Synthetic Compressor Oil Market Research Report – Segmentation by Type (Polyalphaolefin (PAO), Polyalkylene Glycol (PAG), Synthetic Esters, Silicone-based oils, Poly-internal olefins (PIO), Bio-based synthetic oils); By Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Retail, Specialty Stores, Original Equipment Manufacturers (OEMs), Aftermarket Suppliers);and Region - Size, Share, Growth Analysis | Forecast (2025– 2030)

Synthetic Compressor Oil Market Size (2025-2030)

The Synthetic Compressor Oil Market was valued at USD 8.61 Billion in 2024 and is projected to reach a market size of USD 11.61 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 4.36%.

The synthetic compressor oil market is a vital segment of the broader industrial lubricants industry, catering to a wide range of end-users across sectors such as manufacturing, automotive, oil & gas, food & beverage, and pharmaceuticals. The rising emphasis on energy efficiency, equipment longevity, and operational reliability has fueled the demand for synthetic compressor oils, which outperform conventional mineral-based lubricants in high-performance applications. These lubricants are engineered to withstand extreme temperatures, resist oxidation, and reduce wear and tear on mechanical components, ensuring the seamless operation of compressors in industrial settings.

Key Market Insights:

The global synthetic compressor oil market has demonstrated robust performance in 2024, reaching a valuation of $5.8 billion as industrial sectors continue to prioritize equipment efficiency and longevity. Polyalphaolefin (PAO) based formulations have secured dominance with 43% market share, valued for their exceptional thermal stability and extended drain intervals, while synthetic esters represent 27% of the market due to their superior biodegradability and performance in high-temperature applications. The average price point for premium synthetic compressor oils stabilized at $11.40 per liter, representing a 3.2% increase from 2023 figures despite raw material cost pressures. Maintenance cost reduction has emerged as the primary purchase driver, with industrial customers reporting an average 22% decrease in total compressor maintenance expenses when transitioning from mineral-based to synthetic lubricants.

Energy efficiency improvements have become increasingly quantifiable, with synthetic oils demonstrating an average 4.7% reduction in compressor energy consumption compared to conventional alternatives, translating to approximately $187 million in collective energy savings across industrial applications in 2024. Service interval extension represents another significant value proposition, with synthetic formulations enabling 8,500-hour average drain intervals compared to 2,000 hours for mineral oils, substantially reducing downtime and disposal costs. The food and beverage sector has emerged as a high-growth application area, consuming 840,000 metric tons of food-grade synthetic compressor oils in 2024, a 17% increase from the previous year as manufacturers prioritize risk reduction and regulatory compliance.

Synthetic Compressor Oil Market Drivers:

The relentless march of industrial automation has emerged as a powerful catalyst in the synthetic compressor oil market.

The compressor is a silent hero in the industrial world, and it is at the center of this revolution. Numerous processes depend on these devices since they are responsible for supplying compressed air or gas for different uses. These compressors are used more frequently as automation rises, which makes the lubricants that keep them operating properly even more crucial. The exceptional qualities of synthetic compressor oils put them in a prime position to satisfy the requirements of this new industrial paradigm. Synthetic formulations provide improved oxidation stability over typical mineral oils, enabling longer drain intervals. This attribute is in perfect harmony with the automation-driven goal of fewer maintenance cycles and downtime.

The global push for environmental sustainability has become a powerful force shaping industries across the board, and the synthetic compressor oil market is no exception.

The demand on industries to minimize their environmental effect and lower their carbon footprint is at the forefront of this transition. Conventional mineral-based compressor oils, which come from petroleum, have a history of posing environmental risks because of their propensity for pollution and non-biodegradable nature. Synthetic compressor oils, on the other hand, provide a greener substitute that is in line with the global sustainability goal. Biodegradability is a feature of many synthetic compressor oils, especially those made from ester-based formulations. This feature greatly lowers the environmental risk in the event of spills or leaks, which is important for businesses operating in delicate ecosystems or under tight environmental regulations. Manufacturers are prioritizing synthetic choices as a result of the ability to promote compressor systems employing "green" lubricants, which has become a major marketing factor.

Synthetic Compressor Oil MarketRestraints and Challenges:

The greater upfront cost of synthetic compressor oils in comparison to traditional mineral-based options is one of the biggest obstacles to their widespread use. This price premium, which is sometimes three to five times more than that of mineral oils, may put off budget-conscious companies, especially small and medium-sized ones. Even while longer drain intervals and increased efficiency provide long-term advantages, businesses with limited resources or those in fiercely competitive industries with narrow profit margins may find it difficult to justify the initial outlay. The complexity of transitioning from mineral to synthetic oils presents another challenge. Many existing compressor systems were designed with mineral oils in mind, and switching to synthetics isn't always a straightforward process. Issues such as seal compatibility, potential leakage due to the different flow characteristics of synthetics, and the need for thorough system cleaning before changeover can make the transition daunting. This complexity can lead to reluctance among end-users to make the switch, especially if their current systems are functioning adequately. Market fragmentation also poses a challenge. The synthetic compressor oil market is characterized by a wide array of products tailored for specific applications and industries. While this diversity caters to specialized needs, it can also lead to confusion among end-users and complicate inventory management for distributors. The lack of standardization across different manufacturers further compounds this issue, making it difficult for users to compare products directly or switch between brands easily.

Synthetic Compressor Oil MarketOpportunities:

One of the most promising avenues for expansion lies in the rapidly growing renewable energy sector. As wind and solar power installations proliferate worldwide, the demand for high-performance compressor oils in these applications is surging. Wind turbines, in particular, require lubricants that can withstand extreme conditions and provide long-lasting protection. Synthetic compressor oils, with their superior stability and performance characteristics, are ideally suited for these demanding environments. Manufacturers who can develop specialized formulations for renewable energy applications stand to capture a significant share of this burgeoning market. The ongoing digital transformation of industries presents another exciting opportunity. As Industrial Internet of Things (IIoT) technologies become more prevalent, there's growing potential for "smart" synthetic oils. These advanced lubricants could incorporate sensors or markers that allow for real-time monitoring of oil condition, viscosity, and contamination levels. By integrating with predictive maintenance systems, these smart oils could revolutionize compressor maintenance practices, offering unprecedented levels of efficiency and reliability. Companies that can successfully merge lubrication technology with digital capabilities will likely find themselves at the forefront of the industry.

SYNTHETIC COMPRESSOR OIL MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2024 - 2030

Base Year

2024

Forecast Period

2025 - 2030

CAGR

4.36%

Segments Covered

By Type, , Distribution Channel and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

Exxon Mobil, Royal Dutch Shell, BP, Chevron, Total Energies, FUCHS Petrolub SE, Idemitsu Kosan Co., Ltd., PetroChina Company Limited, Sinopec, Valvoline Inc., Lukoil, ENI S.p.A.l, Phillips 66, Petronas Lubricants International, Gulf Oil International.

Synthetic Compressor Oil MarketSegmentation:

Synthetic Compressor Oil Market Segmentation: By Types:

Polyalphaolefin (PAO)

Polyalkylene Glycol (PAG)

Synthetic Esters

Silicone-based oils

Poly-internal olefins (PIO)

Bio-based synthetic oils

Polyalphaolefin (PAO) based synthetic oils dominate the market. PAOs have established themselves as the go-to option for many industries due to their excellent overall performance characteristics. PAO-based synthetic oils have proven particularly popular in industries requiring high-performance lubricants, such as automotive, aerospace, and heavy manufacturing. Their ability to maintain effectiveness under extreme conditions and contribute to energy efficiency has cemented their position as the dominant type in the synthetic compressor oil market.

Bio-based synthetic oils are emerging as the fastest-growing segment. This rapid growth is driven by increasing environmental concerns and stringent regulations pushing industries towards more sustainable solutions. Bio-based synthetic oils, derived from renewable resources such as vegetable oils or synthetic esters, offer a compelling combination of high performance and reduced environmental impact. These oils are gaining traction across various industries, particularly in regions with strict environmental regulations. Their biodegradability and potential for carbon footprint reduction make them attractive to companies aiming to enhance their sustainability profiles.

Synthetic Compressor Oil Market Segmentation: By Distribution Channel:

Direct Sales

Distributors/Wholesalers

Online Retail

Specialty Stores

Original Equipment Manufacturers (OEMs)

Aftermarket Suppliers

Currently, the most common distribution route for synthetic compressor oils is distributors/wholesalers. In industries where technical know-how and product assistance are vital, distributors are critical in bridging the gap between producers and end-users. They frequently act as more than just a conduit for sales, offering insightful guidance on the choice, use, and upkeep of products. This channel's dominance is especially noticeable in sectors that need specialized lubricant handling and storage or have intricate supply networks.

The synthetic compressor oil distribution route that is expanding the quickest is online retail. Manufacturers and distributors may offer comprehensive product specifications, use directions, and even virtual consultation services through online platforms. Customers may make well-informed judgments with the aid of this abundance of information, which is especially crucial for specialty items like synthetic compressor oils. Furthermore, accessing new markets and consumers who might not have easy access to traditional distribution networks is something that the internet channel is proven to be very good at.

In the market for synthetic compressor oil, North America is a major participant. The region's strong industrial foundation and technical breakthroughs are what fuel its market share. North America had around 30% of the world market for synthetic compressor oil in 2023. The aerospace, automotive, and industrial industries all make significant contributions to the United States' crucial role as the region's largest economy. The need for synthetic compressor oils is mostly driven by the existence of several industrial sites and the automobile sector.

Asia-Pacific is the fastest-growing region in the synthetic compressor oil market, driven by rapid industrialization and economic growth. The rising economic power of Asia-Pacific countries contributes to the expansion of various industries, including manufacturing, automotive, and electronics. Massive investments in infrastructure projects across the region boost the demand for high-performance compressor oils. Countries like China and Japan are experiencing significant industrial growth, leading to increased demand for synthetic compressor oils.

COVID-19 Impact Analysis on the Synthetic Compressor Oil Market:

The market for synthetic compressor oil had a notable decline in the early phases of the epidemic. Numerous industries saw a steep fall in industrial activity as a result of widespread lockdowns and economic uncertainty. Major users of synthetic compressor oils, including the automobile, aerospace, and general manufacturing industries, had to temporarily halt or scale back operations. The market was rocked by this abrupt decline in demand, which resulted in stockpiling and pressure on prices. All industries did not see a consistently unfavourable impact, though. Sectors that were considered vital, such pharmaceuticals, food processing, and healthcare, experienced a rise in activity. The need for premium synthetic compressor oils in these vital applications was indirectly increased by the spike in demand for medical goods, especially oxygen concentrators and ventilators. As economies began to recover and adapt to the "new normal," the synthetic compressor oil market started to show signs of resilience. The pandemic accelerated the trend towards automation and digitalization across industries, indirectly benefiting the market. As companies sought to reduce human intervention in their operations, the reliance on automated systems and machinery increased, driving demand for high-performance lubricants like synthetic compressor oils. The crisis also heightened awareness of the importance of maintenance and equipment reliability. With many businesses operating under financial constraints, there was a growing emphasis on extending the lifespan of existing equipment. This shift in focus favoured synthetic compressor oils, known for their superior performance and ability to extend drain intervals, potentially lowering overall maintenance costs. The pandemic-induced push towards sustainability and environmental consciousness also played a role in shaping the market. As companies reassessed their operations in light of the crisis, many renewed their commitment to environmentally friendly practices.

Latest Trends/ Developments:

One of the most significant trends is the development of synthetic oils capable of withstanding increasingly extreme operating conditions. As industries push the boundaries of what's possible, compressors are being subjected to higher temperatures, pressures, and speeds. In response, oil manufacturers are creating advanced formulations that maintain stability and performance under these harsh conditions. For instance, new synthetic oils are being designed to operate effectively in ultra-high-temperature environments found in aerospace applications or deep-sea drilling operations. The incorporation of nanotechnology into synthetic compressor oils is an exciting development. Nano-additives are being used to enhance the lubricating properties of these oils, improving their ability to reduce friction and wear. These nano-enhanced oils can potentially extend equipment life and improve energy efficiency. Research is ongoing into the use of graphene and other nanomaterials to create lubricants with unprecedented performance characteristics.

Key Players:

ExxonMobil

Royal Dutch Shell

BP

Chevron

Total Energies

FUCHS Petrolub SE

Idemitsu Kosan Co., Ltd.

PetroChina Company Limited

Sinopec

Valvoline Inc.

To Learn more about this report,

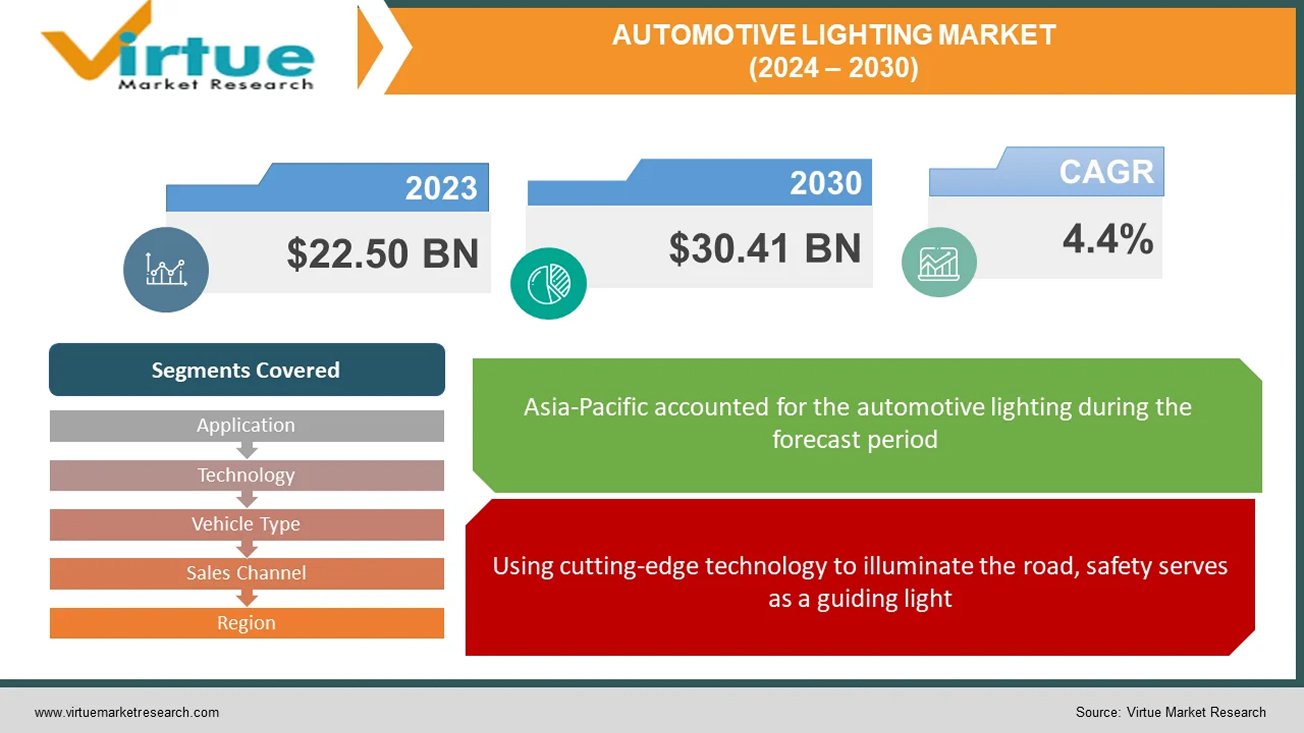

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

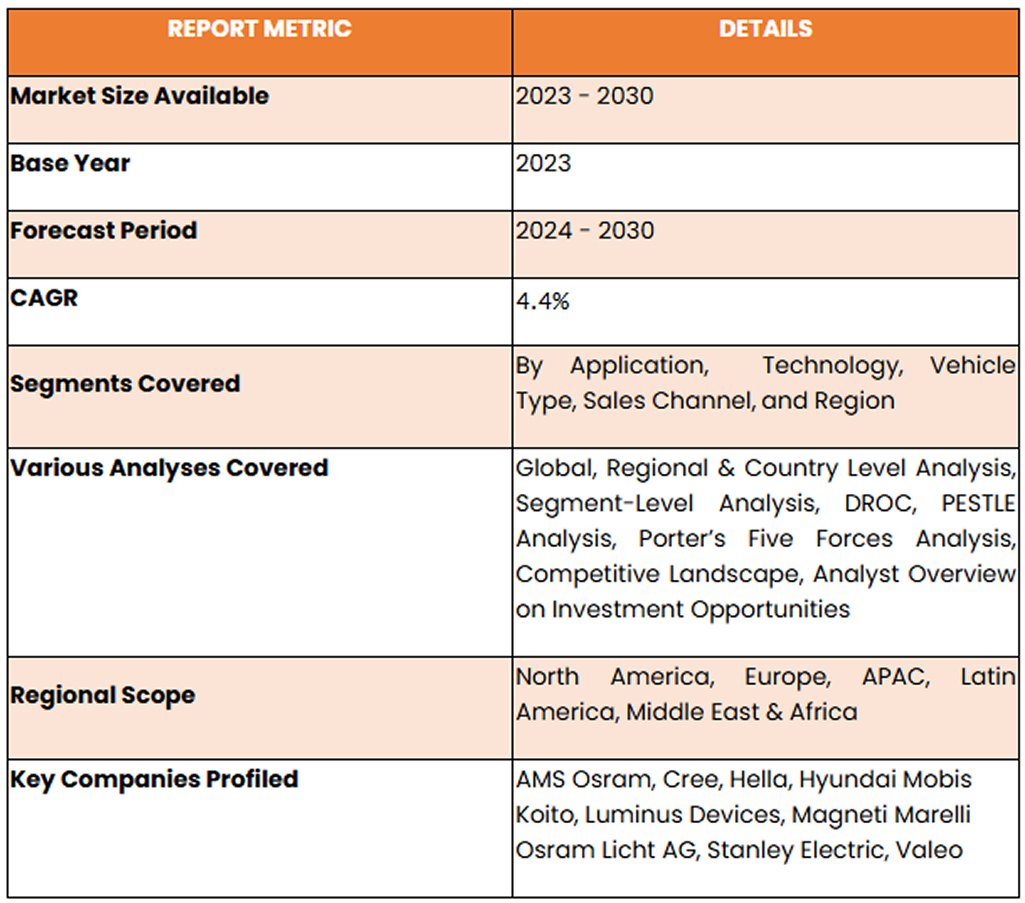

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

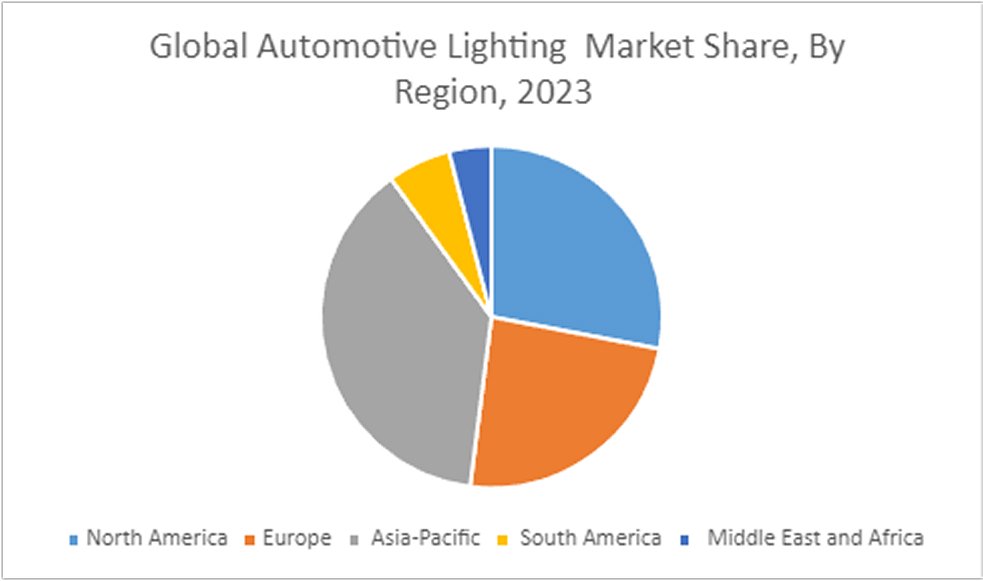

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Chapter 7. SYNTHETIC COMPRESSOR OIL MARKET – By Distribution Channel

7.1 Introduction/Key Findings

7.2 Direct Sales

7.3 Distributors/Wholesalers

7.4 Online Retail

7.5 Specialty Stores

7.6 Original Equipment Manufacturers (OEMs)

7.7 Aftermarket Suppliers

7.8 Y-O-Y Growth trend Analysis By Distribution Channel

7.9 Absolute $ Opportunity Analysis By Distribution Channel , 2025-2030

Chapter 8. SYNTHETIC COMPRESSOR OIL MARKET - By Geography – Market Size, Forecast, Trends & Insights

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Distribution Channel

8.1.3. By Types

8.1.4. Countries & Segments - Market Attractiveness Analysis

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Types

8.2.3. By Distribution Channel

8.2.4. Countries & Segments - Market Attractiveness Analysis

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia-Pacific

8.3.2. By Types

8.3.3. By Distribution Channel

8.3.4. Countries & Segments - Market Attractiveness Analysis

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Types

8.4.3. By Distribution Channel

8.4.4. Countries & Segments - Market Attractiveness Analysis

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. United Arab Emirates (UAE)

8.5.1.2. Saudi Arabia

8.5.1.3. Qatar

8.5.1.4. Israel

8.5.1.5. South Africa

8.5.1.6. Nigeria

8.5.1.7. Kenya

8.5.1.8. Egypt

8.5.1.8. Rest of MEA

8.5.2. By Types

8.5.3. By Distribution Channel

8.5.4. Countries & Segments - Market Attractiveness Analysis

Fill out the form below and our team will get back to you shortly

FAQ's

Synthetic compressor oils offer enhanced performance characteristics compared to mineral oils, including improved viscosity index, oxidation resistance, and thermal stability.

Synthetic compressor oils are generally more expensive than mineral oils, which can limit their adoption in cost-sensitive applications

Exxon Mobil, Royal Dutch Shell, BP, Chevron, Total Energies, FUCHS Petrolub SE, Idemitsu Kosan Co., Ltd., PetroChina Company Limited, Sinopec, Valvoline Inc., Lukoil, ENI S.p.A.l, Phillips 66, Petronas Lubricants International, Gulf Oil International.

North America is the most dominant region in the market, accounting for approximately 35% of the total market share.

Asia Pacific although currently holding a smaller market share of 25%, is the fastest-growing region in the market.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19305 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the AI Model Monitoring and Guardrails Market was valued at approximately USD 245.6 billion. It is projected to grow at a CAGR of around 10.9% during the forecast period of 2026–2030, reaching an estimated USD 4...

Report Code: VMR-19304 | Published Date: April 2026 | Format: Excel and PDF

The Critical Minerals & Rare Earth Elements Supply Market was valued at USD 362,000 Million in 2025 and is projected to reach a market size of USD 575,097.8 Million by the end of 2030. Over the forecast period of 2026–20...

Report Code: VMR-19276 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the global CBAM Compliance Solutions for Export-Oriented Value Chains Market was valued at approximately USD 1.20 billion. It is projected to grow at a CAGR of around 32.93% during the forecast period of 2026–20...

Report Code: VMR-19256 | Published Date: April 2026 | Format: Excel and PDF

The Global Fertilizer and Ammonia Supply Chain Resilience Market was valued at USD 9.14 billion in 2025 and is projected to reach a market size of USD 21.87 billion by the end of 2030. Over the forecast period of 2026–20...

Report Code: VMR-19077 | Published Date: February 2026 | Format: Excel and PDF

The Ferroconcrete Market was valued at USD 45.50 billion in 2025 and is projected to reach a market size of USD 70.20 billion by the end of 2030. Over the forecast period of 2026-2030, the market is projected to grow at...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”