PFAS Water Treatment Market Research Report – Segmentation By technology (Granular activated carbon, Ion-exchange resins, Membrane filtration, Advanced oxidation and electrochemical systems, Other adsorption and thermal treatment methods), By media type (Carbon-based media, Resin-based media, Membrane media, Hybrid engineered sorbents, Other specialized treatment media), By application (Drinking water treatment, Industrial wastewater management, Groundwater and site remediation, Firefighting foam runoff treatment, Other related water purification applications); and Region - Size, Share, Growth Analysis | Forecast (2026– 2030)

PFAS Water Treatment Market Size (2026-2030)

The Global PFAS Water Treatment Market was valued at USD 2.13 Billion in 2025 and is projected to reach a market size of USD 2.98 Billion by the end of 2030. Over the forecast period of 2026-2030, the market is projected to grow at a CAGR of 7%.

The Global PFAS Water Treatment Market can be described as a fast-developing ecosystem of technologies, media solutions, and application-specific ways of treatment aimed at removing, reducing, or containing per- and polyfluoroalkyl substances in various streams of water, and it has become one of the most strategically specific segments in the overall environmental remediation environment. With the increasing regulatory pressure on the planetary level and the scientific evidence still indicating that exposure to PFAS is linked to long-term risks in health and ecology, the market is experiencing an acute acceleration in innovation, scale, and cross-sector adoption. The technology vendors are gradually evolving the older treatment models with high-performance sorbents, milled-to-fit resins, novel membrane structures, and state-of-the-art electrochemical and oxidation routes that can treat not only old contaminants but also the more complicated PFAS chemistries.

PFAS-treatment rollouts and utility acquisitions have more financing capacity with a rising activity of at least 26%. Annually, by private-equity and infrastructure funds that are entering the water sector.

Remediation demand is being transformed by the increasing legal obligations. Insurers disclose 1,129 billion of global non-life run-off reserves, of which approximately 55% are changing deal structures because of PFAS exposure-forcing the stakeholders on remediation-funded avenues.

Market Drivers:

Stiffening regulatory pressure and increasing safety standards drive the market.

Governments and regulators worldwide have increased the limits and monitoring demands since the emergence of per- and polyfluoroalkyl compound (PFAS) health hazards awareness has intensified. The industry reacts: local governments, industries, and individual water managers are now subject to evident legal and financial repercussions or fault due to the inability to achieve new thresholds. Compliance has ceased to be a choice; it has become a business necessity. This host of new regulations jumpstarts the demand for aggressive removals, point-of-use polishing to large-scale treatment trains. There are two impacts of regulatory action. First, it compels existing facilities to upgrade or overhaul outdated infrastructure--establishing short-term retrofit projects and a constant stream of capital projects. Second, it increases the minimum level of water quality standards in entire regions, which generates investment in research and pilots of future generations of removal techniques. The former companies that hadn't considered PFAS as a niche liability are now considering it as a strategic priority, which has led to budget allocation on assessment, monitoring and permanent treatment systems. The corporate compliance teams and utility boards focus on solutions that minimise liability in the long run. The net effect is an expansion of the overall market since almost all applications, such as the drinking water utilities to the industrial wastewater and the remediation of legacy sites, will have to be updated to meet these high standards. In simple terms, regulation opens markets, finances projects and transforms awareness into long-lasting buying behaviour.

Expanded application requirements and intersector adoption are driving the market.

The contamination of PFAS is not limited to a single industry or environment. It has reached drinking water systems, industrial effluents, groundwater plumes from past locations, and stormwater with remains of firefighting foams. Such a geographic and functional extent increases demand. The contractor who is required to remove an old manufacturing site will require a different approach compared to the utilities that are chasing the purity of their potable water, but they all require a reliable reduction of PFAS. Such versatility of uses increases the market depth and breadth. The end users also require highly flexible systems that will be able to respond to mixed contaminated streams without the need to redesign the system regularly. That need promotes adaptive media, hybrid sorbents and scaled process units-designs that can be optimised to suit different influent chemical, flow rates and concentrations. With resilience and future-proofing becoming key considerations of end users, suppliers with configurable and multi-application platforms receive more opportunities. The outcome is a market that is expanding, not only due to the increased stakeholder need for PFAS control, but also due to an increase in the capabilities of the stakeholders themselves, and the establishment of long-term demand in a variety of applications.

Market Restraints and Challenges:

Complexity in regulations and imbalanced standards.

The key barrier to the global PFAS water treatment market is regulatory complexity and a lack of standards. Policy environment is also fragmented: various jurisdictions have varied limits, testing procedures and schedules, which compel the vendors and the water companies to follow multiple compliance paths simultaneously. This division swells up expenses and delays implementation. Smaller communities and industries are being hit the hardest: they have to scrimp on specialized monitoring, retrofitting of treatment, and consultancy charges instead of investing in scalable and standardized solutions. The risk is also escalated with the uncertainty of the future rules that will cause the long-run capital not to flow into pilot projects and rollouts of new technologies. Manufacturers would be reluctant to mass-produce when the specifications of products and technologies allowed can change under new regulations. Simultaneously, the litigation and liability risks associated with the legacy contamination introduce legal overhead and lead to the diversion of funds not towards active upgrades. Collectively, these forces squeeze margins and stretch sales cycles of the suppliers, as well as making procurement decisions by end users complex. The market will not be able to effectively convert technical innovation rapidly into popular, affordable treatment capacity so long as regulators do not come to harmonized thresholds and practical guidance. A sense of coordination and clarity is still necessary.

Market Opportunities:

Technological innovation and modular solutions.

The technological innovation promises a promising future through which the market of PFAS water treatment can be redefined, and more people can have the opportunity to implement effective water treatment. Current developments in hybrid sorbents, selective ion-exchange chemistries, and next-generation membranes have enhanced the removal efficiencies and reduced the energy and material footprints. Skid-mounted (modular), decentralized designs allow smaller utilities and industrial locations to implement designs based on local requirements, without giant civil works. Adsorbent-based pilot experiments that include adsorbents with non-selective oxidation or thermal elimination can be promising in treating more challenging mixtures of PFAS. The potential solution of commercialization of regenerable low-cost media that is regenerable could change the approach in operating models by saving on the recurrent replacement costs and also allow the recycling or recovery of media. The technology has been proven through private-public cooperation: demonstration grants, research consortia and co-funded field trials make adoption less risky to manufacturers and end users. In cases where organisations synchronise product roadmaps with effective monitoring procedures and disposal channels, customers become confident, and the procurement process becomes quick. In the long run, these innovations have the potential of reducing entry barriers, generating new service revenues, and providing competitive differentiation to firms that bind performance and transparent lifecycle management. Durable, cost-effective solutions will be achieved by the market leaders and will attract large contracts and grow fast.

PFAS WATER TREATMENT MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2025 - 2030

Base Year

2025

Forecast Period

2026 - 2030

CAGR

7%

Segments Covered

By technology , application, media type, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

Veolia, SUEZ, Evoqua Water Technologies, Xylem, Jacobs Engineering, AECOM, Arcadis, Tetra Tech, Wood PLC, Battelle Memorial Institute, Gradiant, Puraffinity, CycloPure, Purolite, and Newterra.

PFAS Water Treatment Market Segmentation:

PFAS Water Treatment Market Segmentation by Technology

Granular activated carbon

Ion-exchange resins

Membrane filtration

Advanced oxidation and electrochemical systems

Other adsorption and thermal treatment methods

The current technology is granular activated carbon that has dominated with the majority share based on the proven performance, wide use by the municipalities, and because of its familiarity among its users. Under third-person narration, the market recognises the reassuring history, under GAC, to eliminate the legacy PFAS compounds when engineering teams have to deal with the latest short-chain chemistries that require new strategies. Membrane filtration and engineered resins are the leading technologies with the most rapid development caused by regulatory restrictions and the necessity to capture molecules that are missed by the traditional adsorbents. The balance between established methods of carbon-based systems and pilot membranes and resin beds is being made by manufacturers and utilities, who frequently implement hybrid trains in which adsorption coexists with nano-filtration or reverse osmosis. This technology ballet dances vendor differentiation: others make scalable GAC retrofit sales, others develop proprietary resin formulations, and a fresh group is developing destruction-ready providers of electrochemical and advanced oxidation. The investors and procurement officers both experience stability and disruption; GAC capex and consumables remain the favourite in the budget, whilst R&D and pilot capital seek membranes and resins that offer lower lifecycle costs and stricter effluent requirements, and community health outcomes are enhanced.

PFAS Water Treatment Market Segmentation by Media Type

Carbon-based media

Resin-based media

Membrane media

Hybrid engineered sorbents

Other specialised treatment media

The carbon-based media, with granular and powdered activated carbons taking the lead, have the largest section of the treatment media sales as they have broad availability, ease of operation, and their removal effectiveness with many traditional PFAS has been documented. Under third-person narration, according to the industry observers, buyers are drawn to carbon since it is easy to incorporate into the existing filters, and they are aware of the regeneration or replacement cycles. However resin resin-based media has become the fastest expanding type, driven by both designed chemistries specific to short-chain PFAS and advertising that focuses on selectivity, capacity and faster sorption kinetics of difficult influents. Suppliers place resins as either a complement or a substitute for carbon, based on site chemistry, capital restriction and waste management. Hybrid sorbents and membrane media have a niche role to play when they are required by footprint, lifecycle disposal or demanding effluent requirements. Procurement groups have that way gone to a portfolio mentality, carbon to support broad utility retrofits, resin to favour specific removals, membrane to support high purity or industrial reuse, and hybrid in situations where complexity warrants custom engineering responses, and restrictions increase.

PFAS Water Treatment MarketSegmentation by Application

Drinking water treatment

Industrial wastewater management

Groundwater and site remediation

Firefighting foam runoff treatment

Other related water purification applications

The biggest usage is drinking water treatment, which is driven by compliance programs at the municipal level, concerns of people and high urgency to reach by the stricter health advisory limit. Ultimately, in third-person prose, utilities and consultants focus on point-of-entry and treatment-plant upgrades that reduce the exposure of the community, as well as provide quantifiable decreases in PFAS levels. In the meantime, water purification of groundwater and treatment of industrial waste products are the most rapidly expanding application segments where old contamination sites and industrial dischargers are faced with remediation responsibilities and regulatory obligations. The projects of site remediation require sophisticated treatment trains, which are an integration of extraction, adsorption, and destruction pathways, and industrial players invest in the pre-treatment to defend downstream municipal systems. The real-world interaction of drinking water programs and clean-up efforts results in cross-sector learning: contaminated site pilots educate municipal retrofits and vice versa. Consultancies exploit this by packaging these services together: monitoring, permitting and end-of-life disposal, and technology vendors, in turn, develop modular solutions that can be adjusted depending on the variable influent chemistry in the settings. The outcome is a growing market whereby the urgency to comply and technical innovations meet to mitigate exposures and rehabilitate the affected waters in the long term in a responsible manner.

PFAS Water Treatment Market Segmentation: Regional Analysis:

North America

Europe

Asia-Pacific

South America

Middle East & Africa

North America enjoys the greatest regional percentage due to the assertive regulation, historical contamination places and a high level of municipal and federal funding, all of which create demand in PFAS treatment technologies. In the third-person narration, the U.S. and Canadian programs that hasten the implementation of granular activated carbon, pilot resin systems, and built-in monitoring networks are mentioned by the audience. Europe is still relevant, having EU strict directives and country programs that maintain procurement and service markets. Asia Pacific is the leader in terms of growth as urbanisation, industrial growth and increased environmental consciousness are driving municipal improvement and industrial pretreatment investment. South America and the Middle East & Africa are smaller, emerging markets in which demand tends to focus on specific industrial or military locations, and not on the general programs of the municipality. The geographic combination thus compels sellers to balance between mature and huge contracts with agile entry strategies to high growth markets, align product roadmaps, service offerings and local relationships with diverse regulatory and commercial dynamics. These regional trends are followed with keen interest by investors and policymakers with high emphasis on scalability, capacity building locally and sustainable waste-management opportunities to achieve the long-term objectives of efficacy and resilience community.

COVID-19 Impact Analysis:

The COVID-19 crisis has affected the Global PFAS Water Treatment market in a complex and permanent manner that has triggered an urgent re-setting of priorities among the public utilities, industrial operators, and remediation specialists. Municipal revenues reduced, factories halted production, and budgets were tightened, so those projects that appeared not to be urgent, such as long-term groundwater cleanup or renovations aimed at dealing with per- and polyfluoroalkyl substances, were frequently postponed or reduced. Simultaneously, the pandemic was triggering some strategic changes that indirectly served the benefit of the PFAS market. The COVID-19-driven restructuring of the PFAS market is not a smaller, slower version of the earlier one, but a reformulated one, with a different emphasis on digital capabilities and more risk-averse capital planning and integrated, adaptive treatment strategies that enforce more urgent social health needs in a limited environmental setting and that respond to those needs.

Latest Trends and Developments:

The worldwide PFAS water-treatment industry is going through a swift, practical transformation: regulatory intensity and place-in-the-media policymaking are pushing the industry out of the niche remediation work and into the mass utility planning, and it is creating a ripple that is simultaneously driving what is being purchased and what is being developed by technologists. Regulators and governments have shifted to binding measures as opposed to conditional advice, pushing utilities and industrial operators to focus on established tactical removals as they seek more sophisticated destruction methods. Meanwhile, market analysts are still registering high multi-year growth with the municipalities and industries strenuous to comply with new standards and reporting demands. In practice, the market exhibits a stratified technology structure-granular activated carbon continues to be actively used near-terminally because of familiarity with operations and moderate cost; ion-exchange resins and engineered sorbents are becoming increasingly common because of either short-chain PFAS or space constraints; and membrane-based technology or hybrid engineered treatments are becoming widespread with complex, high-strength influents. In addition to separation, there is a significant trend towards destruction and circularity in that pilot-scale electrochemical, advanced oxidation, and other emerging technologies are no longer just in the laboratory and are being rolled out in the real world because of the increasing number of technologies that destroy rather than concentrate PFAS molecules.

Key Players in the Market:

Veolia

SUEZ

Evoqua Water Technologies

Xylem

Jacobs Engineering

AECOM

Arcadis

Tetra Tech

Wood PLC

Battelle Memorial Institute

Market News:

Jan 23, 2023 Xylem acquired Evoqua, the supplier of PFAS treatment, at 7.5 billion, reorganising the supply chains involved in the treatment and, within two years, placing in-service over 80 PFAS treatment projects in the United States. The merger increased commercialization of carbon, resin, and hybrid media systems and concentrated the competition among the vendors. Operators reacted to this by adjusting the procurement strategies to be in line with the expanded capabilities of the combined firm.

To Learn more about this report,

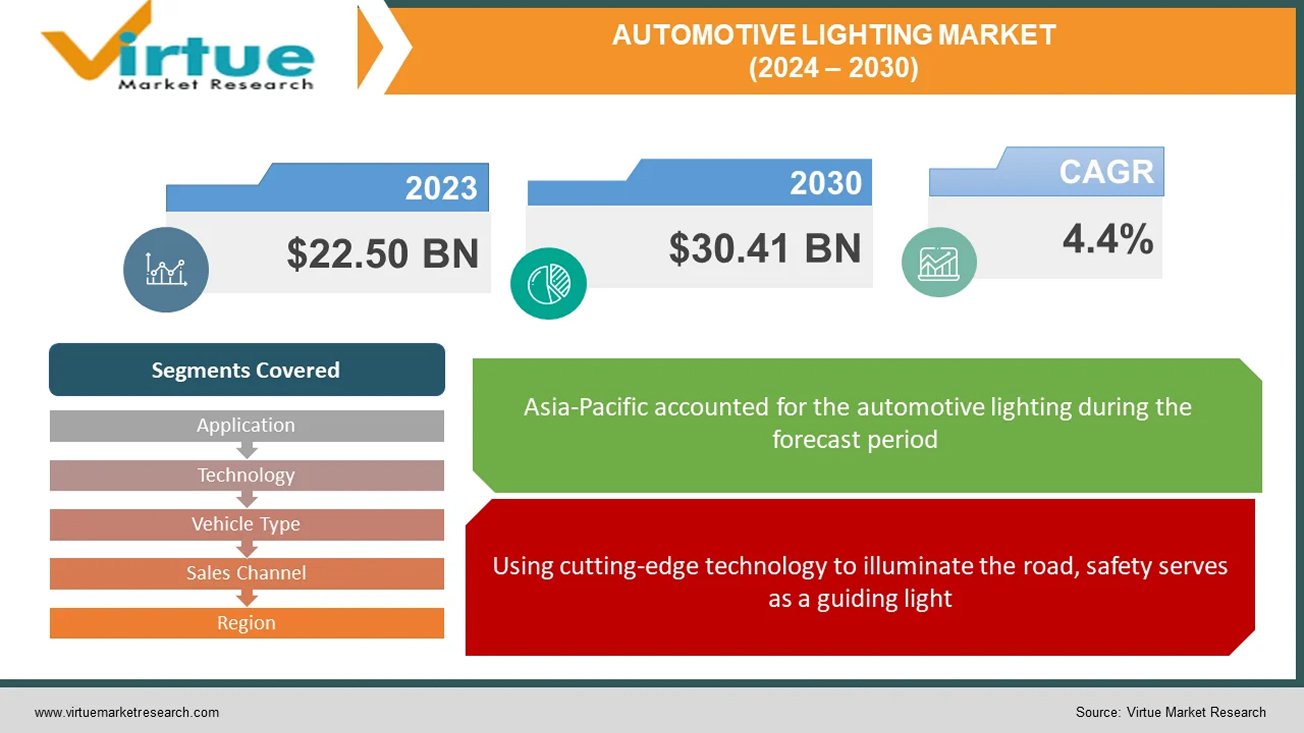

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

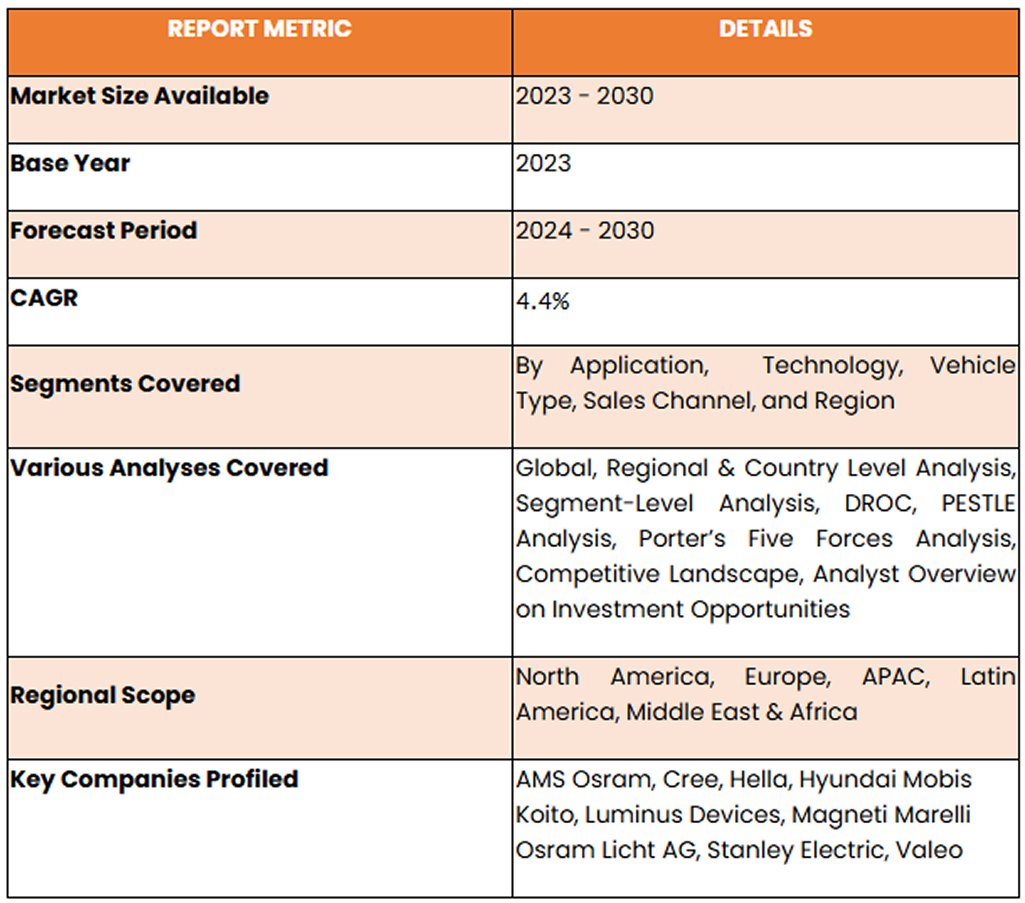

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

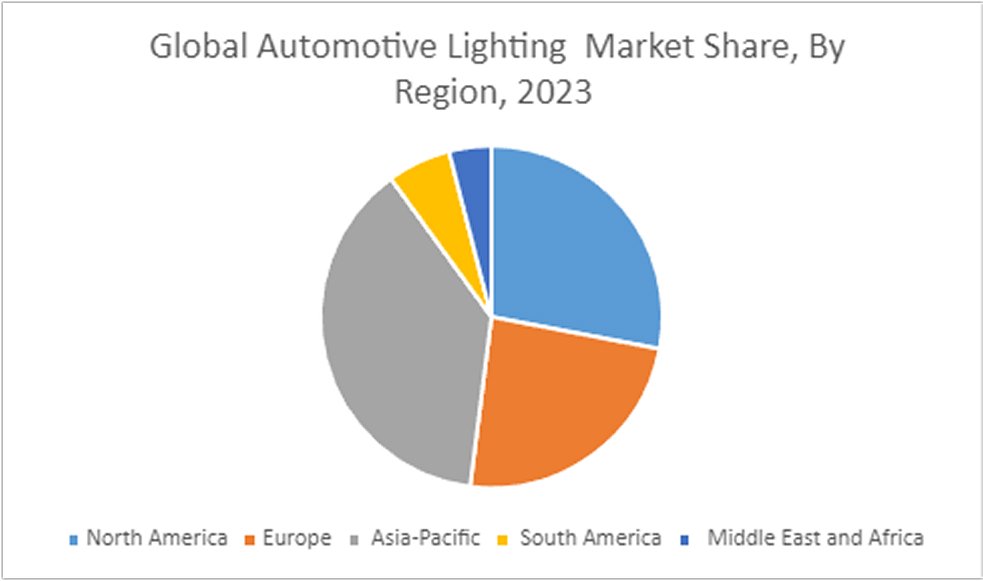

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. PFAS Water Treatment MARKET – SCOPE & METHODOLOGY

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Source

1.5. Secondary Source

Chapter 2. PFAS Water Treatment MARKET – EXECUTIVE SUMMARY

2.1. Market Size & Forecast – (2026 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. PFAS Water Treatment MARKET – COMPETITION SCENARIO

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Packaging TECHNOLOGY Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. PFAS Water Treatment MARKET - ENTRY SCENARIO

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Players

4.5.6. Threat of Substitutes

Chapter 5. PFAS Water Treatment MARKET - LANDSCAPE

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. PFAS Water Treatment MARKET – By Technology

6.1 Introduction/Key Findings

6.2 Granular activated carbon

6.3 Ion-exchange resins

6.4 Membrane filtration

6.5 Advanced oxidation and electrochemical systems

6.6 Other adsorption and thermal treatment methods

6.7 Y-O-Y Growth trend Analysis By Technology

6.8 Absolute $ Opportunity Analysis By Technology , 2026-2030

Chapter 7. PFAS Water Treatment MARKET – By Media Type

7.1 Introduction/Key Findings

7.2 Carbon-based media

7.3 Resin-based media

7.4 Membrane media

7.5 Hybrid engineered sorbents

7.6 Other specialised treatment media

7.7 Y-O-Y Growth trend Analysis By Media Type

7.8 Absolute $ Opportunity Analysis By Media Type , 2026-2030

Chapter 8. PFAS Water Treatment MARKET – By Application

8.1 Introduction/Key Findings

8.2 Drinking water treatment

8.3 Industrial wastewater management

8.4 Groundwater and site remediation

8.5 Firefighting foam runoff treatment

8.6 Other related water purification applications

8.7 Y-O-Y Growth trend Analysis Application

8.8 Absolute $ Opportunity Analysis Application , 2026-2030

Chapter 9. PFAS Water Treatment MARKET, BY GEOGRAPHY – MARKET SIZE, FORECAST, TRENDS & INSIGHTS

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Technology

9.1.3. By Application

9.1.4. By Media Type

9.1.5. Countries & Segments - Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Technology

9.2.3. By Application

9.2.4. By Media Type

9.2.5. Countries & Segments - Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Technology

9.3.3. By Application

9.3.4. By Media Type

9.3.5. Countries & Segments - Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Application

9.4.3. By Media Type

9.4.4. By Technology

9.4.5. Countries & Segments - Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Application

9.5.3. By Technology

9.5.4. By Media Type

9.5.5. Countries & Segments - Market Attractiveness Analysis

Chapter 10. PFAS Water Treatment MARKET – Company Profiles – (Overview, Technology Portfolio, Financials, Strategies & Developments)

10.1 Veolia

10.2 SUEZ

10.3 Evoqua Water Technologies

10.4 Xylem

10.5 Jacobs Engineering

10.6 AECOM

10.7 Arcadis

10.8 Tetra Tech

10.9 Wood PLC

10.10 Battelle Memorial Institute

Fill out the form below and our team will get back to you shortly

FAQ's

The growth of the Global PFAS Water Treatment Market is driven by intensifying regulatory pressure worldwide, rising enforcement of strict PFOS and PFOA limits, and expanding demand across drinking water utilities, industrial wastewater systems, and site remediation projects. Rapid innovation in granular activated carbon, selective ion-exchange resins, next-generation membranes, and hybrid sorbent technologies is accelerating adoption.

The Global PFAS Water Treatment Market faces key challenges such as regulatory complexity, fragmented regional standards, high capital and operating costs of advanced treatment technologies, and the difficulty of treating mixed long-chain and short-chain PFAS compositions.

Veolia, SUEZ, Evoqua Water Technologies, Xylem, Jacobs Engineering, AECOM, Arcadis, Tetra Tech, Wood PLC, Battelle Memorial Institute, Gradiant, Puraffinity, CycloPure, Purolite, and Newterra

North America holds the largest share of the Global PFAS Water Treatment Market, driven by aggressive regulations, major federal funding programs, extensive historical contamination sites, and accelerated adoption of carbon, resin, and membrane-based treatment systems.

Asia-Pacific is the fastest-growing region in the Global PFAS Water Treatment Market due to rapid industrial expansion, increasing urbanisation, rising environmental awareness, and major investments in municipal water treatment and industrial pretreatment infrastructure.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19305 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the AI Model Monitoring and Guardrails Market was valued at approximately USD 245.6 billion. It is projected to grow at a CAGR of around 10.9% during the forecast period of 2026–2030, reaching an estimated USD 4...

Report Code: VMR-19304 | Published Date: April 2026 | Format: Excel and PDF

The Critical Minerals & Rare Earth Elements Supply Market was valued at USD 362,000 Million in 2025 and is projected to reach a market size of USD 575,097.8 Million by the end of 2030. Over the forecast period of 2026–20...

Report Code: VMR-19276 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the global CBAM Compliance Solutions for Export-Oriented Value Chains Market was valued at approximately USD 1.20 billion. It is projected to grow at a CAGR of around 32.93% during the forecast period of 2026–20...

Report Code: VMR-19256 | Published Date: April 2026 | Format: Excel and PDF

The Global Fertilizer and Ammonia Supply Chain Resilience Market was valued at USD 9.14 billion in 2025 and is projected to reach a market size of USD 21.87 billion by the end of 2030. Over the forecast period of 2026–20...

Report Code: VMR-19077 | Published Date: February 2026 | Format: Excel and PDF

The Ferroconcrete Market was valued at USD 45.50 billion in 2025 and is projected to reach a market size of USD 70.20 billion by the end of 2030. Over the forecast period of 2026-2030, the market is projected to grow at...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”