In 2025, the LiDAR Receiver & Photodetector Components Market was valued at approximately USD 1.18 billion. It is projected to grow at a CAGR of around 14.3% during the forecast period of 2026–2030, reaching an estimated USD 2.30 billion by 2030.

The Global LiDAR Receiver and Photodetector Components Market is the ecosystem of sensing components that transform reflected laser light into electrical signals and provide LiDAR systems with the ability to provide precise ranging measurements of distance, depth, and spatial geometry. These elements are at the core of current three-dimensional sensing systems in mobility, industrial automation, mapping, and enhanced perception systems. The market is generally composed of semiconductor photodetectors and integrated optical receiver circuits, as well as specialized sensing modules that are intended to capture high-speed signals and reduce noise. It specifically deals with the elements that allow optical signal capture in LiDAR hardware and not the entire sensing system.

The market it focuses on includes detector chips, optical front-end electronics, and hybrid receiver assemblies optimized across wavelength bands and semiconductor material platforms. Nevertheless, it does not generally include upstream laser transmitters, mechanical scanning assemblies, or downstream LiDAR software or analytics platforms. The focus is still on the delicate electronic interfaces, which convert photons to useful data signals. These constituents require an extremely high level of sensitivity, time, and reliability in order to work in a sophisticated sensing environment.

In recent years, the situation has changed rapidly, with LiDAR being used not only in experimental settings but also in commercial and industrial uses. Advances in semiconductor manufacturing, increased levels of integration, and new material platforms have limited size, power, and cost whilst extending performance limits. Simultaneously, system designers are becoming more focused on smaller receiver designs that can achieve higher scan rates and extended ranges.

Key Market Insights

The developers of autonomous vehicles have made over one hundred and sixty-four billion dollars, which has enhanced the innovation of LiDAR sensing and photodetectors.

Car models with LiDAR-based Level-2+ autonomy have an approximate cost of sensor devices of about 1500-2000 dollars.

The market size of LiDAR sensors is expected to increase to approximately 2 billion dollars in the year 2025 and up to 7 billion dollars in the year 2035.

ADAS and autonomy sensors in a car are expected to grow by approximately 8 percent every year across the globe.

The market for automotive sensors as a whole will grow to almost twice the 23 billion level of 2019.

The driverless technologies have the potential to create $300-400 billion in passenger-vehicle revenues worldwide every year by 2035.

In some urban settings, the operating costs of robot taxis can be 40-50 percent lower than those of a traditional ride-hailing company.

By 2040, autonomous vehicles have the potential to make up more than 40 percent of the number of new cars sold.

By 2040, China would be able to contribute 66 percent to passenger-kilometers covered by autonomous vehicles.

The market size of semiconductors used autonomously in driving can grow to a level of 29 billion dollars annually by the year 2030 worldwide.

Autonomous sensor ecosystems are estimated to be more than 40 billion dollars in the automotive market in 2035.

Mobility-as-a-service has the potential to grow by capturing 25-30 percent of the industry profit pools through autonomous mobility services.

Research Methodology

Scope & Definitions

Market covers commercial sales of LiDAR receiver and photodetector components, including APD, SPAD, PIN photodiodes, SiPM, and integrated receiver modules.

Excludes LiDAR transmitters, full LiDAR systems, software analytics, and aftermarket services.

Geography: global coverage across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa.

Timeframe: historical analysis, current baseline year, and forward forecast period defined in-report.

Segmentation follows component type, material platform, wavelength compatibility, integration level, and end-use industry.

A standardized data dictionary ensures consistent definitions and prevents double counting across segments.

Evidence Collection (Primary + Secondary)

Primary interviews with executives, product managers, photonics engineers, distributors, and system integrators across the LiDAR and semiconductor value chain.

Coverage includes component manufacturers, module suppliers, LiDAR system developers, and downstream OEMs.

Secondary research uses verifiable sources including company annual reports, investor presentations, technical papers, patents, and trade publications.

Regulatory, standards, and industry inputs sourced from organizations such as IEEE, Optica, and relevant regulators/standards bodies/industry associations specific to LiDAR Receiver & Photodetector Components Market (named in-report).

Triangulation & Validation

Market size estimated using bottom-up supplier revenue aggregation and top-down demand modeling from LiDAR system shipments.

Results reconciled with company financial disclosures and product-level revenue where available.

Conflicting data resolved through multi-source comparison, expert interviews, and statistical normalization.

All major estimates undergo internal analyst peer review.

Presentation & Auditability

Key findings supported by source-linked evidence and verifiable datasets referenced throughout the report.

Transparent assumptions, calculation steps, and segmentation rules documented in-report.

Tables, charts, and forecasts maintain traceable inputs for enterprise decision-making.

Methodology ensures reproducibility and audit-ready transparency for stakeholders.

The high rate of development of autonomous and advanced driver assistance systems.

The Global LiDAR Receiver & Photodetector Components Market is driven by numerous forces that are most likely to impact the market and are highlighted by increasing rates of autonomous mobility and advanced driver-assistance technologies. Within the world of the automotive industry, auto manufacturers and technology vendors are putting a lot of money into sensing systems that can help cars view the world around them in an even more accurate way. The LiDAR technology will have a central role in this change since it provides high-resolution three-dimensional environmental mapping, which is paramount in safe automated navigation.

Raising the use of LiDAR in industry automation and smart infrastructure.

The contemporary industrial plants are greatly dependent on automated machines and robotic platforms, and autonomous material-handling systems. These systems should move around the warehouses, manufacturing facilities, and logistic centers safely and without colliding with the obstacles and, at the same time, keep the specific positioning. The LiDAR sensors are enhanced by sophisticated photodetector receivers to allow the robots and automated guided vehicles to create real-time 3-dimensional maps of the surrounding environment. This would greatly increase the safety of operation as well as boost the productivity of industrial activities.

Increasing the Demand for High-Resolution Mapping, Geospatial Analytics, and Environmental Monitoring.

The scanning systems based on LiDAR have been adopted by the geospatial professionals to record accurate elevation and structural data over wide areas. This information can be used in topography mapping, urban planning, land development, and transportation infrastructure design. The core of these systems is the photodetector receivers, which perceive reflected laser signals and transform them into precise measurements of distance.

The Global LiDAR Receiver and Photodetector Components. The market has a number of technical and commercial limitations that retard its broader adoption. Increased production costs are still being caused by complex manufacturing and precision semiconductor manufacturing. Simultaneously, there is an ongoing engineering dilemma of preserving high sensitivity and minimizing noise and power. The supply chain dependencies of specific materials and high-tech packaging technologies are also handled by industry participants. Moreover, the burden on development schedules and market scalability is further increased by system integration issues and high reliability demands, especially in safety-critical systems.

The growing autonomy and smart infrastructure initiatives are providing great prospects to the suppliers of the LiDAR receiver and photodetector components. Observers in the industry point out that demand is increasing because automotive sensing, robotics navigation, and other high-end mapping solutions are demanding quicker, more precise optical detection. Meanwhile, the modernization of defense and the implementation of smart city surveillance programs are stimulating investments in high-precision sensor technologies. The broader application in augmented reality devices and smaller and highly integrated consumer electronics further increases the scope of opportunities, compelling manufacturers to develop smaller, more energy-efficient, and more integrated photodetection platforms.

How this market works end-to-end

The LiDAR receiver and photodetector ecosystem sits inside a broader LiDAR system workflow. Understanding how these components fit into the sensing pipeline helps clarify why the market exists as a separate component layer.

System architecture planning

Engineers define system range, resolution, and safety requirements before choosing detection technology.

Wavelength selection

LiDAR systems typically operate in wavelength bands such as 850–905 nm, 940–1064 nm, 1310 nm, or 1550 nm. Receiver materials must match these wavelengths.

Detector technology choice

System designers choose between technologies such as avalanche photodiodes, SPAD devices, PIN photodiodes, or silicon photomultipliers.

Material platform decision

Photodetectors may use silicon, indium gallium arsenide, germanium, gallium arsenide, or hybrid semiconductor structures depending on sensitivity and wavelength requirements.

Integration strategy

Some systems use discrete detectors. Others integrate photodetector arrays or monolithic receiver chips with signal processing electronics.

Receiver module assembly

Manufacturers integrate detectors into optical front-end modules that include amplification and noise control circuits.

System-level integration

Receiver modules are combined with laser transmitters and scanning optics inside a LiDAR system.

End-use deployment

Systems are deployed in automotive autonomy, robotics, mapping, aerospace, smart infrastructure, and consumer devices.

What matters most when evaluating claims in this market

Claim type

What good proof looks like

What often goes wrong

Detection sensitivity

Measured device performance under controlled test conditions

Marketing values without test context

Long-range capability

System-level validation across target environments

Component-level numbers presented as system range

Integration efficiency

Documented reduction in system size or power

Claims based on prototype designs

Reliability

Qualification data and long-term testing

Short-term lab results used as durability proof

Manufacturing readiness

Production-scale fabrication and supply history

Early-stage devices presented as market-ready

The decision lens

Define the component boundary

Confirm the report focuses only on receiver and photodetector components, not entire LiDAR systems.

Verify segmentation logic

Check that technologies, materials, wavelength compatibility, and integration levels are clearly separated.

Evaluate end-use coverage

Different industries such as automotive, robotics, and mapping have distinct adoption patterns.

Check value chain coverage

Ensure the report analyzes component manufacturers, module suppliers, and system integrators.

Compare technology maturity

Distinguish between established photodiodes and emerging SPAD-based architectures.

Assess market assumptions

Look for clear definitions of market scope and prevention of double counting.

The contrarian view

The LiDAR receiver component market is often misunderstood.

One common mistake is confusing component revenue with full LiDAR system revenue. Photodetectors represent only a portion of the LiDAR value chain.

Another problem is overgeneralizing technology transitions. SPAD arrays receive attention due to automotive LiDAR programs, but many industries continue to rely on mature photodiode technologies.

Boundary mistakes also occur when integrated receiver modules are counted alongside full LiDAR subsystems. Without strict scope definitions, market estimates can easily inflate.

Finally, performance claims can become misleading. Detection range is often a system-level result that depends on lasers, optics, and software, not just photodetectors.

Practical implications by stakeholder

Automotive LiDAR developers

Must balance detector sensitivity with automotive reliability standards.

Integration level directly affects system cost and size.

Industrial automation companies

Favor mature detector technologies with stable manufacturing supply.

Reliability and environmental tolerance matter more than extreme range.

Geospatial and mapping providers

Prioritize accurate signal detection over compact integration.

Largest share portion: Avalanche Photodiodes (APD) take up 27% segment of the component type market and are very well adopted in automotive sensing and industrial LiDAR receivers. Single-Photon Avalanche Diodes (SPAD) are next with 22, and the PIN photodiodes take 18, silicon photomultipliers at 14, and hybrid receiver modules at 12, which points to the wide variety of detection structures.

Readers of this article will find interest in the fastest growing segment: Single-Photon Avalanche Diodes (SPADs) are expected to grow at the highest rate of CAGR, with 17.8%, owing to ultra-sensitive photon detection. APD continues to enjoy a high share of 27 percent with PIN photodiodes (18 percent), SiPM technologies (14 percent), and hybrid receiver modules (12 percent) featuring consistent usage in precision sensing applications.

LiDAR Receiver & Photodetector Components Market – By Material Platform

Introduction/Key Findings

Silicon (Si)

Indium Gallium Arsenide (InGaAs)

Germanium (Ge)

Gallium Arsenide (GaAs)

Compound Semiconductor / Hybrid Materials

Others

Y-O-Y Growth Trend & Opportunity Analysis

LiDAR Receiver & Photodetector Components Market – By Wavelength Compatibility

Introduction/Key Findings

850–905 nm Band

940–1064 nm Band

1310 nm Band

1550 nm Band

Others

Y-O-Y Growth Trend & Opportunity Analysis

LiDAR Receiver & Photodetector Components Market – By Integration Level

LiDAR Receiver & Photodetector Components Market – By End-Use Industry

Introduction/Key Findings

Automotive & Autonomous Vehicles

Industrial Automation & Robotics

Mapping, Surveying & Geospatial

Aerospace & Defense

Smart Infrastructure & Security

Consumer Electronics & AR/VR

Others

Y-O-Y Growth Trend & Opportunity Analysis

The automotive vehicles and autonomous vehicles are the most distributed in the industry, with 32 percent market share, as more LiDAR applications are implemented in advanced driver assistance and autonomous navigation. Industrial Automation & Robotics will have 19 percent, Mapping and Geospatial 13 percent, Aerospace and Defense 12 percent, Smart Infrastructure 10 percent, and Consumer Electronics 9 percent.

Consumer electronics and AR/VR are the fastest-growing segments with an 18.9% CAGR, and they are propelled by an increased need for compact 3D sensing. Automotive has 32 percent dominance, with Industrial Automation (19 percent), Geospatial (13 percent), Aerospace and Defense (12 percent), and Smart Infrastructure (10 percent) making it a diversified LiDAR receiver adoption.

Asia Pacific takes 36 percent of the world market and has backed it with semiconductor manufacturing and the automotive LiDAR market. Emerging deployment landscapes are based on North America of 27, Europe of 20, the Middle East and Africa of 9, and South America of 8.

North America is the quickest developing region with a 16.4% CAGR due to autonomous vehicle technology and defense sensing schemes. Asia Pacific has the highest share of 36 percent, Europe comes next with 20 percent, and the Middle East and Africa occupy 9 percent, and South America occupies 8 percent of the market demand, respectively.

Latest Market News

Mar 05, 2026: A LiDAR supplier announced it shipped 1.2 million receiver units in 2025, which is a 35 percent year-over-year growth due to the increased adoption of automotive ADAS.

Jan 22, 2026: A semiconductor manufacturer announced a SPAD LiDAR receiver array with timing resolution of under 100 ps, and initial samples will be available to automotive customers in Q1 2026.

Oct 18, 2025: A photonics company had expanded into the production of compound semiconductors, with a 28 percentage point increase in output by 2025 due to demand for LiDAR photodetectors.

Jul 09, 2025: A photonics supplier and LiDAR developer entered into a partnership to construct high-efficiency APD receivers, with a 40 percent increase in detection sensitivity.

Apr 14, 2025: A LiDAR technology company also bought a photonics design company to enhance SPAD receiver integration in future automotive sensors.

Nov 21, 2024: The semiconductor manufacturer released an InGaAs photodetector platform for 1550-nm LiDAR with 20 percent better quantum efficiency.

Aug 27, 2024: A LiDAR hardware vendor said 300,000 modules of receivers were shipped in H1 2024, indicating a good demand on robotics and infrastructure.

Feb 12, 2024: A photonics startup raised 75M in Series C funding to mass produce SPAD sensors to be used in LiDAR systems.

Key Players

Hamamatsu Photonics

onsemi

Lumentum Holdings

Excelitas Technologies

First Sensor

Teledyne Technologies

Broadcom Inc.

II-VI Incorporated

STMicroelectronics

ams OSRAM

Questions buyers ask before purchasing this report

What exactly does the LiDAR receiver and photodetector components market include?

This report focuses specifically on semiconductor photodetectors and receiver modules used within LiDAR systems. The scope includes technologies such as avalanche photodiodes, SPAD detectors, PIN photodiodes, silicon photomultipliers, and integrated receiver modules. The market boundary excludes LiDAR transmitters, scanning systems, optics assemblies, and software platforms. This distinction helps maintain a clear component-level perspective on the value chain.

Why separate receiver components from the full LiDAR market?

LiDAR systems combine lasers, optics, detectors, and software. Each layer has its own supply chain and technology roadmap. Receiver components represent the sensing front end responsible for detecting reflected light signals. Separating this layer allows buyers to understand technology trends and supplier dynamics that may be hidden inside broader LiDAR system analyses.

Which industries drive demand for these photodetector components?

Demand comes from several industries that use LiDAR sensing. Automotive autonomy programs represent one of the most visible segments. Industrial automation and robotics also use LiDAR for navigation and obstacle detection. Mapping and geospatial applications depend on precise signal detection. Aerospace, defense, and emerging consumer electronics applications further expand demand.

How do different photodetector technologies compare?

Photodetector technologies differ in sensitivity, cost, and system integration complexity. Avalanche photodiodes provide strong signal amplification. SPAD detectors enable extremely sensitive photon detection and support advanced sensing architectures. PIN photodiodes remain widely used due to their reliability and cost efficiency. Silicon photomultipliers offer high sensitivity in certain designs. Each technology fits different LiDAR architectures.

Why does wavelength compatibility matter?

LiDAR systems operate at specific wavelengths depending on performance and safety requirements. Receiver materials must detect reflected signals efficiently at those wavelengths. Silicon-based detectors typically serve shorter wavelength ranges, while compound semiconductor materials support longer wavelengths used in some high-performance LiDAR systems.

What role does integration level play in the market?

Integration determines how photodetectors connect with electronic signal processing components. Discrete detectors require external circuitry, while integrated receiver modules combine multiple functions. Monolithic receiver chips push integration further by embedding detectors and electronics on the same platform. Higher integration can reduce system size and improve efficiency.

How should buyers compare market reports on this topic?

Buyers should examine whether a report clearly defines market boundaries and segmentation logic. The most useful reports distinguish between detector technologies, material platforms, wavelength compatibility, integration levels, and end-use industries. Transparent definitions and consistent segmentation help ensure the analysis reflects the real structure of the component ecosystem.

What risks exist when estimating this market?

Market estimates can become inaccurate when component boundaries are unclear. For example, counting LiDAR subsystems together with photodetectors can inflate totals. Another risk is assuming one technology will dominate all applications. In reality, different industries use different detector architectures depending on cost, performance, and reliability requirements.

To Learn more about this report,

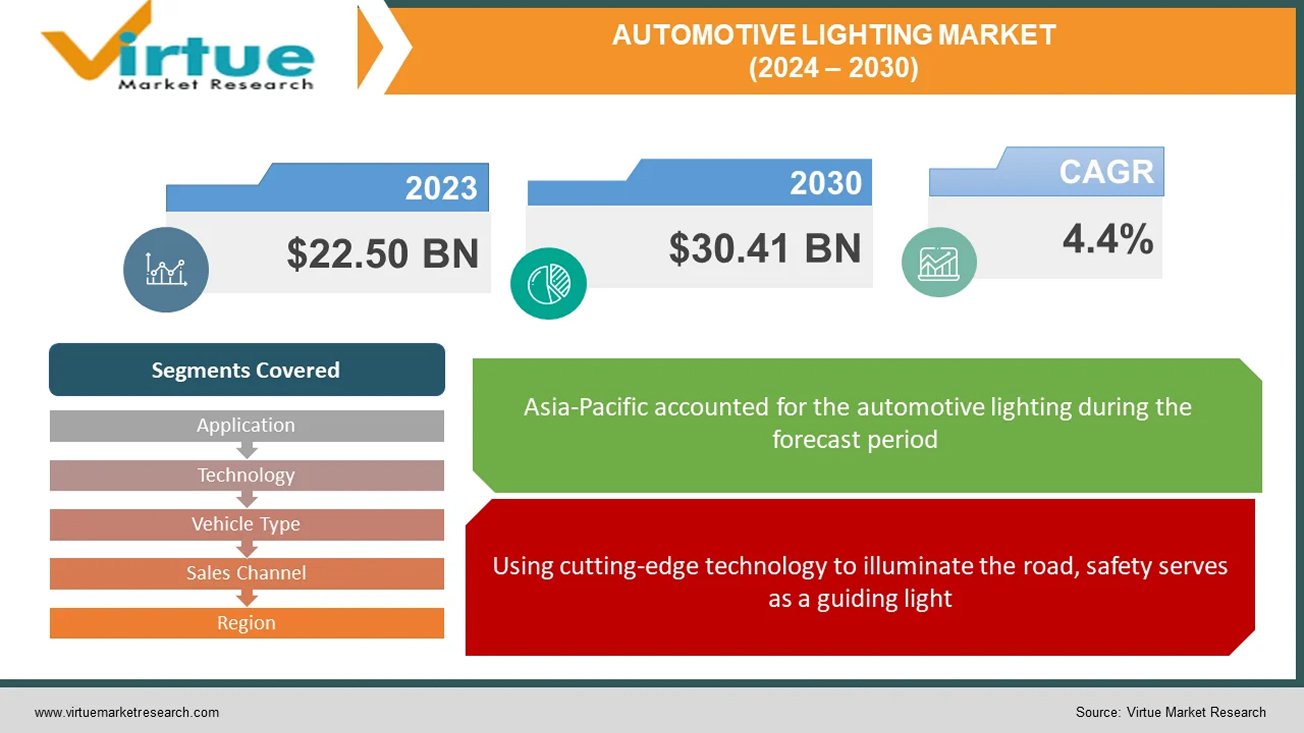

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

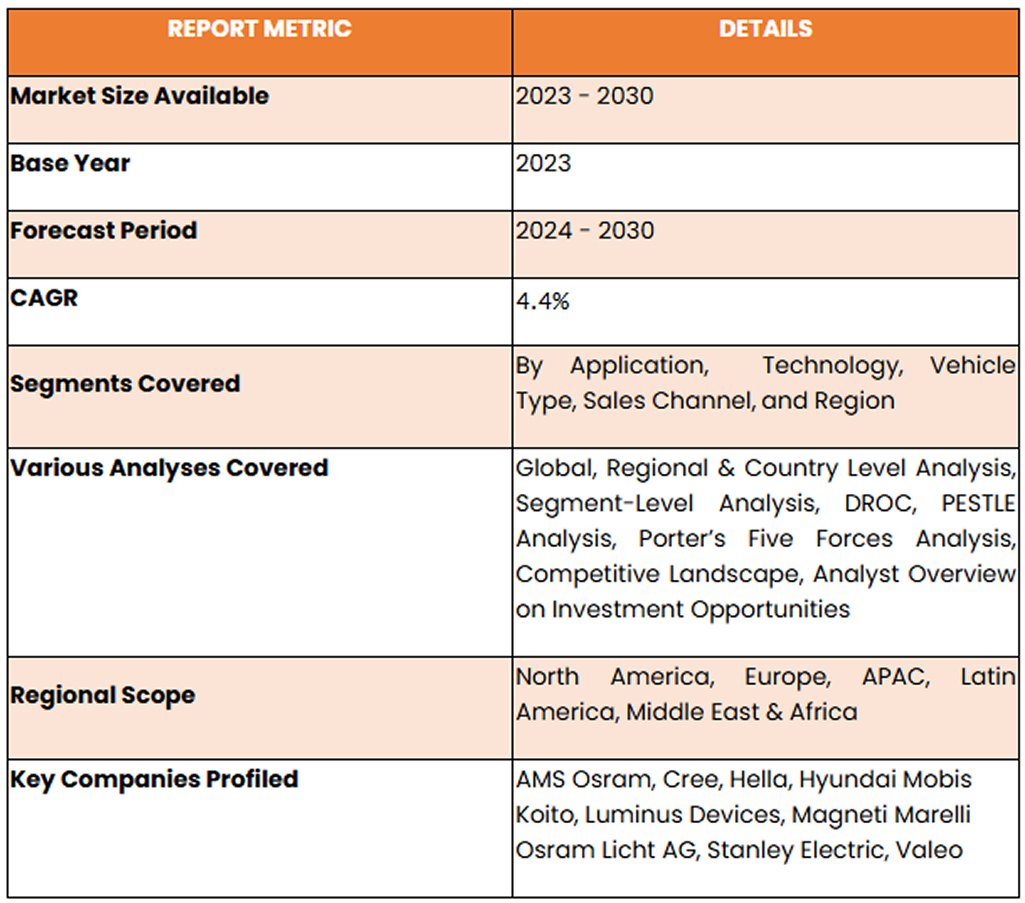

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

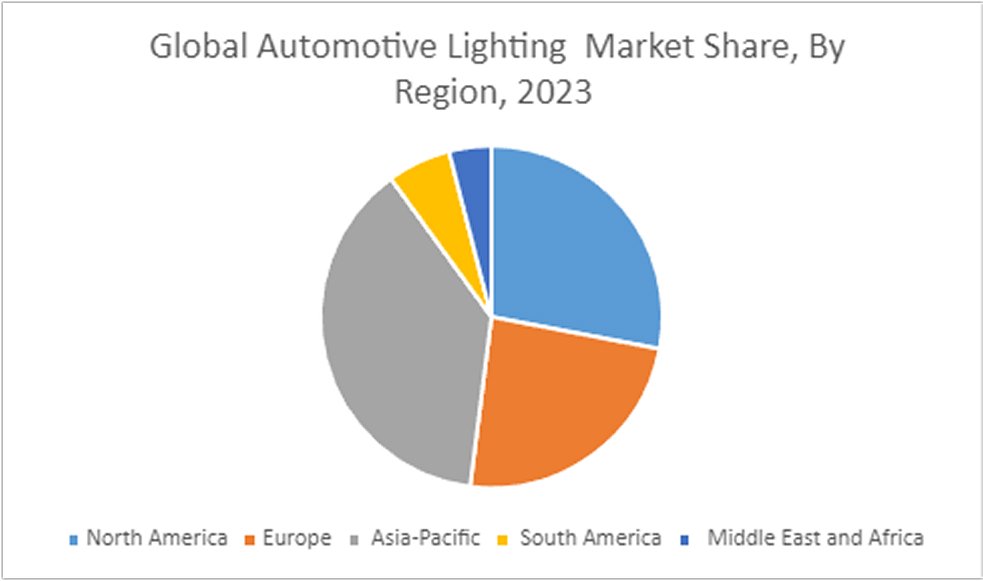

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

11.1.2. By Component Type

11.1.3. By Material Platform

11.1.4. By Wavelength Compatibility

11.1.5. By Integration Level

11.1.6. By End-Use Industry

11.1.7. Countries & Segments - Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Component Type

11.2.3. By Material Platform

11.2.4. By Wavelength Compatibility

11.2.5. By Integration Level

11.2.6. By End-Use Industry

11.2.7. Countries & Segments - Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.1. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Component Type

11.3.3. By Material Platform

11.3.4. By Wavelength Compatibility

11.3.5. By Integration Level

11.3.6. By End-Use Industry

11.3.7. Countries & Segments - Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Component Type

11.4.3. By Material Platform

11.4.4. By Wavelength Compatibility

11.4.5. By Integration Level

11.4.6. By End-Use Industry

11.4.7. Countries & Segments - Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.8. Egypt

11.5.1.9. Rest of MEA

11.5.2. By Component Type

11.5.3. By Material Platform

11.5.4. By Wavelength Compatibility

11.5.5. By Integration Level

11.5.6. By End-Use Industry

11.5.7. Countries & Segments - Market Attractiveness Analysis

Chapter 12. LIDAR RECEIVER & PHOTODETECTOR COMPONENTS MARKET – Company Profiles – (Overview, Type of Training Portfolio, Financials, Strategies & Developments)

Fill out the form below and our team will get back to you shortly

FAQ's

The Global LiDAR Receiver & Photodetector Components Market was valued at approximately USD 1.18 billion in 2025 and is projected to reach an estimated USD 2.30 billion by the end of 2030. Over the forecast period of 2026–2030, the market is expected to grow at a CAGR of around 14.3%.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19367 | Published Date: May 2026 | Format: Excel and PDF

As of 2025, the market was estimated to be around USD 410 billion, which took into account the cumulative investments, production, and development of the ecosystem associated with the localized production of semiconducto...

Report Code: VMR-19286 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the global Nearshoring and Contract Manufacturing for Electronics Market was valued at approximately USD 759.93 billion. It is projected to grow at a CAGR of around 12.66% during the forecast period of 2026–2030...

Report Code: VMR-19221 | Published Date: March 2026 | Format: Excel and PDF

In 2025, the High-Temperature Electronics Market was valued at approximately USD 3.94 billion. It is projected to grow at a CAGR of around 7% during the forecast period of 2026–2030, reaching an estimated USD 5.53 billio...

Report Code: VMR-19228 | Published Date: March 2026 | Format: Excel and PDF

In 2025, the Semiconductor Probe Cards Market was valued at approximately USD 2.6 billion. It is projected to grow at a CAGR of around 7.2% during the forecast period of 2026–2030, reaching an estimated USD 3.68 billion...

Report Code: VMR-19218 | Published Date: March 2026 | Format: Excel and PDF

In 2025, the Semiconductor Wafer Handling & AMHS Market was valued at approximately USD 6.2 billion. It is projected to grow at a CAGR of around 8.6% during the forecast period of 2026–2030, reaching an estimated USD 9.3...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”