilience, clinical workflow integration, and ROI are becoming major priorities in procurement. When organisations consider this market, the factors they need to take into account include the need to meet current operational demands and the future care delivery needs they have, alongside selection, deployment, and ecosystem partnerships in order to ensure the successful growth of virtual care in the United Kingdom.

Key Market Insights

BCG's new front end, due to be released in 2026, will reduce costs and workload.

KPMG recommends that those hospital-at-home groups that are ready for 2026 scale carefully and selectively.

By 2035, providers will be moving to decentralize care with AI, according to PwC.

IBM discovered that 13% of organizations were compromised in AI models or applications.

97% of AI incidents were found to be due to the lack of access controls, according to IBM.

According to IBM, 14% of healthcare security teams are staffed to the fullest.

AI assistants will help monitor and support home care and surgery, KPMG said.

Virtual wards cost the system in 2025, unless they release beds.

65% find virtual care easier than face-to-face care.

Deloitte reports virtual visits rose from 42% to 44% in 2024.

Twenty-four percent would change doctors if they had the option to see them virtually, meaning there will be even more competition in the physician's office.

BCG's noted areas for growth included 2024 at-home care, virtual wards, and remote diagnostics.

Care@Home requires reconfigured devices, since home is not a hospital, says Accenture.

Accenture associates value-based care stress with decreased-cost home treatment models.

Research Methodology

Scope & Definitions

Market scope covers technology revenue generated from virtual wards and hospital-at-home platforms, remote patient monitoring solutions, care coordination software, clinical decision support tools, and connected monitoring devices deployed across the United Kingdom.

Excludes conventional inpatient hospital services, home nursing service revenue, and non-digital community care.

Analysis covers the United Kingdom with historical, base-year, and forecast assessments using standardized segmentation, inclusion criteria, and a documented data dictionary to prevent overlap and double counting.

Evidence Collection (Primary + Secondary)

Primary research included interviews across NHS trusts, integrated care systems, technology vendors, device manufacturers, digital health specialists, clinicians, procurement stakeholders, and industry experts.

Secondary research utilized publications from NHS England, UK Department of Health and Social Care, Office for National Statistics, company reports, investor filings, peer-reviewed literature, and relevant regulators/standards bodies/industry associations specific to the market (named in-report).

Key findings are supported by verifiable sources and source-linked evidence within the report.

Triangulation & Validation

Market estimates were developed using bottom-up and top-down methodologies and reconciled against financial disclosures where available.

Conflicting inputs were resolved through multi-source validation, interview cross-checking, and consistency testing to minimize bias.

Presentation & Auditability

All assumptions, calculations, segmentation rules, and source references are documented for traceability.

Findings are presented through auditable tables, forecasts, and evidence-backed insights suitable for decision-grade analysis.

United Kingdom Virtual Wards and Hospital-at-Home Technology Market Drivers

Healthcare providers are focusing on more capacity building using digital means.

In the UK, technology-based care models are becoming a key solution for healthcare providers to cope with the growing demands on services without necessarily building more physical facilities. Virtual care environments help to maximize the utilization of resources and provide ongoing monitoring of patient care. This transformation is driving more investments in connected monitoring, workflow automation, and digitally coordinated care pathways that are helping to make healthcare operations more efficient.

Intelligent clinical workflows are transforming how patients are managed remotely.

Increasing focus on automation in healthcare service delivery is fueling the growth of advanced clinical workflow technologies. Advances in clinical workflow technologies are driving adoption, as healthcare delivery is increasingly focused on automation. Healthcare organizations are looking for systems that simplify the way the patient is monitored, prioritize interventions, and decrease administrative work for care teams. As virtual care programs evolve, intelligent coordination platforms are indispensable for patient management operations that are scalable, efficient, and responsive.

The pace of technology decisions to modernize integrated care is rapidly increasing.

The process of healthcare modernization is driving increased interoperability between care settings, leading to a need for technologies that enable the smooth flow of information and help manage patient data. Decision-makers are increasingly looking for digital platforms that enable them to bring the clinical teams together and monitor the environment and care pathways. This is making technology an enabling platform for future-ready healthcare delivery.

United Kingdom Virtual Wards and Hospital-at-Home Technology Market Restraints

Leaders in the healthcare sector continue to face a myriad of challenges that hinder the growth of virtual care, such as a lack of skilled staff, patient engagement, a disjointed digital landscape, and intricate data-sharing needs. Large-scale deployments can be challenging due to budget constraints, and interoperability issues can add to the operational risk, as can cybersecurity concerns. Achieving a balance between innovation, clinical governance, scalability, and sustainable uptake is increasingly vital to the market's journey.

United Kingdom Virtual Wards and Hospital-at-Home Technology Market Opportunities

There are opportunities for hospital delivery to be extended outside walls, in integrated monitoring ecosystems, predictive clinical intelligence, workforce optimization tools, and scalable digital care pathways. The technologies, partnerships, and services are evolving across the country as a response to the growing demand for proactive chronic disease management, quick discharge coordination, and individualized home-based interventions.

How this market works end-to-end

Patient Identification

Eligible patients are identified for acute virtual wards, rehabilitation-at-home programs, chronic disease management, or post-discharge monitoring.

Clinical Assessment

Care teams evaluate clinical suitability, risk levels, monitoring requirements, and escalation protocols.

Technology Selection

Providers deploy remote patient monitoring platforms, connected devices, and virtual care software based on pathway needs.

Device Deployment

Monitoring equipment is installed and configured for patient use at home.

Data Collection

Connected devices continuously collect physiological and clinical information.

Workflow Coordination

Care coordination platforms route alerts, tasks, and communications across multidisciplinary teams.

Clinical Monitoring

Healthcare professionals review patient data using virtual care and command-center environments.

Escalation Management

Clinical decision support tools identify deterioration risks and trigger intervention workflows.

Care Transition

Patients move from acute monitoring into recovery, rehabilitation, community care, or discharge.

Performance Evaluation

Providers assess utilization, outcomes, operational efficiency, and technology effectiveness.

Why this market matters now

The strategic question is no longer whether healthcare can be delivered at home. The question is how to scale it safely, efficiently, and sustainably.

NHS organizations continue to face capacity constraints, workforce pressures, and growing demand complexity. Virtual wards offer a pathway to expand care delivery without relying solely on additional physical beds.

However, scaling introduces new risks. Technology fragmentation can create operational inefficiencies. Cybersecurity threats increase as more connected devices and cloud platforms enter clinical environments. Procurement decisions made today may shape operational flexibility for years.

As virtual wards mature, buyers must evaluate not only technology functionality but also interoperability, workflow integration, clinical governance, and vendor resilience.

What matters most when evaluating claims in this market

Claim type

What good proof looks like

What often goes wrong

Capacity improvement

Operational deployment evidence across care pathways

Assuming pilots represent scaled performance

Cost reduction

Documented workflow and utilization outcomes

Ignoring implementation costs

Clinical effectiveness

Real-world patient monitoring results

Overreliance on small studies

Platform scalability

Multi-site deployment experience

Confusing deployments with active utilization

Cybersecurity readiness

Established governance and security controls

Treating compliance as security

Integration capability

Proven interoperability across systems

Assuming APIs guarantee integration

The decision lens

1. Define Care Objectives

Identify whether goals focus on admission avoidance, step-down care, rehabilitation, or chronic disease management.

2. Validate Workflow Fit

Compare technology capabilities against actual clinical workflows rather than feature lists.

3. Assess Integration Risk

Review interoperability requirements across electronic records, monitoring systems, and operational platforms.

4. Stress-Test Scalability

Evaluate whether solutions perform beyond pilot environments and support wider deployment.

5. Examine Cyber Resilience

Verify governance, security controls, monitoring processes, and incident response readiness.

6. Compare Vendor Stability

Assess long-term product investment, implementation support, and ecosystem partnerships.

7. Monitor Timing Signals

Track procurement priorities, funding visibility, workforce constraints, and operational pressures.

The contrarian view

A common mistake is treating virtual wards as a device market. In practice, workflow orchestration often creates more value than hardware.

Another error is using patient monitoring volumes as a proxy for market maturity. Large deployments do not automatically indicate operational success.

Many analyses also double count technology categories by combining software, devices, services, and care delivery revenues within the same estimate.

Perhaps the biggest misconception is assuming every clinical pathway benefits equally from virtual ward deployment. Suitability varies significantly across patient groups and care models.

Practical implications by stakeholder

NHS Trusts

Prioritize interoperability and operational scalability.

Evaluate long-term workforce implications.

Integrated Care Systems

Align virtual ward investments across regional care pathways.

Reduce fragmentation between providers.

Technology Vendors

Demonstrate workflow outcomes, not just technical features.

Strengthen integration capabilities.

Device Manufacturers

Focus on usability and deployment efficiency.

Support secure data exchange.

Community Healthcare Providers

Prepare for expanded monitoring responsibilities.

Coordinate closely with acute care teams.

Healthcare Investors

Monitor platform adoption and ecosystem consolidation.

Assess vendor positioning within NHS procurement priorities.

UNITED KINGDOM VIRTUAL WARDS AND HOSPITAL-AT-HOME TECHNOLOGY MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2025 - 2030

Base Year

2025

Forecast Period

2026 - 2030

CAGR

15.5%

Segments Covered

By Technology Component , Care Model , Clinical Use Case , Healthcare Provider Type , Deployment Model , and Region

Various Analyses Covered

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

Europe, UK

Key Companies Profiled

Doccla, Huma, Graphnet Health, Docobo Ltd, Inhealthcare, Feebris, Philips Healthcare, Masimo, Dignio, BT Group, Current Health (Best Buy Health), Lenus Health, Cera Care, The Access Group, and Luscii (Omron Healthcare).

United Kingdom Virtual Wards and Hospital-at-Home Technology Market Segmentation

United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Technology Component

Introduction/Key Findings

Remote Patient Monitoring (RPM) Platforms

Virtual Care & Telehealth Platforms

Care Coordination & Workflow Management Software

Clinical Decision Support & AI Analytics Solutions

Medical Devices & Connected Monitoring Equipment

Others

Y-O-Y Growth Trend & Opportunity Analysis

In 2026, Remote Patient Monitoring (RPM) Platforms accounted for more than one-quarter of the technology component share, bolstered by the constant demand for patient monitoring, real-time vital-signs tracking, and their broad adoption in virtual wards within the NHS.

The Clinical Decision Support & AI Analytics Solutions technology is the fastest-growing segment with a projected 24.7% CAGR from 2021 to 2030. Providers are looking for predictive insights, automated risk stratification, and intervention planning, driving demand.

United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Care Model

Introduction/Key Findings

Acute Virtual Wards

Step-Down/Post-Discharge Virtual Wards

Admission Avoidance Hospital-at-Home Programs

Rehabilitation-at-Home Programs

Palliative & End-of-Life Virtual Care Programs

Others

Y-O-Y Growth Trend & Opportunity Analysis

In 2026, acute virtual wards had the highest level of care model usage, at 34.6 percent, driven by increased capacity management, inpatient avoidance strategies, and better use of healthcare delivery networks.

The CAGR for Admission Avoidance Hospital-at-Home Programs is expected to be 25.3% up to 2030. These models are becoming more popular in the healthcare industry as a way to decrease admissions, make better use of resources, and enhance patient satisfaction.

United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Clinical Use Case

Introduction/Key Findings

Respiratory Conditions

Cardiovascular Conditions

Frailty & Elderly Care

Post-Surgical Recovery

Oncology Care

Infectious Diseases

Chronic Disease Management

Others

Y-O-Y Growth Trend & Opportunity Analysis

United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Healthcare Provider Type

Introduction/Key Findings

NHS Acute Hospital Trusts

Community Healthcare Providers

Integrated Care Systems (ICSs)

Mental Health & Specialist Trusts

Independent Healthcare Providers

Others

Y-O-Y Growth Trend & Opportunity Analysis

United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Deployment Model

Introduction/Key Findings

Cloud-Based Solutions

Hybrid Deployment Solutions

On-Premises Solutions

Others

Y-O-Y Growth Trend & Opportunity Analysis

United Kingdom Virtual Wards and Hospital-at-Home Technology Market– Regional Analysis

The regional lead was 78% for England, thanks to its wide rollout in the NHS's virtual wards, its advanced digital infrastructure, and national adoption across acute and community care settings.

The highest regional market share is from Scotland, with 10% growth and showing signs of accelerating adoption. Investment in the digital modernization of healthcare, remote monitoring, and integrated care delivery models remains robust, bolstering long-term growth prospects.

Latest Market News

On 18 March NHS England announced that virtual ward services are continuing to run on over 10,000 virtual beds, with systems expected to be 80% or more filled under planning guidance for 2025/26. The update further reinforced the importance of remote monitoring and hospital-at-home pathways for both adults and pediatrics.

Health and social care providers are set to benefit from a strategic partnership between Septiscience, maker of Graphnet Health, and Luscii, which will enable them to access Graphnet Remote Monitoring across 20 NHS Integrated Care Systems, covering around 17 million people. The platform already had over 75,000 NHS patients and over 400,000 patients in Europe.

On 14th August 2025, NHS England published July 2025 virtual ward capacity figures, which is the latest in ongoing monitoring of virtual ward occupancy and usage levels in integrated care systems (ICS). The program continued to be in line with planning targets for both adult and children's services and had a planned occupancy of over 80%.

Capacity for June 2025 virtual wards has been published by NHS England, marking the ongoing growth of capacity within local health systems. The guidance highlighted the need to match the priorities for neighborhood health in 2025/26 and to support admission avoidance and early discharge pathways.

NSH England published March 2025 virtual ward performance statistics within its national monitoring framework on the 10th of April 2025. The program remained in place, providing care delivery beyond hospitals, despite operating beyond occupancy targets of > 80% and the need to sustain long-term capacity growth targets.

The Scottish Government announced a target of increasing the capacity of Hospital at Home services by 2,000 beds by the end of 2026 with an extra £100m investment. The goal of the program is to improve the delivery of acute care at home and decrease delayed hospital discharge.

In October 2024, Northamptonshire Integrated Care Board (NICB) recorded 42.5 virtual ward beds per 100,000 people, NHS virtual ward occupancy data revealed. Five other ICBs had between 30.6 and 35.1 beds per 100,000 residents.

On 16th May 2024, NHS England published that the use of virtual wards saved around 9,000 hospital admissions in the South East over the last 12 months. The program was helping to promote wider use of virtual care and facilitate patient flow and de-escalate physical hospital capacity.

Key Players

Doccla

Huma

Graphnet Health

Docobo Ltd

Inhealthcare

Feebris

Philips Healthcare

Masimo

Dignio

BT Group

Questions buyers ask before purchasing this report

How mature is the United Kingdom virtual wards technology market?

Market maturity varies across technologies, care pathways, and provider types. Some virtual ward models have moved into routine operations, while others remain at earlier deployment stages. Buyers need visibility into where adoption is accelerating, which technologies are becoming standard, and where operational barriers continue to limit scale.

Which technology categories are attracting the most attention?

Buyer focus increasingly extends beyond monitoring devices. Care coordination software, workflow orchestration tools, clinical decision support platforms, and integrated virtual care systems are receiving growing attention because they directly influence operational effectiveness and scalability.

What risks should procurement teams evaluate?

Procurement teams should assess interoperability limitations, cybersecurity exposure, implementation complexity, vendor concentration, and scalability constraints. Technology selection decisions often create long-term operational dependencies that become difficult to reverse.

How important is deployment model selection?

Deployment choices influence security, integration complexity, implementation speed, operational flexibility, and future expansion opportunities. The optimal model depends on organizational priorities, infrastructure readiness, and governance requirements.

Which care pathways are creating the strongest demand?

Demand is strongest where providers can improve capacity utilization, support admission avoidance, accelerate discharge pathways, and manage chronic conditions more effectively. However, suitability differs significantly across patient populations and clinical objectives.

What separates successful virtual ward deployments from unsuccessful ones?

Success typically depends on workflow design, clinical governance, staff engagement, escalation management, and technology integration. Organizations that focus only on device deployment often struggle to achieve expected operational outcomes.

How should buyers evaluate vendor positioning?

Buyers should examine implementation capabilities, integration experience, product roadmap strength, cybersecurity maturity, and long-term commitment to healthcare markets. Feature comparisons alone rarely provide a complete picture.

Why is market intelligence important now?

Decision-makers face evolving procurement priorities, changing care delivery models, growing cybersecurity expectations, and increasing operational pressure. Reliable market intelligence helps reduce uncertainty, identify emerging risks, and improve strategic planning decisions.

To Learn more about this report,

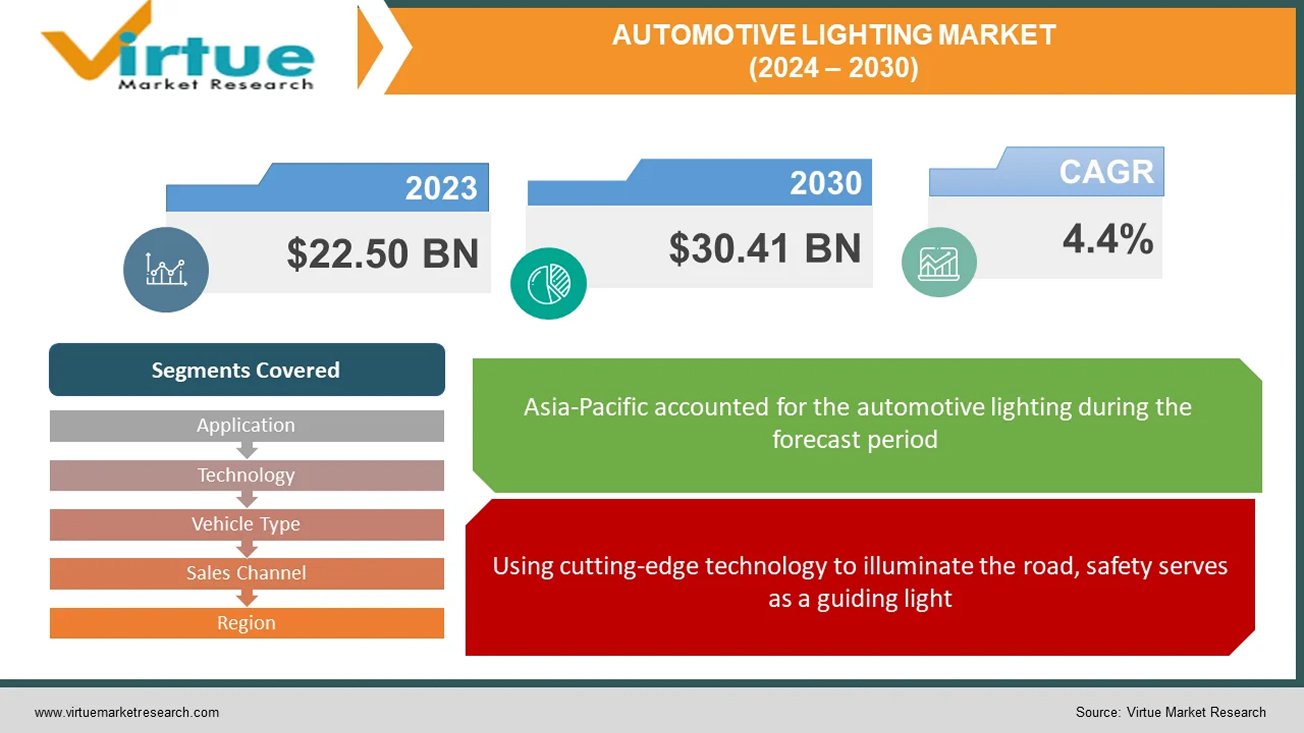

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

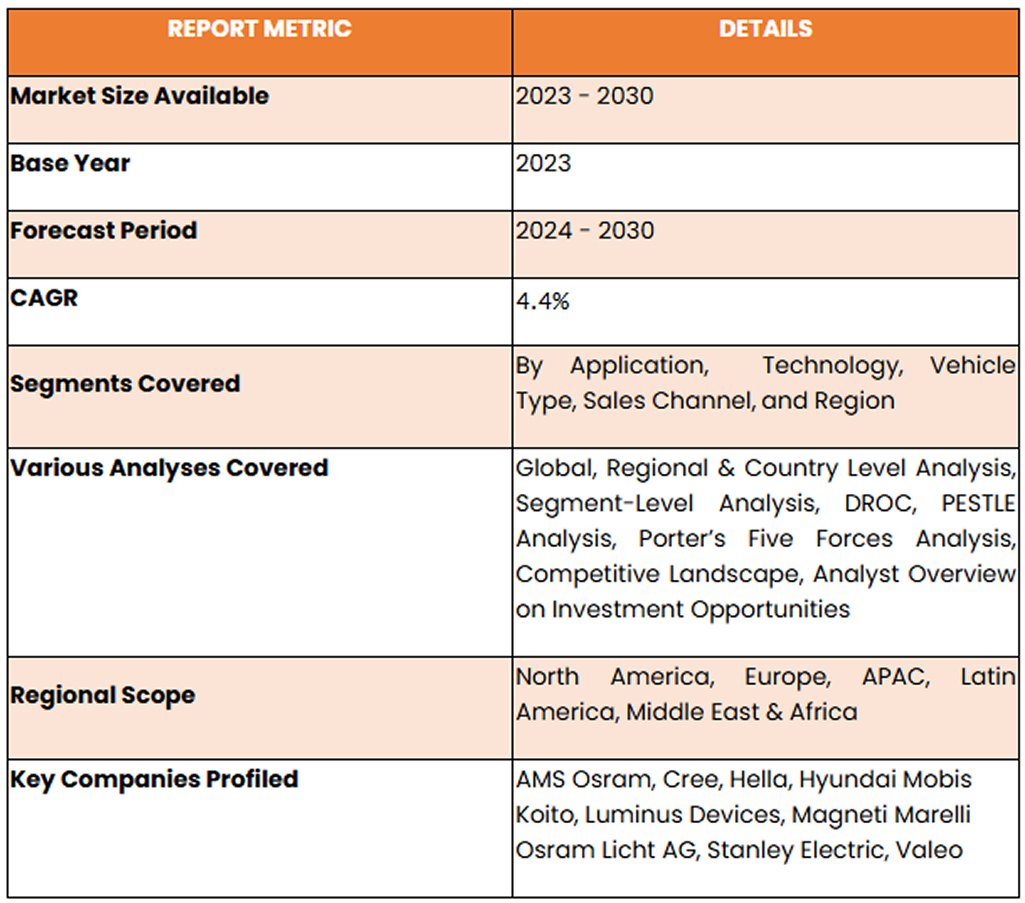

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

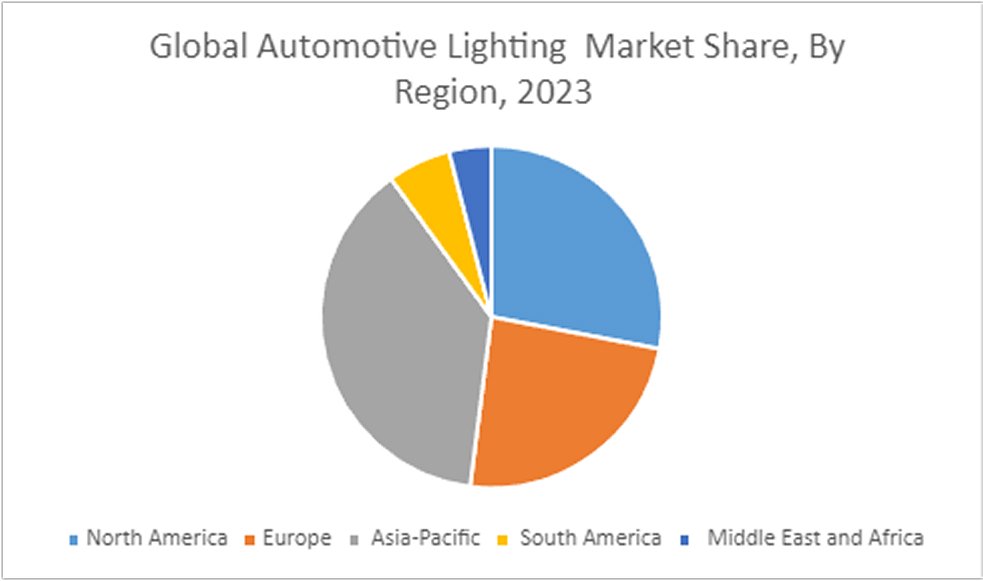

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – SCOPE & METHODOLOGY

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Source

1.5. Secondary Source Chapter 2. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – EXECUTIVE SUMMARY

2.1. Market Size & Forecast – (2026 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis Chapter 3. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – COMPETITION SCENARIO

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Packaging TESTING TYPE Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis Chapter 4. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET - ENTRY SCENARIO

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Players

4.5.6. Threat of Substitutes Chapter 5. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET - LANDSCAPE

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities Chapter 6. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – By Clinical Workflow Function

6.1 Introduction/Key Findings

6.2 Remote Patient Monitoring (RPM) Platforms

6.3 Virtual Care & Telehealth Platforms

6.4 Care Coordination & Workflow Management Software

6.5 Clinical Decision Support & AI Analytics Solutions

6.6 Medical Devices & Connected Monitoring Equipment

6.7 Others

6.8 Y-O-Y Growth trend Analysis By Clinical Workflow Function

6.9 Absolute $ Opportunity Analysis By Clinical Workflow Function , 2026-2030

Chapter 7. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – By Deployment Model

7.1 Introduction/Key Findings

7.2 Cloud-Based Ambient AI Platforms

7.3 On-Premise Clinical AI Systems

7.4 Hybrid Deployment Models

7.5 Edge AI & Device-Integrated Solutions

7.6 Others

7.7 Y-O-Y Growth trend Analysis By Deployment Model

7.8 Absolute $ Opportunity Analysis By Deployment Model , 2026-2030

Chapter 8. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – By Care Model

8.1 Introduction/Key Findings

8.2 Acute NHS Hospitals

8.3 General Practice & Primary Care Networks

8.4 Community Care & Integrated Care Systems

8.5 Mental Health Trusts

8.6 Ambulance & Emergency Care Services

8.7 Specialty Care Clinics

8.8 Others

8.9 Y-O-Y Growth trend Analysis Care Model

8.10 Absolute $ Opportunity Analysis Care Model , 2026-2030 Chapter 9. United Kingdom Virtual Wards and Hospital-at-Home Technology MARKET – By By Clinical Use Case

9.1 Introduction/Key Findings

9.2 Respiratory Conditions

9.3 Cardiovascular Conditions

9.4 Frailty & Elderly Care

9.5 Post-Surgical Recovery

9.6 Oncology Care

9.7 Infectious Diseases

9.8 Chronic Disease Management

9.9 Others

9.10 Y-O-Y Growth trend Analysis By Clinical Use Case

9.11 Absolute $ Opportunity Analysis, By Clinical Use Case 2026-2030

Chapter 10 United Kingdom Virtual Wards and Hospital-at-Home Technology Market – By Healthcare Provider Type

10.1 Introduction/Key Findings

10.2 NHS Acute Hospital Trusts

10.3 Community Healthcare Providers

10.4 Integrated Care Systems (ICSs)

10.5 Mental Health & Specialist Trusts

10.6 Independent Healthcare Providers

10.7 Others

10.8 Y-O-Y Growth trend Healthcare Provider Type

10.9 Absolute $ Opportunity Healthcare Provider Type , 2026-2030

Chapter 11 United Kingdom Virtual Wards and Hospital-at-Home Technology Market, By Geography – Market Size, Forecast, Trends & Insights

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.2. By By Clinical Use Case

11.2.3. By Healthcare Provider Type

11.2.4. By Clinical Workflow Function

11.2.5. Deployment Model

11.2.6. Care Model

11.2.7. Countries & Segments - Market Attractiveness Analysis

Chapter 12 United Kingdom Virtual Wards and Hospital-at-Home Technology Market – Company Profiles – (Overview, Deployment Model Portfolio, Financials, Strategies & Developments)

12.1 Doccla

12.2 Huma

12.3 Graphnet Health

12.4 Docobo Ltd

12.5 Inhealthcare

12.6 Feebris

12.7 Philips Healthcare

12.8 Masimo

12.9 Dignio

12.10 BT Group

Fill out the form below and our team will get back to you shortly

FAQ's

The United Kingdom Virtual Wards and Hospital-at-Home Technology Market was valued at approximately USD 412.6 Million. It is projected to grow at a CAGR of around 15.5% during the forecast period of 2026–2030, reaching an estimated USD 848.08 Million by 2030.

The major drivers of the United Kingdom Virtual Wards and Hospital-at-Home Technology Market include increasing healthcare capacity pressures, rising adoption of digitally enabled care pathways, and growing demand for remote patient management technologies. Healthcare providers are investing in virtual care infrastructure to optimize resource utilization, reduce unnecessary hospital admissions, improve patient monitoring, and enhance clinical efficiency. Additionally, increasing emphasis on interoperability, workflow automation, integrated care delivery, and healthcare modernization initiatives is accelerating market growth across NHS organizations and community healthcare settings.

England is the most dominant region in the United Kingdom Virtual Wards and Hospital-at-Home Technology Market, supported by extensive NHS virtual ward deployments, advanced digital healthcare infrastructure, strong investment in remote care technologies, and broad adoption across acute and community care settings. Scotland is expected to be the fastest-growing region during the forecast period of 2026–2030, driven by healthcare digitalization initiatives, expansion of Hospital-at-Home programs, and increasing investments in remote monitoring and integrated care delivery models. Wales and Northern Ireland continue to experience steady growth supported by ongoing healthcare modernization efforts and expanding virtual care capabilities.

The key players in the United Kingdom Virtual Wards and Hospital-at-Home Technology Market include Doccla, Huma, Graphnet Health, Docobo Ltd, Inhealthcare, Feebris, Philips Healthcare, Masimo, Dignio, BT Group, Current Health (Best Buy Health), Lenus Health, Cera Care, The Access Group, and Luscii (Omron Healthcare).

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19432 | Published Date: June 2026 | Format: Excel and PDF

In 2025, the Europe Digital Health Reimbursement Pathways Market was valued at approximately USD 5.40 Billion and is projected to reach around USD 8.50 Billion by 2030, expanding at a CAGR of about 9.50% during 2026–2030...

Report Code: VMR-19431 | Published Date: June 2026 | Format: Excel and PDF

The United States Digital Obesity Care and GLP-1 Support Market was valued at approximately USD 2185.4 million. It is projected to grow at a CAGR of around 22.1% during the forecast period of 2026–2030, reaching an estim...

Report Code: VMR-19429 | Published Date: June 2026 | Format: Excel and PDF

In 2025, the United States Ambient Clinical Documentation AI Market was valued at approximately USD 1.02 Billion and is projected to reach around USD 3.12 Billion by 2030, expanding at a CAGR of about 25.09% during 2026–...

Report Code: VMR-19427 | Published Date: June 2026 | Format: Excel and PDF

The United Kingdom NHS Ambient Scribing and Clinical Workflow AI Market was valued at approximately USD 186.4 million. It is projected to grow at a CAGR of around 22.4% during the forecast period of 2026–2030, reaching a...

Report Code: VMR-19426 | Published Date: June 2026 | Format: Excel and PDF

The United Kingdom AI Diagnostics and Community Diagnostic Centres Market was valued at approximately USD 318.7 Million. It is projected to grow at a CAGR of around 24.2% during the forecast period of 2026–2030, reaching...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”