Industrial Power Reliability Solutions Market Research Report –Segmentation by Solution Type (Uninterruptible Power Supply (UPS) Systems, Backup Generator Systems, Power Conditioning & Voltage Regulation Systems, Industrial Surge Protection Systems, Power Monitoring & Diagnostics Systems, Others); by Power Capacity (Below 100 kVA, 100 kVA – 500 kVA, 500 kVA – 1 MVA, 1 MVA – 5 MVA, Above 5 MVA, Others); by Deployment Configuration (Standalone Power Reliability Systems, Integrated Power Reliability & Power Quality Systems, Redundant / Parallel Reliability Systems, Modular / Scalable Reliability Systems, Others); by End Use Industry (Manufacturing & Industrial Processing, Data Centers & Digital Infrastructure, Oil & Gas & Energy Facilities, Healthcare & Critical Facilities, Transportation & Infrastructure, Commercial & Institutional Facilities, Others); by Distribution Channel (Direct OEM / Manufacturer Sales, System Integrators & Engineering Procurement Contractors (EPCs), Industrial Electrical Distributors, Others)and Region - Size, Share, Growth Analysis | Forecast (2026– 2030)

Industrial Power Reliability Solutions Market Size (2026-2030)

In 2025, the Industrial Power Reliability Solutions Market was valued at approximately USD 16.49 Billion. It is projected to grow at a CAGR of around 6.1% during the forecast period of 2026–2030, reaching an estimated USD 22.17 Billion by 2030.

The Global Industrial Power Reliability Solutions Market is the ecosystem of technologies and services that are aimed at providing stable, interruption-free, and high-quality electrical power to essential industrial processes. These solutions eliminate outages, voltage fluctuations, and power disturbances, which may cause production interruptions, equipment damage, or destruction of operational safety. The market encompasses, in a broad way, features advanced backup power infrastructure and power conditioning technologies, and intelligent monitoring systems to provide continuity in the operation of industries and mission-critical facilities.

In this market segment, the reliability solutions usually cover equipment and built-in systems used to ensure a constant power supply and protect the industrial operations. It has voltage regulation technologies, surge protection, power quality management, and backup power continuity technologies in large-scale industrial facilities. The market, however, usually does not cover general electrical distribution equipment, consumer-level backup equipment, and non-industrial home power solutions, as the emphasis is still on high-reliability settings where downtime has severe consequences on operations and finances.

It has been a decade since the market changed with increasing automation, the development of digital infrastructure, and the increasing sensitivity of modern equipment to the disruptions of power. The digitisation of industries, the electrification of the manufacturing process, and the growth of production sectors with significant energy consumption have increased the demand for resilient power systems. Furthermore, the evolving sensitisation towards operational risk, emerging tougher compliance needs, and growing integration of intelligent monitoring technologies have already redefined how industries are undertaking power reliability planning.'

Key Market Insights

Outages that are impactful in 2024 were associated with power failures 54% of the time.

Most major outages were incurred by operators of more than 100,000 in the recent past (54%).

Better management would have prevented four out of five serious outages.

An increase in battery storage should be fourteen times by 2030 with a 90% increase.

Investment in the grid will have to almost double, reaching over 600 billion a year in 2030.

Digitalization spending in grids has increased more than 50 percent in the world since 2015.

More than 75% of the digital grid infrastructure expenditure is on distribution grids.

In 2023, APAC had almost 60% of the installed smart meters.

The penetration of smart meters in APAC can be up to 67% at the end of the decade.

The clean energy investment in India in 2023 alone was up to 68 billion.

By 2035, peak electricity demand can increase by 26%, and this puts a strain on reliability.

Eighty percent of manufacturers intend large budget allocations for smart manufacturing in the near future.

Predictive maintenance is able to reduce the downtime of assets by 35-50%.

Research Methodology

Scope & Definitions

Defines the Industrial Power Reliability Solutions Market as product/system sales ensuring continuous, stable industrial power.

Includes UPS systems, backup generators, power conditioning, surge protection, and monitoring systems; excludes routine electrical distribution equipment and services-only contracts.

Global coverage with historical, base-year, and forecast timelines defined in-report.

MECE segmentation applied across solution type, capacity, configuration, industry, and distribution channels.

Data dictionary standardizes technical terms, capacity ranges, and system classifications.

Revenue attribution rules prevent double counting across integrated systems and distribution layers.

Evidence Collection (Primary + Secondary)

Primary interviews with OEM executives, system integrators, EPC firms, industrial facility managers, and reliability engineers across the value chain.

Secondary research uses company filings, annual reports, product documentation, verified trade publications, and market disclosures.

Inputs also reviewed from relevant regulators, standards bodies, and industry associations specific to Industrial Power Reliability Solutions (named in-report).

All key claims supported by verifiable sources and source-linked evidence within the report.

Triangulation & Validation

Market size estimated through bottom-up aggregation of supplier revenues and top-down modeling from industrial power infrastructure spending.

Results reconciled with financial disclosures, shipment trends, and industry investment data.

Conflicting-source resolution applied through weighted credibility scoring and expert validation.

Interview insights cross-checked with documented evidence to reduce bias.

Presentation & Auditability

Findings structured with transparent assumptions, standardized segmentation tables, and consistent market definitions.

Quantitative models maintain traceable calculation logic and documented estimation steps.

Source-linked evidence accompanies major data points and insights.

Methodology, assumptions, and s are documented to ensure full auditability for enterprise decision-making.

Industrial Power Reliability Solutions Market Drivers

Increasing Cost of Industry Downtime and Production Disruption.

In the context of the modern industrial ecosystem, continuous power supply has become one of the most precious working resources unobtrusively. The production, processing plants, and power-intensive industries are now dependent on sophisticated automated equipment that cannot sustain even a short-term power outage. Whole production lines can be halted in a few seconds by a sudden drop in voltage, an unstable grid, or a temporary blackout. Hours are often spent restarting those lines with recalibration, system diagnostics, and quality checks.

Digital Infrastructure and Energy-Intensive Industrial Facilities Growth.

The other significant factor that is influencing the market of industrial power reliability solutions is the expedited growth of digital infrastructure and facilities that consume a lot of energy. Within the last decade, data services, high-performance computing, and advanced manufacturing industries have significantly decreased their electricity consumption.

Raising the instability of grids and the shift to complex energy systems.

The changing complexity of the contemporary power grids is the changing market of the global industrial power-reliability solutions. It is also observed that electricity networks are becoming more variable in many areas because of old infrastructure, wild weather patterns, and the fast adoption of renewable energy sources. Although renewable energy technologies are necessary for long-term sustainability objectives, the intermittent quality may present new grid stability challenges. These fluctuations are especially sensitive to industrial facilities.

Industrial Power Reliability Solutions Market Restraints

Although there is increasing demand to have continuous operations, the global industrial power reliability solutions market suffers from a number of structural limitations. The cost of upfront installation is also high and difficult to integrate with existing industrial infrastructure, which can slow adoption. Lack of confidence in the payback period and high payback periods are some of the reasons why many facilities are reluctant. Another problem that makes system deployment and maintenance difficult is the shortage of a skilled workforce.

Industrial Power Reliability Solutions Market Opportunities

In the global industry power reliability solutions market, opportunities are occurring at any point where the operations in question cannot manage without downtime. Also, accelerated automation in industries, growing digital infrastructure, and more sensitive tools of production are compelling organisations to focus on resilient power environments. Manufacturers are investing in smarter reliability systems where monitoring, protection, and backup functionalities are integrated into a single platform.

How this market works end-to-end

Facilities assess operational risk.

Plants identify which processes cannot tolerate outages or voltage fluctuations. Production lines, data processing equipment, and critical control systems are usually the focus.

Engineers evaluate power quality.

Voltage instability, harmonic distortion, and surge exposure determine what conditioning technologies are required.

Reliability architecture is designed.

Some facilities deploy standalone reliability equipment, while others build integrated reliability systems that combine conditioning, surge protection, monitoring, and backup power.

Capacity requirements are determined.

Reliability equipment ranges from small installations supporting less than 100 kVA to large industrial deployments exceeding several megavolt-ampere systems.

System configuration is selected.

Redundant or parallel architectures are common where downtime risks are high. Modular systems are often used in facilities expecting capacity expansion.

Monitoring and diagnostics tools track system health.

These platforms analyze electrical conditions, detect anomalies, and trigger maintenance before failures occur.

Distribution and integration channels complete the workflow.

Manufacturers supply hardware, but system integrators and engineering procurement contractors often design and implement full reliability solutions.

What matters most when evaluating claims in this market

Claim type

What good proof looks like

What often goes wrong

System reliability

Demonstrated uptime performance in comparable facilities

Vendors quote theoretical availability

Capacity capability

Engineering documentation showing load support ranges

Capacity numbers presented without context

Integration claims

Documented compatibility across monitoring, conditioning, and backup systems

Devices combined without full system design

Downtime prevention

Evidence from real facility deployments

Marketing claims without operational validation

Scalability

Modular expansion design validated in installed environments

Expansion promises that require full replacement

The decision lens

Define downtime tolerance

Identify which operations cannot stop and what outage duration is acceptable.

Map electrical risk

Assess voltage instability, surge exposure, and grid reliability conditions.

Compare reliability architectures

Evaluate standalone, integrated, redundant, or modular system configurations.

Evaluate capacity scaling

Confirm that systems support both current loads and planned facility expansion.

Review monitoring capability

Ensure diagnostic tools provide real-time visibility and predictive maintenance signals.

Validate deployment experience

Ask vendors for examples of installations in similar industries or facility sizes.

The contrarian view

This market often appears simpler than it is.

Many buyers assume reliability equals backup power. In reality, power disturbances often occur without full outages. Voltage sags, spikes, and harmonic distortion can damage equipment long before a generator starts.

Another common mistake is focusing on device specifications rather than system architecture. A powerful UPS does not guarantee reliability if surge protection, conditioning, and monitoring are absent.

Capacity estimates also create confusion. Facilities frequently purchase reliability equipment sized for peak load rather than critical load, increasing cost without improving uptime.

Double counting is another risk when evaluating market claims. Some analyses treat generators, UPS systems, and monitoring platforms as separate markets even when they function as one integrated reliability solution.

Finally, industry-wide claims about reliability standards can be misleading. The requirements of automated factories, data centers, and healthcare facilities differ significantly. One-size reliability strategies rarely work.

Practical implications by stakeholder

Manufacturing operators

Evaluate reliability systems as part of automation strategy.

Downtime risk grows as robotics and digital control increase.

Data center operators

Integrated monitoring and redundancy architecture becomes central.

Reliability planning often prioritizes scalability and expansion.

Energy and industrial infrastructure operators

Reliability investments protect safety systems and control networks.

Facilities must handle unstable grid conditions in many regions.

Healthcare facilities

Reliability systems support life-critical equipment and facility operations.

Monitoring systems help ensure compliance with operational continuity standards.

Engineering procurement contractors

Integration expertise becomes a key differentiator.

Clients increasingly expect full reliability architecture design.

Industrial electrical distributors

Sales increasingly depend on solution knowledge rather than product supply alone.

Partnerships with integrators are becoming more important.

INDUSTRIAL POWER RELIABILITY SOLUTIONS MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2025 - 2030

Base Year

2025

Forecast Period

2026 - 2030

CAGR

6.1%

Segments Covered

By Solution Type , Deployment Configuration , End Use Industry, Power Capacity , Distribution Channel and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

Schneider Electric, Eaton Corporation, ABB Ltd., Siemens AG, Vertiv Group Corp., Mitsubishi Electric Corporation, General Electric Company, Toshiba Corporation, Emerson Electric Co., Cummins Inc., Caterpillar Inc., Legrand SA, Delta Electronics Inc., Fuji Electric Co. Ltd., and Kohler Co.

Industrial Power Reliability Solutions Market Segmentation

Industrial Power Reliability Solutions Market – By Solution Type

Introduction/Key Findings

Uninterruptible Power Supply (UPS) Systems

Backup Generator Systems

Power Conditioning & Voltage Regulation Systems

Industrial Surge Protection Systems

Power Monitoring & Diagnostics Systems

Others

Y-O-Y Growth Trend & Opportunity Analysis

The most significant portion is Uninterruptible Power Supply (UPS) systems, which have approximately 34%, and they are backed by the continuous need for instant power guard in industrial automation and digital facilities. Backup generator systems take almost 27%, power monitoring and diagnostics 14%, power conditioning 13%, surge protection 9%, and others 3 percent.

The strongest segment is power monitoring and diagnostics systems, which is growing at an almost 8.6% CAGR due to predictive maintenance. UPS systems come next at approximately 7.1% growth, voltage regulation solutions at approximately 7.8%, generator systems at approximately 6.8%, surge protectors at approximately 6.5%, and other technology at approximately 5.4%.

Industrial Power Reliability Solutions Market – By Power Capacity

Introduction/Key Findings

Below 100 kVA

100 kVA – 500 kVA

500 kVA – 1 MVA

1 MVA – 5 MVA

Above 5 MVA

Others

Y-O-Y Growth Trend & Opportunity Analysis

Industrial Power Reliability Solutions Market – By Deployment Configuration

Introduction/Key Findings

Standalone Power Reliability Systems

Integrated Power Reliability & Power Quality Systems

Redundant / Parallel Reliability Systems

Modular / Scalable Reliability Systems

Others

Y-O-Y Growth Trend & Opportunity Analysis

Industrial Power Reliability Solutions Market – By End-Use Industry

Introduction/Key Findings

Manufacturing & Industrial Processing

Data Centers & Digital Infrastructure

Oil & Gas & Energy Facilities

Healthcare & Critical Facilities

Transportation & Infrastructure

Commercial & Institutional Facilities

Others

Y-O-Y Growth Trend & Opportunity Analysis

The largest market with 30% of the world's industrial power reliability solutions market is manufacturing and industrial processing, which is based on the automation-intensive production lines that demand consistent power flow. The data centres and digital infrastructure are second with 22% demand, oil and gas and energy facilities with 15% demand, healthcare and critical facilities with 12% demand, transportation and infrastructure with 10% demand, and commercial and institutional facilities with 8% demand.

The fastest-growing segment is data centres and digital infrastructure (9.4% CAGR), which is backed by the growing AI infrastructure and hyperscale computing capabilities. The manufacturing and industrial processing increase at a steady growth rate of about 7.2, with the health care and critical facility sector increasing at the rate of about 7.9, transportation and infrastructural factors increasing at about 7.4, oil and gas and energy increasing at about 6.7, and commercial sectors increasing at the rate of 6.3.

Industrial Power Reliability Solutions Market – By Distribution Channel

Introduction/Key Findings

Direct OEM / Manufacturer Sales

System Integrators & Engineering Procurement Contractors (EPCs)

Industrial Electrical Distributors

Others

Y-O-Y Growth Trend & Opportunity Analysis

Industrial Power Reliability Solutions Market – Regional Analysis

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

The highest regional contribution is in North America, which stands at 32% in the market of industrial power reliability solutions because of the high demand for data centres and industrial automation. Asia Pacific comes second with 29%, Europe with 21%, the Middle East and Africa with 10%, and South America with around 8%.

Asia Pacific is the fastest emerging region with a growth rate of 8.4% CAGR, owing to the speedy industrialisation process and the development of digital infrastructure. North America remains on a steady growth of around 7.1%, whereas the Middle East and Africa are growing steadily around 6.9%, South America is growing steadily around 6.4%, and Europe is growing steadily around 6.1%.

Latest Market News

Mar 05, 2026 - Schneider Electric declared an extended industrial power reliability package that applies to facilities up to 5 MVA, saying efficiency improvements of 18 percent in critical backup designs were implemented in more than 30 industrial locations in early pilot programs in early 2026.

Jan 21, 2026 - Eaton Corporation announced that it partnered with a large digital infrastructure operator to implement 250 innovative UPS modules in 15 operational facilities as a way of enhancing its operational power uptime rate by 22 percent over the former generation systems.

Oct 14, 2025 - ABB introduced a power monitoring platform in industry that could monitor more than 10,000 electrical parameters. Field tests on 40 manufacturing facilities indicated that it reduced the number of unplanned power disturbances by 15%.

Jul 09, 2025 - Vertiv unveiled a modular reliability architecture with 1-5 MVA industrial loads, enabling facilities to increase redundancy capacity by up to 30 percent without overhauling current backup infrastructure.

Apr 18, 2025 - Siemens contracted a supplier of industrial automation to implement power conditioning systems on 120 of its smart manufacturing lines, enhancing the power quality stability by 19 percent in high-duty production facilities.

Nov 27, 2024 - Cummins declared a program of reliability upgrade of industrial generator platforms, which offered new controllers with the potential to detect failures 5 times faster on 300+ installed backup systems.

Aug 12, 2024 - Legrand added the second wave of surge protection products to industrial plants, which it said had been deployed in 20 new infrastructure initiatives to secure equipment used in industries with above 1 MVA loads.

Mar 06, 2024 - Generac Holdings has indicated a strategic acquisition of an industrial energy monitoring technology company in a deal worth approximately 120 million and is aiming at integrating 1,000 installations, globally, that are reliability-centric.

Key Players

Schneider Electric

Eaton Corporation

ABB Ltd.

Siemens AG

Vertiv Group Corp.

Mitsubishi Electric Corporation

General Electric Company

Toshiba Corporation

Emerson Electric Co.

Cummins Inc.

Questions buyers ask before purchasing this report

How is the Industrial Power Reliability Solutions Market defined?

The report defines the market as product and system sales that directly protect industrial operations from power disturbances or outages. This includes UPS systems, backup generators, surge protection equipment, power conditioning systems, and monitoring platforms that manage electrical reliability. The analysis focuses on reliability hardware and integrated system deployments across industrial and infrastructure facilities. Routine electrical distribution equipment and services-only contracts are excluded to maintain a clear market boundary.

Which industries rely most heavily on industrial power reliability systems?

Industries with automated processes or mission-critical operations depend most heavily on reliability solutions. Manufacturing plants use these systems to prevent production losses caused by power disturbances. Data centers rely on layered reliability architectures to protect digital infrastructure. Energy facilities, transportation systems, and healthcare operations also deploy these technologies to maintain operational continuity when grid conditions fluctuate.

What makes power reliability systems different from standard backup power?

Backup power addresses full outages, but industrial reliability solutions handle a wider set of electrical problems. Voltage instability, surges, and harmonic distortion can damage equipment or interrupt automated processes even when the grid remains active. Reliability systems combine conditioning technologies, surge protection, monitoring tools, and backup capacity to maintain stable power conditions across critical operations.

How are reliability systems typically deployed in industrial facilities?

Deployment begins with risk assessment. Facilities identify processes that cannot tolerate power disturbances. Engineers then design reliability architecture that may include conditioning equipment, surge protection, monitoring platforms, and backup power capacity. Systems can be configured as standalone installations or integrated reliability networks with redundancy or modular scalability depending on operational risk.

What role do monitoring systems play in industrial power reliability?

Monitoring platforms provide real-time visibility into electrical conditions across a facility. They detect anomalies such as voltage instability, harmonic distortion, and load fluctuations. These systems also enable predictive maintenance by identifying early warning signals before failures occur. Monitoring capabilities are increasingly central to reliability strategies as industrial operations become more automated.

Why do many reliability projects involve system integrators?

Reliability solutions often require combining multiple technologies into one architecture. System integrators and engineering procurement contractors design and deploy these configurations across complex facilities. Their role includes system design, equipment selection, capacity planning, and integration with monitoring platforms. This integration expertise has become critical as reliability systems grow more complex.

How does system capacity influence reliability strategy?

Capacity decisions depend on facility size, operational risk tolerance, and expected expansion. Smaller installations may require limited reliability support, while large industrial sites often deploy multi-megavolt systems. Some facilities choose modular systems that allow capacity expansion without replacing existing infrastructure. Capacity planning is therefore both a technical and operational decision.

What should buyers compare when evaluating vendors?

Buyers typically compare system architecture capability, deployment experience, monitoring integration, and capacity scalability. Evidence of successful installations in comparable industries can be more valuable than device specifications alone. Vendors that demonstrate integration expertise and operational reliability across complex facilities usually provide the strongest long-term value.

To Learn more about this report,

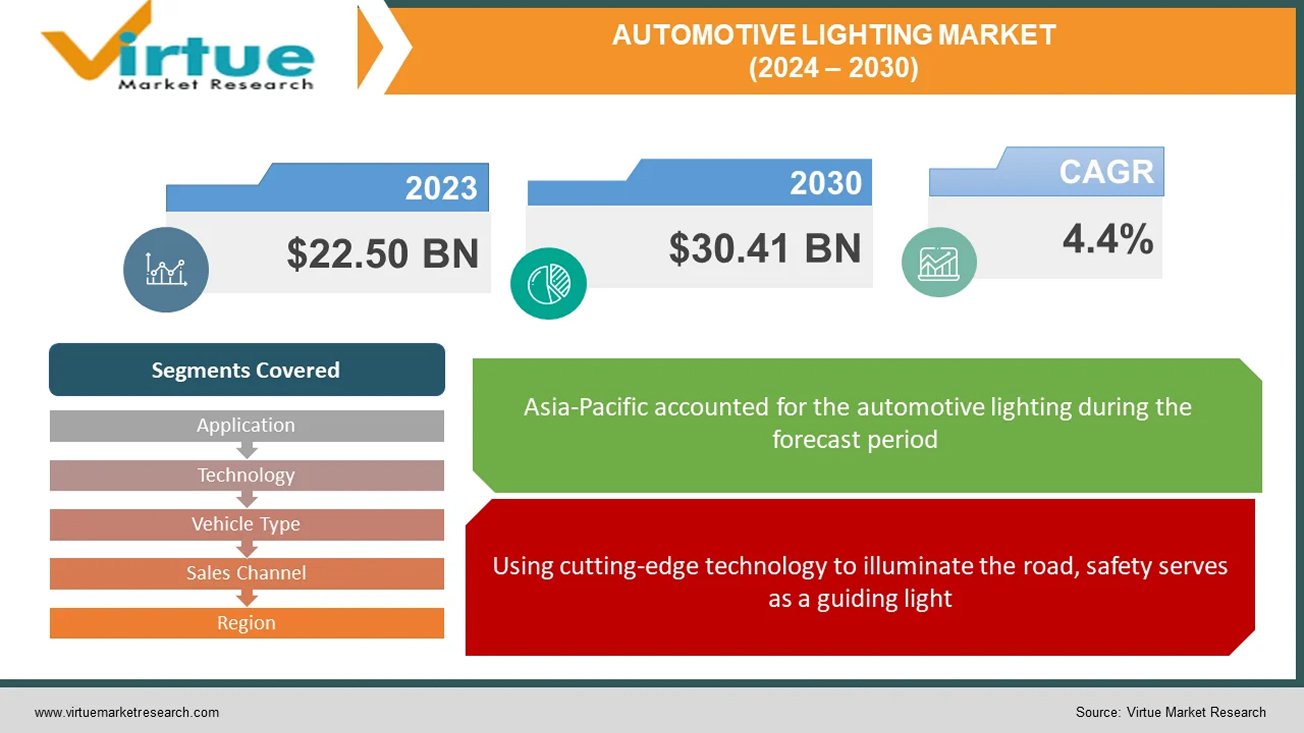

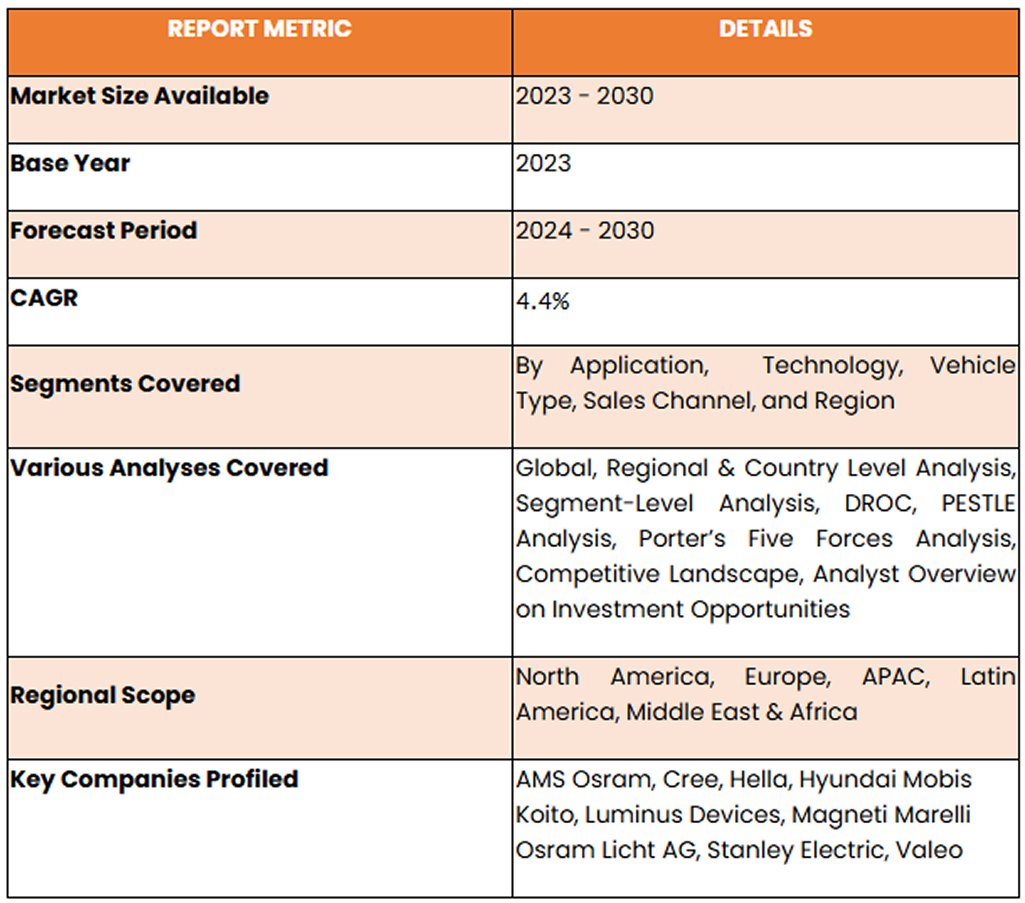

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

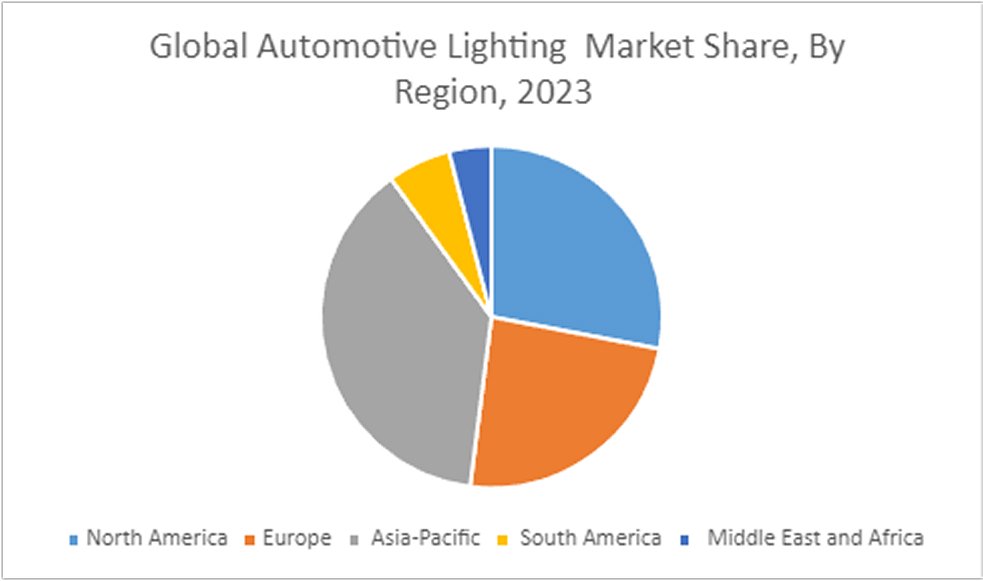

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1 Industrial Power Reliability Solutions Market– Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources Chapter 2 Industrial Power Reliability Solutions Market – Executive Summary

2.1. Market Solution Type Model & Forecast – (2026 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis Chapter 3 Industrial Power Reliability Solutions Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis Chapter 4 Industrial Power Reliability Solutions Market - Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Chapter 5 Industrial Power Reliability Solutions Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6 Industrial Power Reliability Solutions Market – By Solution Type

6.1 Introduction/Key Findings

6.2 Uninterruptible Power Supply (UPS) Systems

6.3 Backup Generator Systems

6.4 Power Conditioning & Voltage Regulation Systems

6.5 Industrial Surge Protection Systems

6.6 Power Monitoring & Diagnostics Systems

6.7 Others

6.8 Y-O-Y Growth trend Analysis Solution Type

6.9 Absolute $ Opportunity Analysis By Solution Type , 2026-2030

Chapter 7 Industrial Power Reliability Solutions Market – By Power Capacity

7.1 Introduction/Key Findings

7.2 Below 100 kVA

7.3 100 kVA – 500 kVA

7.4 500 kVA – 1 MVA

7.5 1 MVA – 5 MVA

7.6 Above 5 MVA

7.7 Others

7.8 Y-O-Y Growth trend Analysis By Power Capacity

7.9 Absolute $ Opportunity Analysis By Power Capacity , 2026-2030

Chapter 8 Industrial Power Reliability Solutions Market – By Deployment Configuration

8.1 Introduction/Key Findings

8.2 Standalone Power Reliability Systems

8.3 Integrated Power Reliability & Power Quality Systems

8.4 Redundant / Parallel Reliability Systems

8.5 Modular / Scalable Reliability Systems

8.6 Others

8.7 Y-O-Y Growth trend Analysis Deployment Configuration

8.8 Absolute $ Opportunity Analysis Deployment Configuration, 2026-2030 Chapter 9 Industrial Power Reliability Solutions Market – By End-Use Industry

9.1 Introduction/Key Findings

9.2 Manufacturing & Industrial Processing

9.3 Data Centers & Digital Infrastructure

9.4 Oil & Gas & Energy Facilities

9.5 Healthcare & Critical Facilities

9.6 Transportation & Infrastructure

9.7 Commercial & Institutional Facilities

9.8 Others

9.9 Y-O-Y Growth trend Analysis End-Use Industry

9.10 Absolute $ Opportunity Analysis End-Use Industry , 2026-2030

Chapter 10 Industrial Power Reliability Solutions Market – By Distribution Channel

10.1 Introduction/Key Findings

10.2 Direct OEM / Manufacturer Sales

10.3 System Integrators & Engineering Procurement Contractors (EPCs)

10.4 Industrial Electrical Distributors

10.5 Others

10.6 Y-O-Y Growth trend Distribution Channel

10.7 Absolute $ Opportunity Distribution Channel , 2026-2030

Chapter 11 Industrial Power Reliability Solutions Market, By Geography – Market Size, Forecast, Trends & Insights

11.1. North America

11.1.1. By Country

11.1.1.1. U.S.A.

11.1.1.2. Canada

11.1.1.3. Mexico

11.1.2. By Power Capacity

11.1.3. By End-Use Industry

11.1.4. By Solution Type

11.1.5. Power Capacity

11.1.6. Distribution Channel

11.1.7. Countries & Segments - Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Deployment Configuration

11.2.3. By End-Use Industry

11.2.4. By Solution Type

11.2.5. Power Capacity

11.2.6. Distribution Channel

11.2.7. Countries & Segments - Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.2. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Deployment Configuration

11.3.3. By End-Use Industry

11.3.4. By Solution Type

11.3.5. Power Capacity

11.3.6. Distribution Channel

11.3.7. Countries & Segments - Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Deployment Configuration

11.4.3. By End-Use Industry

11.4.4. By Solution Type

11.4.5. Power Capacity

11.4.6. Distribution Channel

11.4.7. Countries & Segments - Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.11. Egypt

11.5.1.11. Rest of MEA

11.5.2. By Deployment Configuration

11.5.3. By End-Use Industry

11.5.4. By Solution Type

11.5.5. Power Capacity

11.5.6. Distribution Channel

11.5.7. Countries & Segments - Market Attractiveness Analysis

Chapter 12 Industrial Power Reliability Solutions Market – Company Profiles – (Overview, Power Capacity Portfolio, Financials, Strategies & Developments)

12.1 Schneider Electric

12.2 Eaton Corporation

12.3 ABB Ltd.

12.4 Siemens AG

12.5 Vertiv Group Corp.

12.6 Mitsubishi Electric Corporation

12.7 General Electric Company

12.8 Toshiba Corporation

12.9 Emerson Electric Co.

12.10 Cummins Inc

Fill out the form below and our team will get back to you shortly

FAQ's

In 2025, the Industrial Power Reliability Solutions Market was valued at approximately USD 16.49 Billion. It is projected to grow at a CAGR of around 6.1% during the forecast period of 2026–2030, reaching an estimated USD 22.17 Billion by 2030.

. The major drivers of the Global Industrial Power Reliability Solutions Market include the increasing cost of industrial downtime and production disruption, the rapid growth of digital infrastructure and energy-intensive industrial facilities, and the rising instability of modern power grids due to aging infrastructure and renewable energy integration. Additionally, the growing adoption of automation, electrification of manufacturing processes, and intelligent power monitoring technologies is accelerating demand for reliable and uninterrupted industrial power systems.

Uninterruptible Power Supply (UPS) Systems, Backup Generator Systems, Power Conditioning & Voltage Regulation Systems, Industrial Surge Protection Systems, Power Monitoring & Diagnostics Systems, and Others are the segments under the Global Industrial Power Reliability Solutions Market by Solution Type.

North America is the most dominant region for the Global Industrial Power Reliability Solutions Market due to the high concentration of data centers, advanced industrial automation, and strong investments in power reliability infrastructure across critical industrial and digital facilities

Schneider Electric, Eaton Corporation, ABB Ltd., Siemens AG, Vertiv Group Corp., Mitsubishi Electric Corporation, General Electric Company, Toshiba Corporation, Emerson Electric Co., Cummins Inc., Caterpillar Inc., Legrand SA, Delta Electronics Inc., Fuji Electric Co. Ltd., and Kohler Co. are key players in the Global Industrial Power Reliability Solutions Market.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-19366 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the HVDC Transmission Systems Market was valued at approximately USD 13.84 Billion. It is projected to grow at a CAGR of around 7.7% during the forecast period of 2026–2030, reaching an estimated USD 20.05 Billi...

Report Code: VMR-19364 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Reactive Power Compensation Market was valued at approximately USD 8.14 Billion. It is projected to grow at a CAGR of around 8.3% during the forecast period of 2026–2030, reaching an estimated USD 12.13 Bill...

Report Code: VMR-19363 | Published Date: May 2026 | Format: Excel and PDF

In 2025, the Microgrid Controllers & Integration Services Market was valued at approximately USD 5.84 Billion. It is projected to grow at a CAGR of around 9.8% during the forecast period of 2026–2030, reaching an estimat...

Report Code: VMR-19318 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the Grid Protection & Control Systems Market was valued at approximately USD 109.7 Billion. It is projected to grow at a CAGR of around 8% during the forecast period of 2026–2030, reaching an estimated USD 161.1...

Report Code: VMR-19314 | Published Date: April 2026 | Format: Excel and PDF

In 2025, the AI Model Monitoring and Guardrails Market was valued at approximately USD 2,140 million. It is projected to grow at a CAGR of around 8.40% during the forecast period of 2026–2030, reaching an estimated USD 3...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”